Digital Infrastructure: The Next Generation of Real Assets

- Digital infrastructure — spectrum, wireless towers, fiber networks, and data centers — serves as the backbone of the internet and has created tremendous opportunities for public and private investors.

- The compelling and unique features of digital infrastructure — high barriers to entry and asset scarcity — provide the opportunity for stable cash flows and attractive returns.

- Bessemer Trust’s investment professionals have developed a deep understanding of the opportunities, risks, and rewards of the digital infrastructure ecosystem and are sourcing and executing compelling investment opportunities for clients.

A Deep Dive Into Digital Infrastructure Investments

Digital infrastructure underpins the global trend of “more, better, faster, everywhere” data consumption. It brings together and interconnects physical and virtual technologies such as computing, storage, and applications to deliver data and digital content. Four key components of digital infrastructure — spectrum, wireless towers, fiber networks, and data centers — serve as the backbone of the internet (Exhibit 1). These networks — or digital infrastructure — have created tremendous opportunities for public and private investors.

While Bessemer’s public equity team has invested in companies focused on communications and data movement for decades, digital infrastructure represents a newer opportunity set in private real assets investing. The unique characteristics of these assets — their intrinsic value or resilient cash flow profile — have made them a critical component of the next generation of real assets portfolios.

In this A Closer Look, we explore the key characteristics, trends, and opportunities associated with digital infrastructure and why this collection of assets has become an important component of Bessemer’s real assets and public equity portfolios.

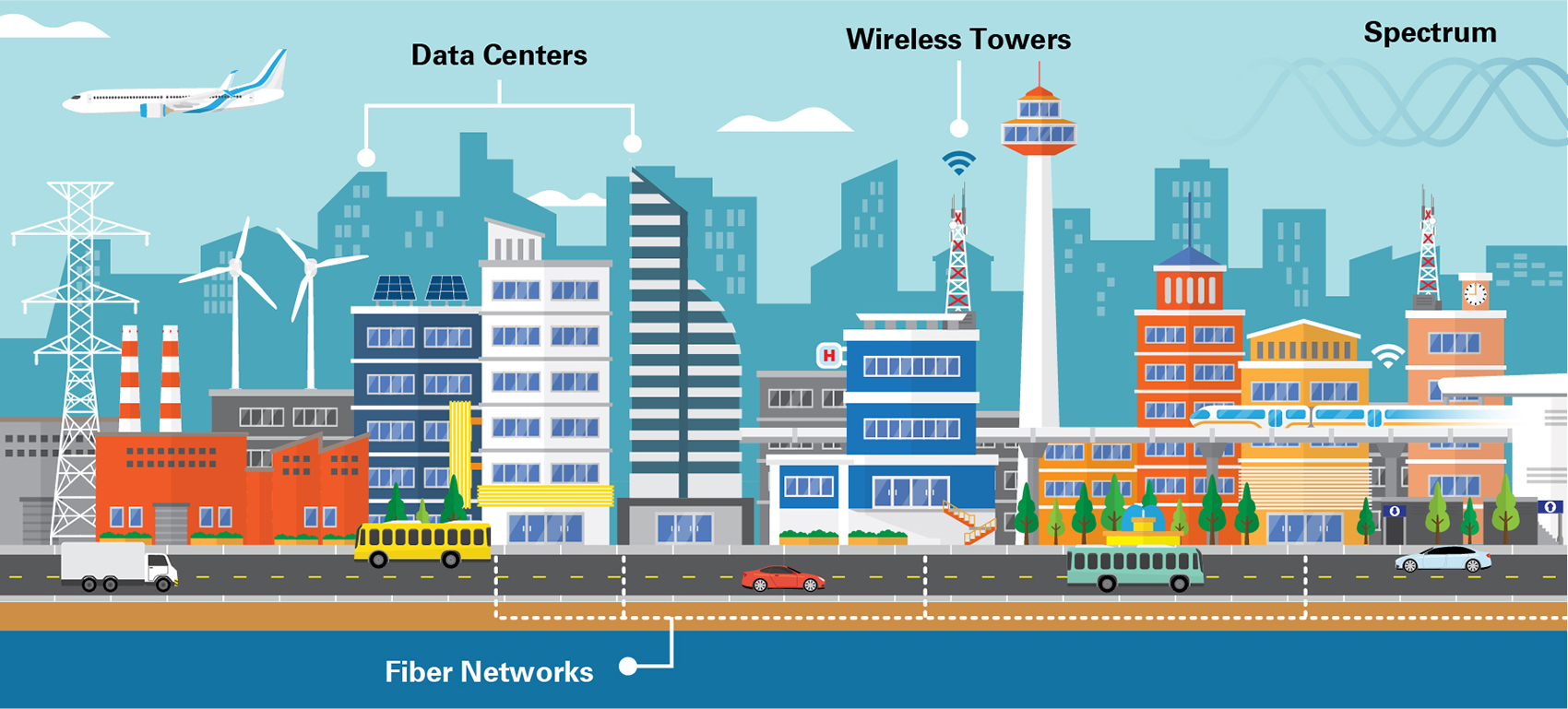

Exhibit 1: What Is Digital Infrastructure?

Exhibit 1 depicts a crowded cityscape and identifies the four key components of digital infrastructure — spectrum, wireless towers, fiber networks (below ground), and data centers. Source: Bessemer Trust, Schroders

Introduction to the Digital Infrastructure Ecosystem

From the first telegram sent from Washington, D.C., to Baltimore in 1844, to the first handheld cellular phone call in 1973, the use of wires and radio waves to communicate has transformed economies. Information that once spanned thousands of pages (e.g., World Book encyclopedias) and days to locate now appears instantaneously. A 2022 report by telecom equipment manufacturer Ericsson highlighted that the global monthly average usage for smartphones is anticipated to be 19 gigabytes (GB) per person this year and reach 46 GB by the end of 2028. As a reference, 20 GB of data usage roughly translates to listening to 140 hours of music on Spotify, viewing 20 hours of video on Netflix, or browsing social media for 220 hours. New use cases and applications based on autonomous vehicles, artificial intelligence, or telemedicine are just a few examples of the innovations that will be driven by faster, reliable, and secure data transmissions.

Real assets serve as the fundamental building blocks of productive societies. These assets are often underpinned by long-term contracts or leases. As a result, during periods of market volatility, real assets can solve for a range of client objectives by providing both downside resilience as well as an income cushion and inflation protection. Notably, as our economies evolve, the definition of what constitutes a fundamental building block also evolves. As we continue to prioritize connectivity, digital infrastructure assets, such as wireless towers, fiber networks, and data centers, are increasingly recognized as real assets. These assets, along with the key enabler of spectrum, are the fuel and engine that enable today’s digital world (Exhibit 2).

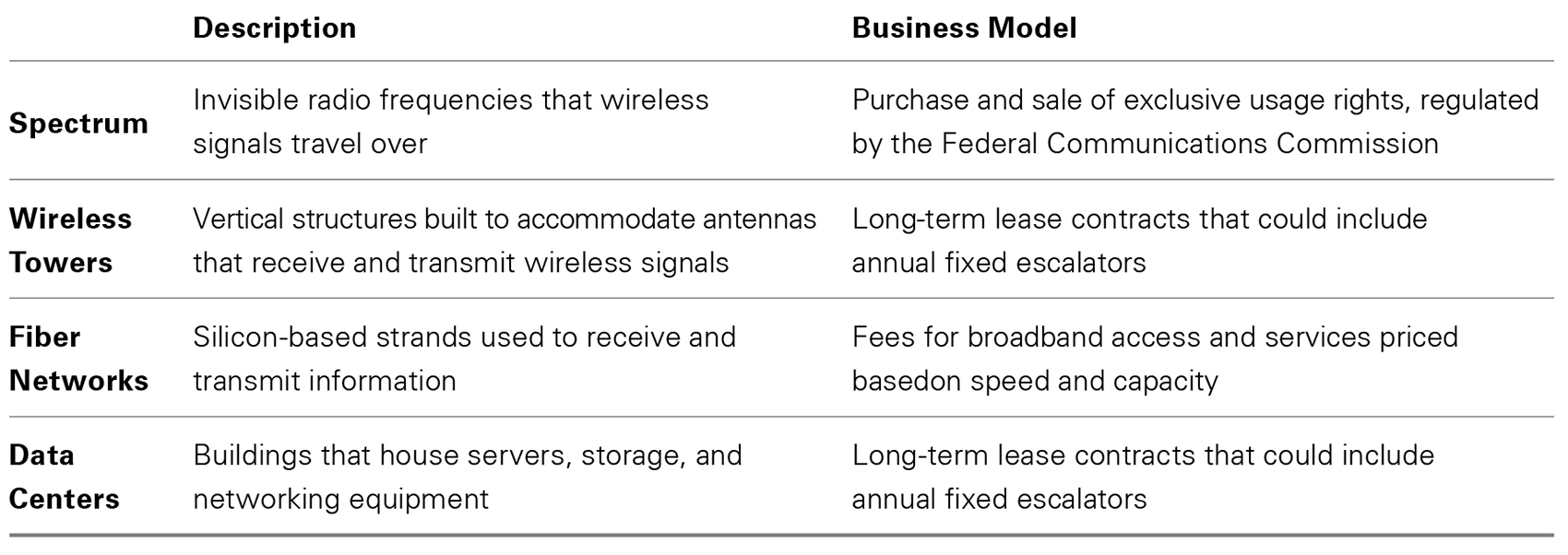

Exhibit 2: Key Features of Digital Infrastructure

Exhibit 2 is a table that provides a description of a component of digital infrastructure and its business model. For Spectrum, the description is the invisible radio frequencies that wireless signals travel over, and the business model is the purchase and sale of exclusive usage rights, regulated by the Federal Communications Commission. Wireless towers are described as vertical structures built to accommodate antennas that receive and transmit wireless signals; its business model is long-term lease contracts that could include annual fixed escalators. Fiber networks are described as silicon-based strands used to receive and transmit information; its business model is based on fees for broadband access and services that are priced based on speed and capacity. Data centers are described as buildings that house servers, storage, and networking equipment; its business model is based on long-term lease contracts that could include annual fixed escalators. The source is Bessemer Trust.

Digital Infrastructure Asset #1: Spectrum

Spectrum can be thought of as the fuel in digital engines. Spectrum consists of invisible radio frequencies over which wireless signals travel. In the U.S., the Federal Communications Commission (FCC) regulates the commercial use of spectrum. Since 1993, the FCC has conducted auctions granting winning bidders exclusive usage rights. Recently, the advent of 5G (the latest generation of cellular technology) has ushered in renewed demand for spectrum, especially for potential new use cases. 5G operates on three frequency bands: low, mid, and high. Of these three frequencies, mid-band is considered the “sweet spot” spectrum, providing both fast speeds as well as wide coverage.

Over the past two years, the three largest U.S. wireless companies — Verizon, AT&T, and to a lesser extent, T-Mobile — have raced to acquire mid-band spectrum to support their 5G rollout. In 2020, T-Mobile got a head start when it merged with Sprint, which had prime, underutilized mid-band spectrum holdings. When the FCC held new mid-band spectrum auctions in 2021, Verizon and AT&T saw an opportunity to catch up, though it came at a price. Indeed, one auction that concluded in February of that year raised more than $81 billion, becoming the highest grossing spectrum auction in U.S. history. Verizon and AT&T spent more than $45 billion and $32 billion, respectively, for mid-band spectrum over two auctions, highlighting its importance for the companies’ long-term strategic positioning. Wireless companies were major buyers, but cable companies and private equity firms also acquired large swathes of these scarce assets.

Bessemer’s real assets team worked with two managers who bid in the 2021 auctions and were awarded spectrum assets. The team pursued a barbell strategy, participating with one manager who invested in less densely populated but growing regions crucially anchored by state capitals or colleges, and a second manager who acquired spectrum in top U.S. cities and high-density markets. The scarcity of spectrum coupled with consumers’ ever-increasing demand for data has created compelling investment opportunities.

Digital Infrastructure Asset #2: Wireless Towers

If spectrum is the fuel for digital infrastructure’s engines, then wireless towers are key components of the transmission. The earliest radio towers date back to the 1920s and were used by AM radio, then FM radio, and subsequently TV. Public services networks also owned and operated their own towers. The advent of consumer cellphone service in the early 1990s was a catalyst for the tower industry. Advances in mobile devices further accelerated demand for towers. Recently, efforts by carriers to deliver wireless broadband have provided even more demand.

Tower companies build, own, and operate vertical structures, referred to as wireless towers, that host antennas that receive and transmit wireless signals. The smallest towers, referred to as monopole towers, may be no more than 100 feet in height. Large lattice-structured self-supporting towers typically range from 150 to 400 feet, and the tallest towers that can reach 2,000 feet or more are anchored by steel cables. U.S. wireless companies (AT&T, T-Mobile, Verizon, among others), radio stations, and TV networks lease space for their equipment on both the towers as well as the land below. This collection of towers, antennas, and electronic communications equipment, referred to as a cellsite, provides signals and connectivity for voice, video, and data services. Monthly rental rates paid by tenants for sites vary widely and can be as low as a few hundred dollars per month for smaller or rural sites to several thousand dollars for cellsites in high traffic, dense areas.

According to the Cellular Telecommunications Industry Association, there are about 150,000 communications towers in the U.S. There is an oligopoly of publicly traded, U.S.-based tower companies that includes American Tower, Crown Castle, and SBA Communications. These three companies control about 73% of the domestic market. The balance of the U.S. market is controlled by a handful of private equity-backed tower companies and small operators that position themselves as potential acquisition targets for the public companies.

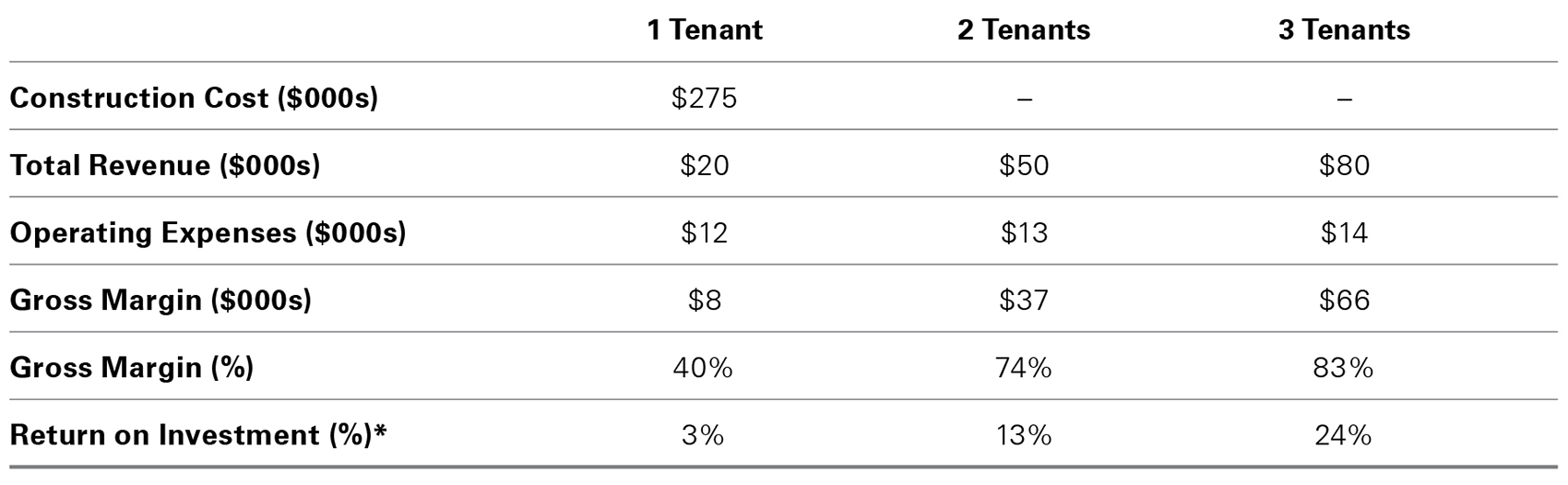

The business model for the tower companies is simple yet facilitates compelling and attractive economics with low operating costs. Tower companies essentially build steel poles to hang antennas. High quality tenants pay monthly rent that usually includes built-in escalators that average about 3% per annum. These recurring, long-term contractual payments provide tower companies with a stable and highly predictable revenue stream. Because of the complicated and time-consuming permitting and municipal regulatory challenges associated with locating and then building a tower, especially in residential areas, towers’ value, pricing, and cash flows are functions of location. This leads to limited supply in many areas, which has resulted in increased pricing power for tower companies. Demand for wireless network services, especially data, has been robust and growing (one study cited that mobile data usage in the U.S. grew at a compounded annual growth rate of 55% from 2007 through 2022). Once wireless carriers activate cellsites, they become mission-critical infrastructure difficult to replace or decommission. This leads to low customer churn rates that have historically averaged less than 2% annually. Finally, the low operating and variable costs coupled with high operating leverage (as a second or third tenant is added to a tower, the operating margin per tower ramps up significantly) create very attractive unit economics. Exhibit 3 illustrates the typical margin expansion economics for a single cell tower as tenants increase from one to three.

Bessemer’s equities and real assets teams currently have several investments in the tower space. For example, American Tower (AMT), the second largest publicly traded REIT in the S&P 500, is a current holding. In private markets, the real assets team has backed a specialist manager who partners with leading tower developers who construct and operate wireless tower assets located in the path of population or data usage growth.

Exhibit 3: Cell Tower Economics

Key takeaway: Tower model demonstrates attractive economics as tenancy increases.

Key takeaway: Tower model demonstrates attractive economics as tenancy increases. Exhibit 3 is a table that describes the changing economics as various tenants are added to a cell tower – construction costs, total revenue, operating expenses, gross margin in dollars and percentages, and return on investment. For one, two, and three tenants, respectively, in thousands of dollars, construction costs remain fixed at $275, operating expenses are $12, $13, and $14; and gross margin is $8, $37, and $66; in percentage terms, gross margin is 40%, 74%, and 83%, and return on investment is 3%, 13%, and 24%. This data is as of September 30, 2022. Return on Investment is calculated as gross margin divided by construction cost. Source is American Tower

*Return on Investment is calculated as gross margin divided by construction cost.

Source: American Tower

Digital Infrastructure Asset #3: Fiber Networks

Fiber networks serve as a key element of the digital infrastructure engine’s transmission. Fiber cables are created from flexible, translucent fiber strands made by drawing silica or plastic to a diameter equating to the thickness of a human hair. These cables are then connected to high-speed lasers and other electronics.

Historically, telecom customers typically chose between copper- and fiber-based options. Today, fiber optic networks have largely replaced copper options for high-capacity lines and are the superior technological solution given their ability to carry data quickly and efficiently (fiber optic cables communicate at the speed of light). However, copper-based networks have historically dominated, especially for connections to residential homes since copper wires were cheaper to manufacture and install. As a result, fiber penetration in the U.S. has lagged that of other countries.

Over the past decade, however, cable companies have increasingly stepped into the void to address consumer demand for faster service via hybrid fiber coaxial cable, combining both fiber and Ethernet cables. For most American consumers, internet through their local cable companies is now the preferred option.

In response, U.S. wireless companies have been rapidly looking to gain market share in this segment. To that end, they have announced ambitious plans to reach 68 million homes by 2025. New start-up entrants are also building positions in secondary and tertiary markets by offering faster and cheaper services. Unlike the market for towers, the fiber market is fragmented across participants. Notably, brand new fiber networks are expensive to build, now more so than ever. Rising inflation costs combined with supply chain challenges have slowed some of those ambitions, with newer entrants as well as incumbents carefully assessing project economics in a higher interest rate environment.

Bessemer’s real assets team has backed managers who specialize in funding the development of fiber networks and providing faster broadband service to underserved residential and commercial markets. Investments that move forward typically include those offered at compelling build economics and that create a differentiated customer experience.

Digital Infrastructure Assets #4: Data Centers

Data centers go back to the 1940s, when the U.S. government designed special rooms to house super computers for military purposes. During the 2000s, companies looked to have their own websites with their IT systems located on premise. However, as public cloud divisions such as Amazon Web Services have gained traction, companies have migrated their operations to these large public cloud service providers.

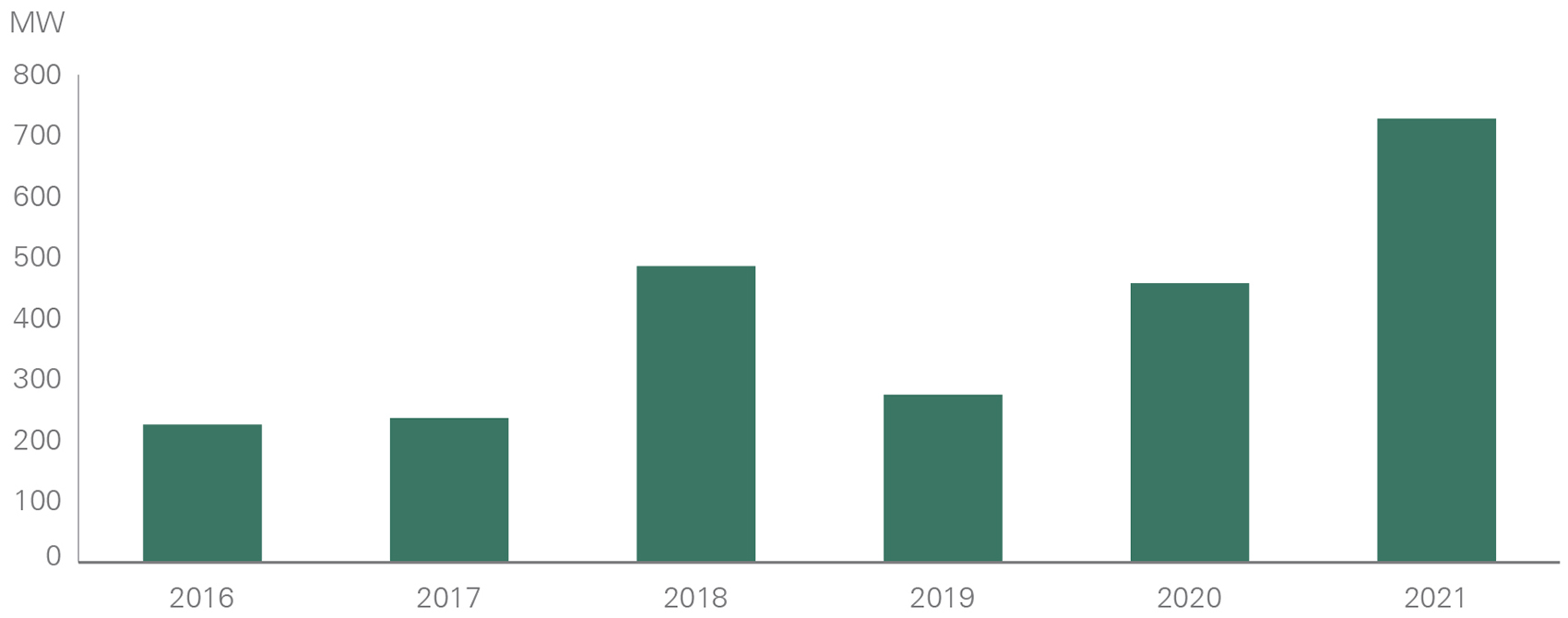

A data center is a climate-controlled building (or group of buildings) that houses servers, storage, and networking equipment. These buildings require significant space, power (Exhibit 4), and cooling — a large data center can use as much electricity as a small town. More and more companies are outsourcing their data center needs to third party providers (also known as colocation providers), such as publicly traded Equinix and Digital Realty, fueling the growth of data centers.

Exhibit 4: Data Centers Power Supply Under Construction

Key takeaway: Data centers have high power needs.

Key takeaway: Data centers have high power needs. Exhibit 4 is a bar chart depicting the significant and increasing annual power needs of data centers from 2016 (slightly more than 200 megawatts) to 2021 (over 700 megawatts). Data is as of March 31, 2022. Source: CBRE

Source: CBRE

The data center business model is notable for its high visibility into future cash flows, typically due to long-term lease contracts (that include annual fixed escalators) and low customer churn (industry revenue churn is 1% to 3% quarterly, but actual customer churn is lower). Fixed costs are high due to the upfront investment in real estate and construction of the warehouse. Variable costs, however, tend to be lower as they are comprised primarily of power and cooling, resulting in high incremental margins.

There are high barriers to entry in the data center business: significant upfront capital requirements to buy real estate and build a warehouse and long lead times to secure a location and interconnections. Given how mission-critical IT infrastructure is, companies are likely to outsource it to established players with long operating histories, favoring larger incumbents. For the same reasons, switching costs tend to be high in the industry, amplified by the cost and effort to move from one data center to another and the related risk of business disruption.

Bessemer public equity portfolios hold positions in Brookfield Corporation (BN) and Blackstone (BX), both of which are alternative investment managers who have been investing in data centers. Brookfield Corporation owns 75% of Brookfield Asset Management (BAM), which owns or has stakes in more than 50 data centers while Blackstone-sponsored funds announced the acquisition of QTS Realty Trust for $10 billion in 2021, which at the time was the largest transaction in data center history. American Tower (AMT), a Bessemer equity portfolio holding mentioned earlier, acquired CoreSite (COR) and its portfolio of 25 data centers for $10 billion in 2021. Bessemer’s real assets team backed a specialist manager with a track record in data center development for hyperscalers such as public cloud service providers.

Case Study: ChatGPT

Terms such as edge computing, natural language processing, and most recently, ChatGPT have entered our lexicon over the past few years. Most of these terms refer to burgeoning services and applications whose architects promise will “change the way we do things.” Undoubtedly, many of these services will prove to be transformational. But what do they have to do with digital infrastructure? Let us explore by delving into ChatGPT.

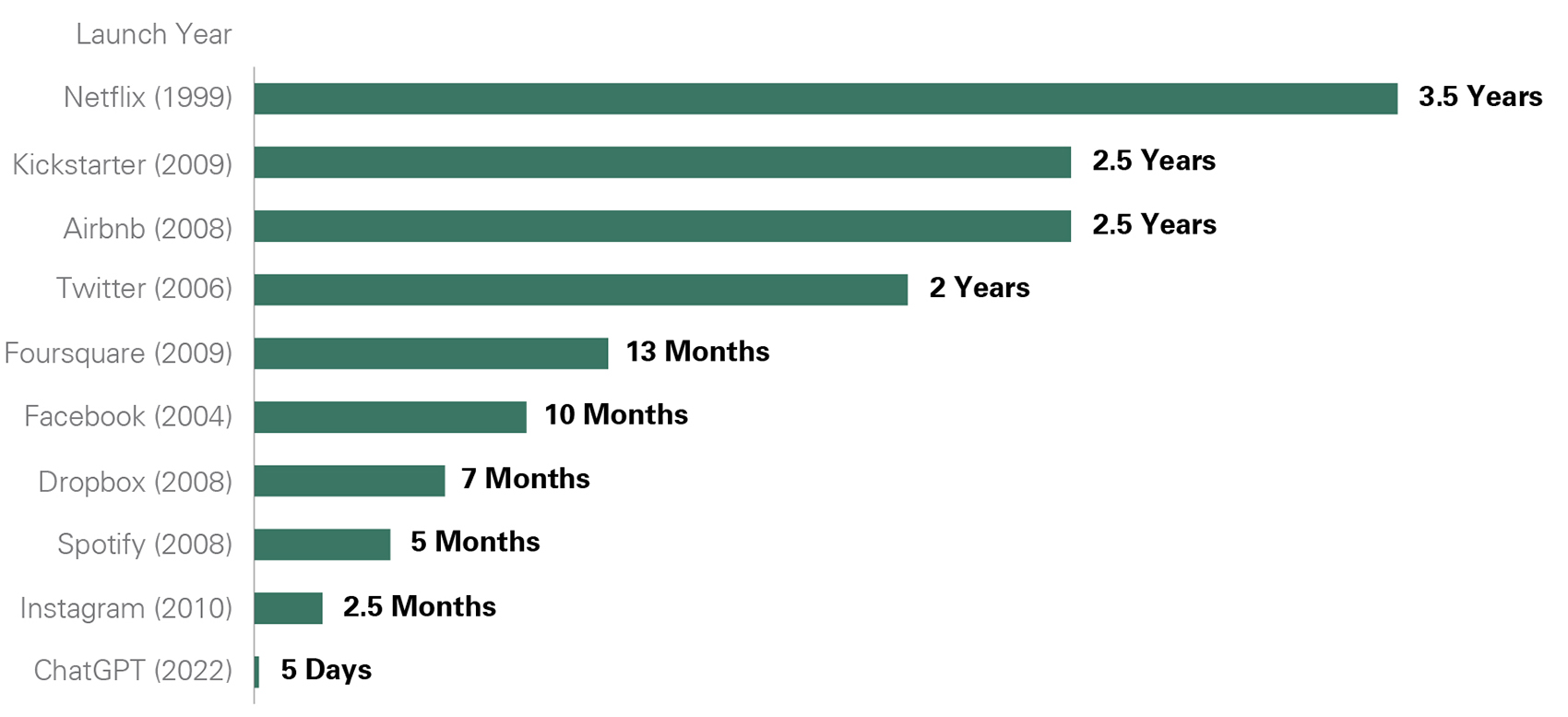

The GPT in ChatGPT stands for generative pre-trained transformer. In layman’s terms, this refers to statistical models that allow text queries to be converted to conversational sentences. If we combine GPT with “Chat” we have what is characterized as a chatbot application that promises to merge the best of internet search output/algorithms with simple, plain language narratives that are both easily understood and instantaneously accessible. As Exhibit 5 highlights, the explosive adoption of ChatGPT — taking just five days after launch to get to one million downloads/active users — highlights its potential. ChatGPT’s market potential depends almost entirely on a strong digital infrastructure foundation: high speed, low latency mobile networks (towers/spectrum); powerful, cloud-based and distributed processing power (data centers); and ubiquitous, nationwide broadband networks (fiber/spectrum). Our upcoming Quarterly Investment Perspective will feature more in depth discussion of artificial intelligence.

Exhibit 5: One Million User Timeline

Key takeaway: ChatGPT did not take long to reach 1 million users.

Key Takeaway: ChatGPT did not take long to reach 1 million users. Exhibit 5 is a bar chart comparing how long it took various companies to reach 1 million users: ChatGPT (5 days) Instagram (2.5 months), Spotify (5 months) Dropbox (7 months) Facebook (10 months) Foursquare (13 months) Twitter (2 years) Airbnb (2.5 years) Kickstarter (2.5 years), and Netflix (3.5 years). As of January 24, 2023. Source: Statista

Source: Statista

Conclusion

Demand for new services, cutting-edge applications, and innovative technologies is serving as a catalyst for investments in digital infrastructure. Funding from public and private markets has been complemented by policy initiatives and government investments too. The necessity and business imperative for universal broadband contributed to the 2021 passage of the Infrastructure Investment and Jobs Act (IIJA) in the U.S., which allocates $65 billion for investment into broadband. The compelling and unique features of digital infrastructure — recurring revenue streams typically with built-in escalators, high barriers to entry, and asset scarcity — all provide the opportunity for stable cash flows and attractive returns. Bessemer Trust’s investment professionals have developed a deep understanding of the opportunities, risks, and rewards of the digital infrastructure ecosystem and are sourcing and executing compelling investment opportunities for clients.

Investments in private real assets are for qualified investors only.

This material is for your general information. It does not take into account the particular investment objectives, financial situation, or needs of individual clients. This material is based upon information obtained from various sources that Bessemer Trust believes to be reliable, but Bessemer makes no representation or warranty with respect to the accuracy or completeness of such information. The views expressed herein do not constitute legal or tax advice; are current only as of the date indicated; and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. Bessemer Trust or its clients may have investments in the securities discussed herein, and this material does not constitute an investment recommendation by Bessemer Trust or an offering of such securities, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference.