Sustainable Investing: Aligning Your Values With Your Wealth Management Goals

- This paper provides an update on sustainable investing and Bessemer’s approach to it given the growing suite of opportunities in the space.

- We acknowledge the complexity and evolution of the sustainability space and believe that our Bessemer Sustainable Leaders portfolio incorporates both.

- Bessemer’s investment and philanthropy departments partner with each other to help clients develop and implement impact investing strategies, and integrate sustainability goals in their portfolios and private foundation endowments or donor-advised funds.

There has been an evolution in how the world thinks about the role that businesses and financial markets can play in advancing positive social, environmental, and governance outcomes. Against this backdrop, wealth holders have a growing suite of opportunities to align their values with their wealth management plans.

In this A Closer Look, we survey notable trends as they relate to sustainable investing and offer steps that interested clients can take to embrace values-driven wealth management innovations in investments and philanthropy.

Sustainability — The Evolution

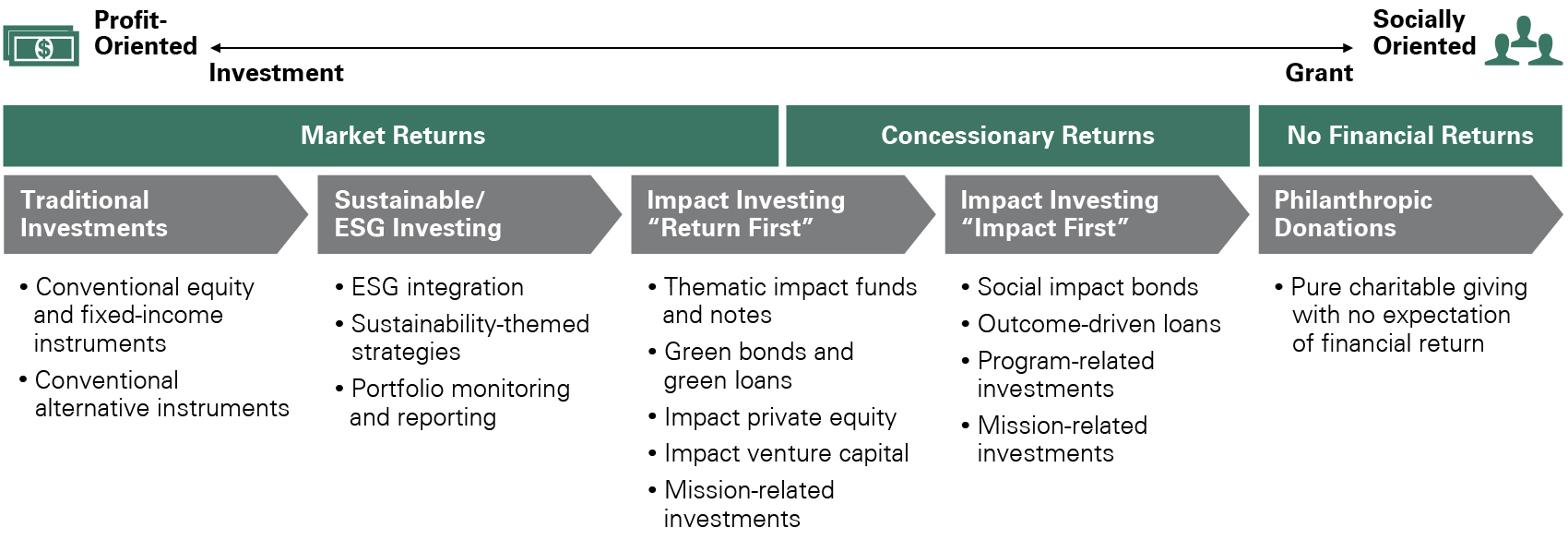

Various terms are used to describe sustainable investing, including socially responsible investing (SRI), ESG (environmental, social, and governance), and impact, among others. While there is some overlap across these terms, there are also important nuances (Exhibit 1). At a high level, there is a broad spectrum of objectives, ranging from traditional investments that are purely profit-driven with no ESG considerations to philanthropic donations that are socially oriented with no financial considerations. At its core, sustainable investing involves integrating ESG factors into fundamental investment analysis to the extent that they are material to investment performance.

While sustainable investing was once considered concessionary, or detrimental to returns, the space has evolved considerably over the past decade. Investing with ESG considerations, in public and private markets, is now considered an alpha generator and risk mitigator by many investors. For example, including ESG in financial analysis may provide insights on companies with good corporate governance, which benefits employees and shareholders as it may lead to increased productivity and stronger performance. Similarly, ESG uncovers global challenges and risks to companies, including climate change, corruption, data privacy, and unethical supply chains. Uncovering these opportunities and risks is a key reason why integrating ESG into investment processes has become more widely accepted by the institutional investment community — particularly as they may materially impact a company’s performance. Moreover, credible financial institutions continue to recognize the benefits as they incorporate ESG into their business models. For example, the CFA Institute has created a certificate for ESG investing, developed in consultation with the United Nations Principles for Responsible Investment. Lastly, as a part of the CFA Institute’s commitment to increasing awareness of ESG-related investment criteria, it has launched the first global voluntary ESG disclosure standards for investment products.

Exhibit 1: The Evolving Sustainable Investing Landscape

The Evolving Sustainable Investing Landscape

Sustainable investing continues to garner record asset flows globally. According to Bloomberg, global ESG assets are on track to exceed $53 trillion by 2025, representing more than a third of projected total assets under management. In private markets, Preqin reports an estimated $3 trillion of private assets managed by firms that are committed to ESG investing, representing 36% of the total private capital AUM globally. Flows in the U.S. in particular continue to break records, though they still lag those in Europe, which continues to dominate global flows.

Coupled with the increasing asset flow is the development of further transparency in reporting. Europe has taken meaningful steps to advance reporting, ahead of the U.S. and other countries. The goal of this reporting is to avoid greenwashing, or providing misleading information about sustainability goals or results, and to help educate retail investors. For example, the Sustainable Finance Disclosure Regulation (SFDR), which aims to ensure that European Union (EU) investors have the disclosures they need to make choices in line with their sustainability goals, was implemented in Europe in 2021. Under the rule, sustainability reporting is mandatory, and firms are required to disclose how ESG risks are considered; if they don’t take sustainability risks into consideration, they are required to provide their rationale. The Corporate Sustainability Reporting Directive proposal, which the European Commission plans to adopt in late 2022, will require approximately 49,000 large EU member state and European stock exchange-listed companies to report on sustainability standards likely beginning in 2024. International pressures ultimately prompted the U.S. SEC in 2021 to direct its Division of Corporation Finance to evaluate ways to enhance its focus on climate-related disclosure in public filings.

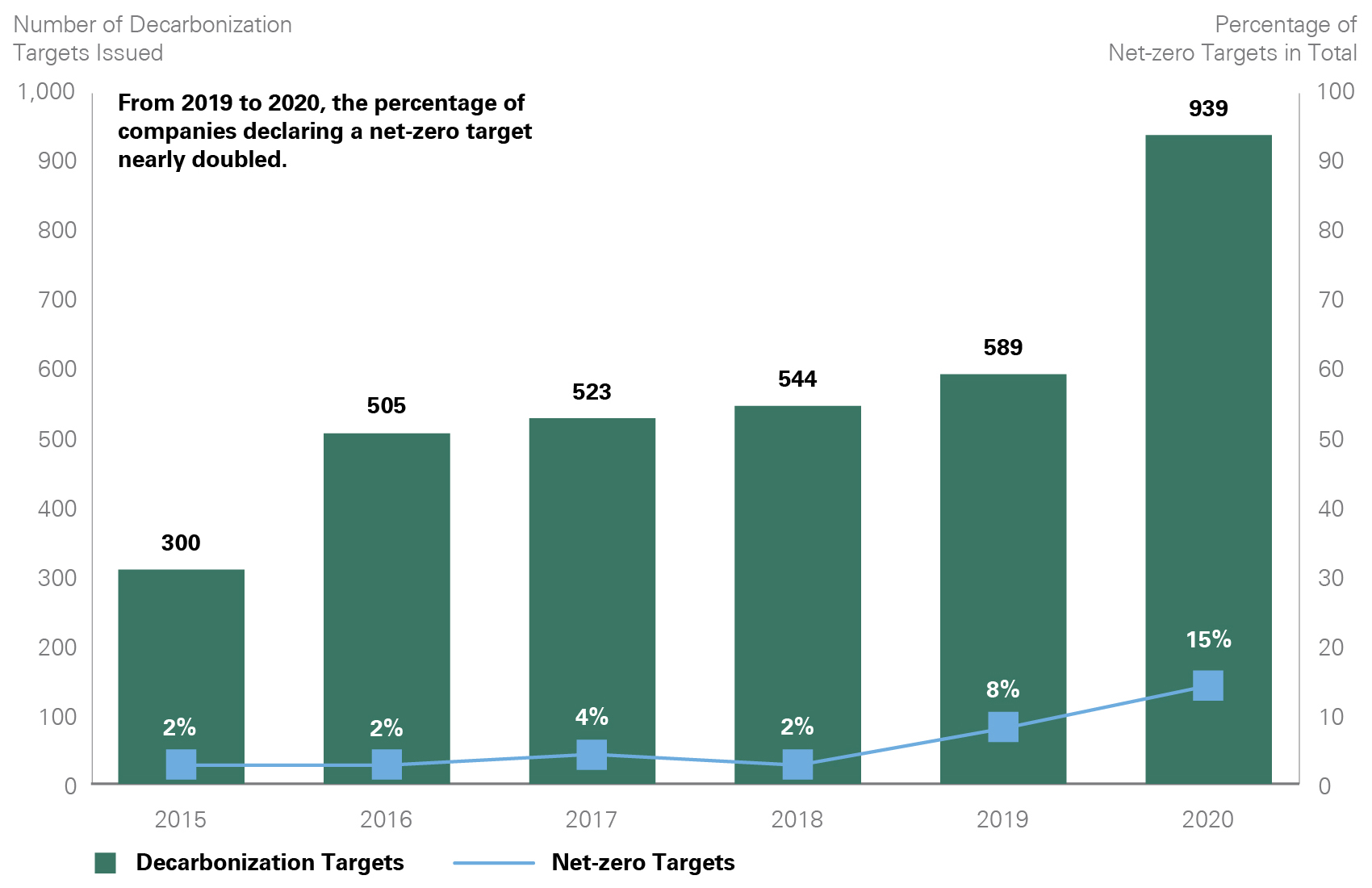

Exhibit 2: Decarbonization Targets Set by the World’s Publicly Listed Companies

Decarbonization Targets Set by the World’s

Publicly Listed Companies

Another major trend in sustainable investing is the call to the world’s largest companies to address climate change. The Paris Agreement — a legally binding international treaty on climate change formed in 2015 — has set the goal to limit global warming to well below 2 degrees Celsius, with an effort to reach below 1.5 degrees Celsius, compared to preindustrial levels. To reach these goals, companies are setting net-zero targets, or reducing carbon emissions to the greatest extent possible, and compensating for the remaining unavoidable emissions via removal. From 2019 to 2020, the percentage of companies declaring a net-zero target nearly doubled (Exhibit 2).

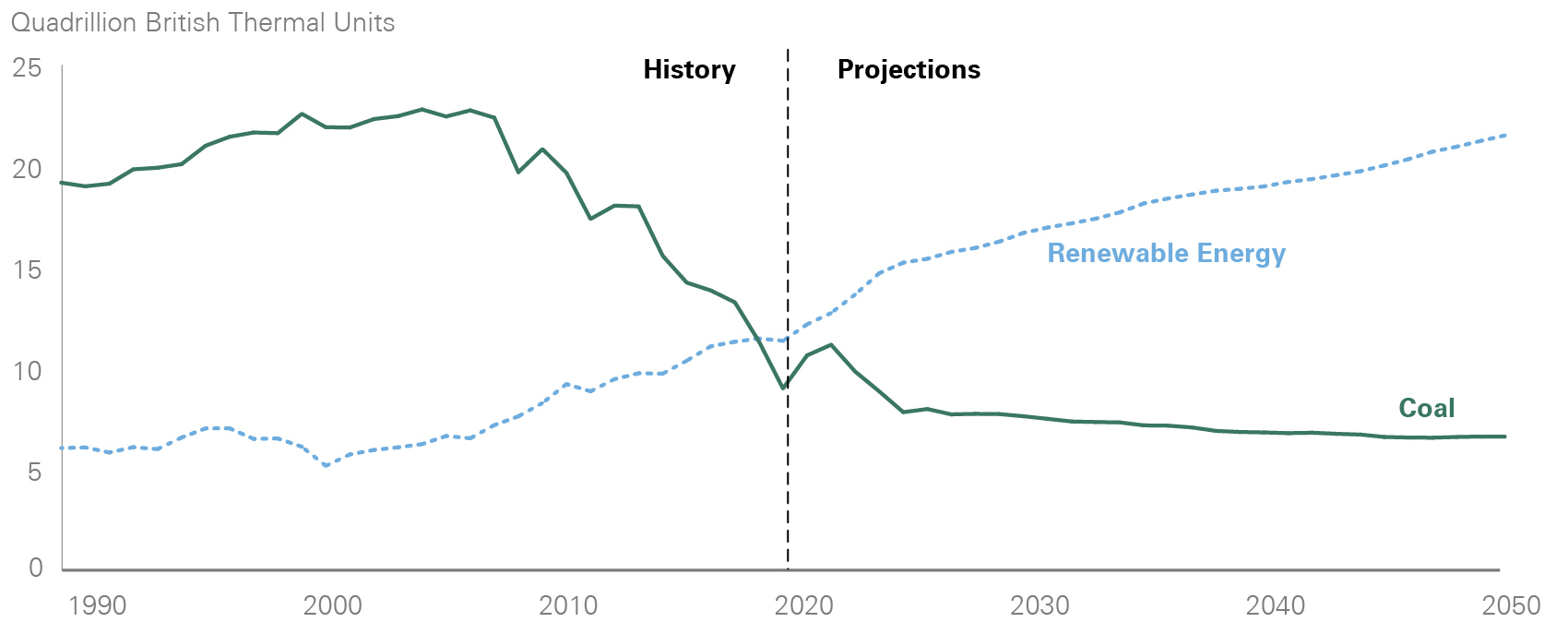

Even outside the Paris Agreement goals, data continues to show a projected transition toward cleaner energy. As shown in Exhibit 3, renewable energy consumption is expected to increase by 94% over the next 30 years. As noted on page 2, investment flows have followed this trend as well, and we note that climate-aware strategies are launching at an increasing rate, particularly in recent quarters.

Exhibit 3: Transition to Clean Energy Expected to Continue

Transition to Clean Energy Expected

to Continue

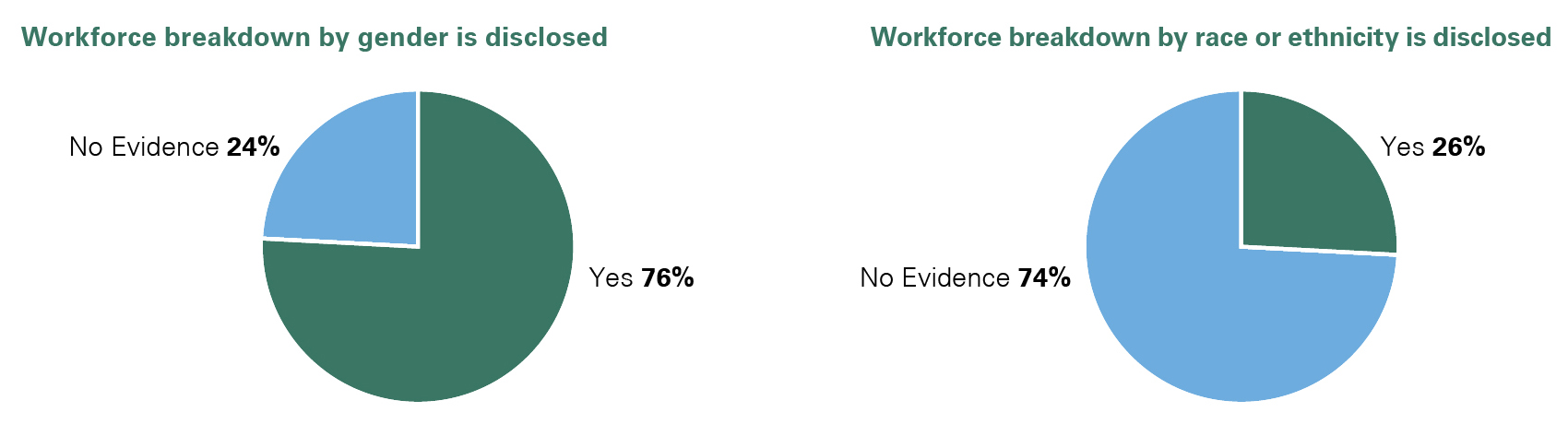

Another key sustainability issue that is gaining the attention of shareholders is diversity, equity, and inclusion (DEI) efforts, including having more diversity on boards and the workforce. Race and ethnicity disclosure severely lags gender disclosure in the workplace. While 76% of companies disclose gender diversity, only 26% of companies disclose race or ethnicity information (Exhibit 4). Shareholders are urging companies to increase their diversity on boards as well as to recruit and maintain diverse employees. A report by McKinsey & Company found that diverse companies perform better, as diversity increases productivity. A more productive workforce translates to higher profits, and diverse teams tend to be more creative and better at problem-solving.

Exhibit 4: Workforce Breakdowns by Gender and Race or Ethnicity

Workforce Breakdowns by Gender and Race or Ethnicity

Impact Investing — Philanthropy as an Entry Point

When clients embark on their journey to integrate their values and vision for the world with their finances, philanthropy is often a good starting point. As families set aside charitable dollars for impact and legacy rather than their living and livelihood, many of our clients are open to taking on greater risks with those dollars. Importantly, private foundations are conducive to experimentation because the investment goals and liquidity needs for meeting required charitable distributions are relatively modest. When set up for perpetuity, a foundation’s endowment can sustain its rate of consumption with an investment return of >5%, and the IRS has publicly encouraged U.S.-based private foundations to consider the relationship between their mission and investment practices. With these enabling factors in place, philanthropic institutions have been at the forefront of innovating and scaling mission-related investing across the spectrum illustrated in Exhibit 1.

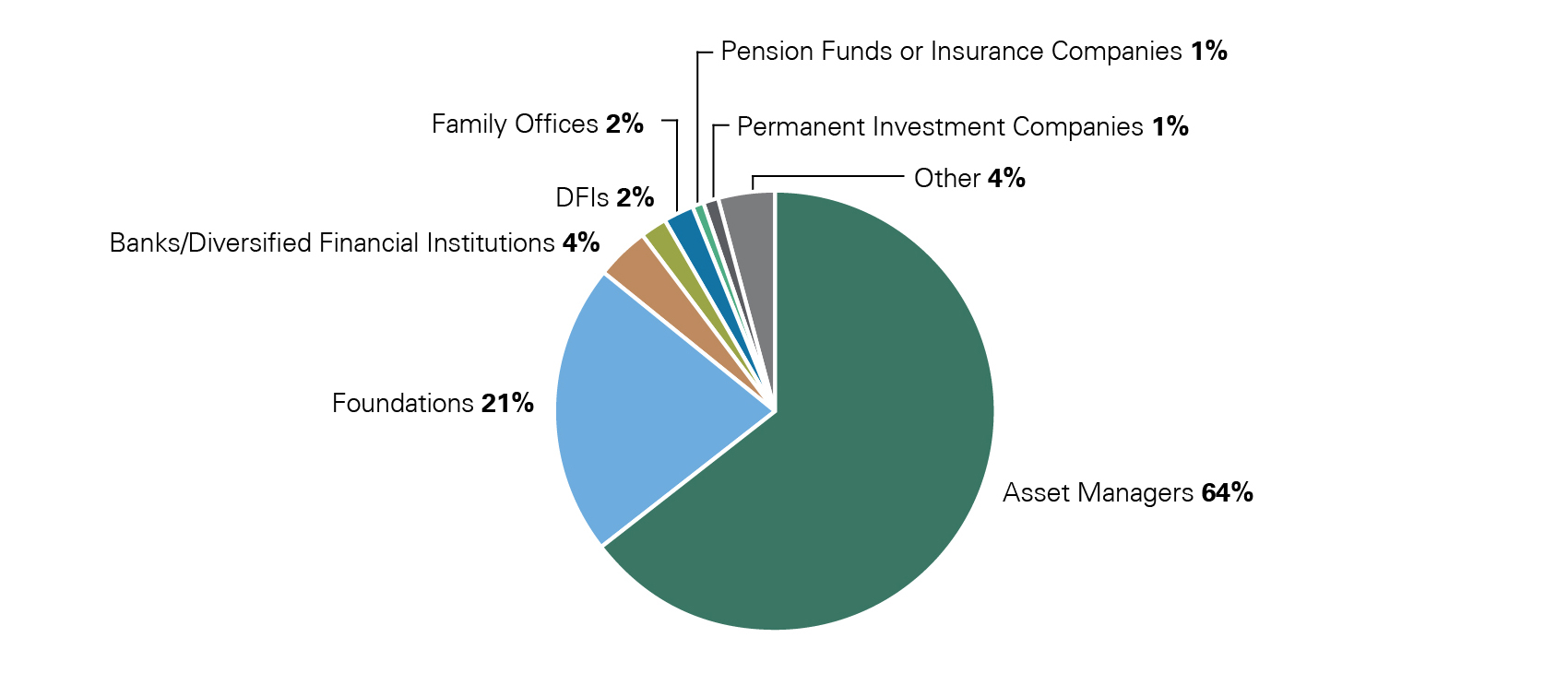

Today, sustainable investing is common among foundation endowments,1 and a growing number of philanthropic organizations are experimenting with “impact investments” (Exhibit 5). As defined by the Global Impact Investing Network (GIIN), a premier industry group, impact investments refer to investments that are intentionally designed to generate positive, measurable social and environmental impact alongside a financial return. According to this group, foundations account for 21% of all organizations actively engaged in impact investing worldwide — second to asset managers.

Exhibit 5: Impact Investing Organizations by Type

Impact Investing Organizations by Type

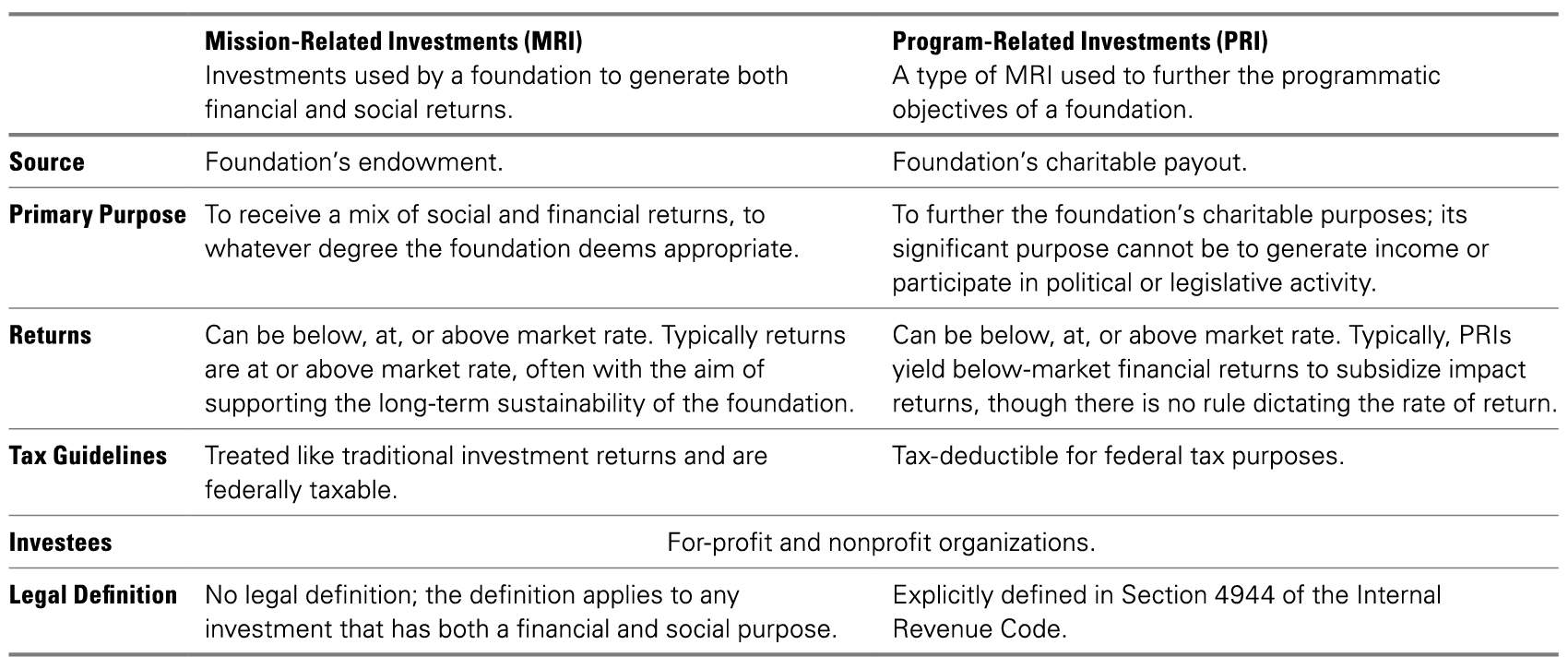

The most common instruments for impact investing are known as mission-related investments (MRIs) or program-related investments (PRIs), described in more detail in Exhibit 6. Mission-related investments refer to those made proactively from the corpus of a private foundation or another charitable vehicle. They can encompass “return first” and “impact first” investments depicted in Exhibit 1. Importantly, MRIs have no legal definition, which can make them relatively more flexible and easier to administer. An MRI is made from the corpus of a philanthropic organization and returns from the investment go back into the corpus with no special treatment or accounting. While philanthropists who pursue these investments must take care to follow “prudent investor” standards and avoid jeopardizing investments, this is relatively easy to do with a well-balanced portfolio.

Exhibit 6: Differences Between MRIs and PRIs

Differences Between MRIs and PRIs

Alternatively, program-related investments are legally defined in the Internal Revenue Code and must meet certain criteria to be recognized. By definition, they are “impact first” investments, made by private foundations with the primary purpose of furthering that foundation’s expressed charitable purpose. Most often, PRIs are subject to a more robust administrative process known as “expenditure responsibility,” which requires philanthropists to follow a thorough diligence and monitoring process. Notably, PRIs are considered, like grants, as charitable distributions and count toward a private foundation’s 5% minimum distribution requirement. They are made from the corpus of a private foundation and treated as a grant. When PRIs are returned, the funds must be redeployed for charitable purposes; they cannot be returned and reinvested with the foundation’s corpus. While PRIs require special administrative and accounting measures, many philanthropists continue to see PRIs as an attractive way to make their charitable dollars stretch further. After all, the investment return for a grant is always zero. PRIs are also popular among philanthropists who are focused on impacting a social or environmental problem they believe must be addressed by private markets.

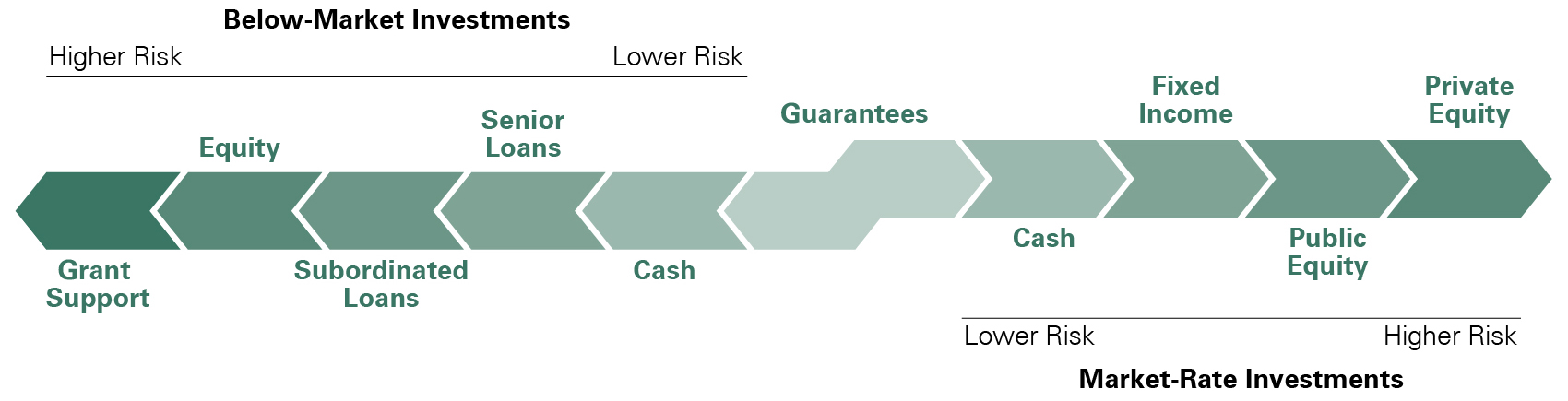

Both mission-related investments and program-related investments can be made using a variety of debt and equity instruments across many different asset classes. Exhibit 7 depicts the broad range of opportunities philanthropists can consider. As the field of impact investing has proliferated, so too has the breadth of investable opportunities. From supporting community development finance institutions to investing in impact funds or directly into a social enterprise, philanthropists have a high degree of optionality. Importantly, a number of communities have emerged to support philanthropists in navigating this space; groups like Mission Investors Exchange, Toniic, and The ImPact focus specifically on impact investing and other philanthropic industry groups that incorporate impact investing-focused education and programming in their broader service offerings.

Exhibit 7: Mission-Related Investment Continuum

Mission-Related Investment Continuum

Case Study: The F.B. Heron Foundation

The F.B. Heron Foundation began its impact investing journey in 1997. The organization’s charitable mission is to “help people and communities help themselves.” In 2012, the foundation committed to investing 100% of its assets in support of this charitable mission. At the time, the foundation’s assets were worth $250 million. Just four years later, the foundation reported full integration of impact screens across its investment portfolio valued at $273 million. Today, the Heron Foundation offers some great examples of impact investments in action.

Consider two examples from its portfolio:

- PRI: The foundation purchased a $350,000 limited partnership interest with a term of 10 years in Adena Ventures, a community development venture capital fund targeting the central Appalachian region. Adena’s mission is to increase the supply of equity and near-equity capital in the region in order to attract and retain businesses and to increase employment opportunities for residents.

- MRI: The foundation purchased “Linda Mae” bonds with an aggregate value of $750,000 issued by Habitat, the leading nonprofit developer of self-help housing for low-income and very low-income families. These bonds helped Habitat raise more than $43 million for its affiliates around the country.

Implementation and Effect on Results

Bessemer works with clients to align their values with their wealth management goals. For nearly a decade, the firm has provided investment solutions to clients focused on sustainability and supported them in their efforts to advance social and environmental impacts through their philanthropy. As the complex and dynamic sustainable finance industry evolves, wealth holders will continue to have greater opportunities to contribute to positive outcomes for people and the planet. Bessemer is committed to delivering comprehensive investment solutions and philanthropic advising to our clients.

A decade ago, client demand in the space was muted, but today it is energized and growing. Moreover, there has been a notable pickup in demand from multigenerational families. Client perspectives on this topic vary widely, and demand can vary significantly as well. We are excited to work with clients to deliver investment solutions that fit their personal interests.

Bessemer’s Director of Sustainable Investing and other colleagues work closely with Bessemer’s equity, fixed income, and alternative investment groups to advise them on the latest macro and sustainable investing trends. As Bessemer primarily invests in high-quality sustainably growing companies, the process lends itself to better than average ESG scores. High-quality companies are likely to have better long-term sustainability practices in addition to the potential to outperform the market over time. For example, high-quality companies have good economics that enable them to consistently invest in ESG initiatives over the long run. As transparency and standardization in reporting evolve, we look forward to understanding their implications, as a broad investment team.

Bessemer’s equity strategies are managed both internally and externally. The internally managed Bessemer Sustainable Leaders strategy employs a fundamentally driven investment process, using Bessemer internal research as the alpha source and sizing the positions for optimal relative risk/return characteristics with a focus on ESG leaders. The strategy seeks securities with sustainably growing, high-quality business models that exhibit attractive valuations, improving fundamentals, and strong ESG characteristics. Bessemer Sustainable Leaders provides transparency for clients and the ability to cater the strategy to individual sustainable goals. Complementing Bessemer Sustainable Leaders are external managers focused on areas such as climate change, water, and the “S” pillar of ESG.

We have relationships with third-party ESG service providers and leverage relevant datasets to understand the sustainability implications within our internal portfolios. As those providers evolve and strengthen their solutions, we will continue to leverage sustainability-related data to enhance our research processes. We are also in regular dialogue with industry leaders within the sustainable investing space, with many best-in-class external managers sharing ideas and trends. Discussions with select external managers have evolved to include their view of sustainability in their investment processes as well as in their day-to-day operations. With all our external managers, we ask about their diversity and inclusion efforts, ESG policies, and initiatives related to employee well-being and retention.

In alternative investments, Bessemer’s Real Assets team conducts comprehensive searches to identify both experienced and promising managers who are increasingly closed to new investors, by drawing from longstanding relationships and Bessemer’s reputation as a partner of choice. The team takes an opportunistic approach to investing in private markets by taking advantage of secular tailwinds, dislocations, and special situations. Themes and sectors of current focus include energy transition, infrastructure, real estate, and specialized agriculture, and we take a thoughtful approach to portfolio construction to diversify risk. Investment examples incorporating ESG include electrifying transport, enabling connectivity, and decarbonizing buildings and foods. The long-term orientation and physical nature of many real asset investments make ESG considerations especially important. The team integrates ESG and DEI factors into the due diligence process by considering questions developed by the Institutional Limited Partners Association (ILPA), which serves as an industry standard.

In philanthropy, our philanthropic advisors support clients to identify and pursue their impact investing goals. In partnership with investment colleagues, we help clients integrate ESG and sustainable investments in their private foundation endowments or donor-advised funds. Through Bessemer Giving Fund, our in-house donor-advised fund, we can support clients directly to execute program-related investments and other traditional grant alternatives. We also advise clients to develop and implement impact investing strategies, leveraging our vast network of thought leaders, vendors, peer communities, and forums to help them along their impact investing journey.

Conclusion

We continue to stay abreast of sustainable investing developments and weigh different types of solutions for clients. If you are interested in sustainable investing, please speak with your Bessemer advisor about what sustainable investing means to you and how we can be of service.

- According to 2020 research published by the Council on Foundations, 19% of foundations surveyed nationally report integrating ESG criteria in their endowment investment decisions. Within this group, 20% of foundations reported a practice of screening out investments that are inconsistent with the institution’s mission, up from 12% just two years prior.

This material is for your general information. It does not take into account the particular investment objectives, financial situation, or needs of individual clients. This material is based upon information obtained from various sources that Bessemer Trust believes to be reliable, but Bessemer makes no representation or warranty with respect to the accuracy or completeness of such information. Views expressed herein are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. Bessemer Trust or its clients may have investments in the securities discussed herein, and this material does not constitute an investment recommendation by Bessemer Trust or an offering of such securities, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Private equity investments are not suitable for all clients.