Estate Planning Basics

What is estate planning, and why does it matter?

Why Do Estate Planning?

Estate planning is the process of thinking through choices, and is best done as part of a thoughtful, realistic analysis, rather than relying on the default estate plan provided by state law. The state law default plan (“one size fits all”) rarely reflects what any individual client would want.

Effective planning includes consideration of three major questions:

- What if I pass away tomorrow?

- What if I live for a long time?

- What if I become disabled?

Each of these questions triggers follow-up questions:

- Who will handle things when I cannot?

- What will happen to my assets?

A natural follow-up to basic estate planning is lifetime gift planning. This summary, however, focuses on basic estate planning.

Last Will and Testament (“Will”)

Your will serves several purposes, including designating an executor or personal representative of your probate estate, disposing of estate assets, and, if applicable, designating a guardian for your minor children.

In the absence of a will, state law will provide a dispositive plan for your assets and determine a priority for interested parties to act as administrator of your probate estate and as guardian of your minor children. Appointment of the guardian and administrator would be by probate court proceeding with the decisions made by the judge.

1. Assets Transferred by Will

Your “probate estate” generally consists of assets titled in your individual name that do not have a beneficiary designation. Assets titled in trust or that have their own beneficiary designation (such as life insurance policies or retirement accounts) will generally be distributed outside of the probate process. Jointly held assets with rights of survivorship will generally be transferred by operation of law directly to the surviving joint tenant.

2. “Control Parties” Designated by Will

Your will would identify who should administer the will, known as your executor or personal representative.

In addition, if you have minor children, your will would designate one or more individuals to act as guardian of your minor children. These persons care for your minor children after your death.

3. Typical Structure of a Will

If your plan includes a revocable trust, your will would typically provide that any assets that have not been transferred to the revocable trust during your lifetime “pour over” to (i.e., will be transferred to) your revocable trust at your death. Even in cases where a person fully funds his or her revocable trust, it is common for a will to identify the individual’s desired disposition of his or her tangible personal property (such as artwork, jewelry, furniture, and clothing).

If your plan does not include a revocable trust, your will describes the disposition of your assets (involving the same issues discussed in "5. Disposition of Your Assets" in the Revocable Trust section below).

4. The Probate Process

The process of probating (proving) a will following death can be quite simple and fast, or it can be cumbersome and slow, depending upon the state of residence and numerous other factors.

The executor or personal representative typically has no legal authority to act for your estate and protect your property until the appropriate court admits the will to “probate” and formally appoints the executor or personal representative. While this process is sometimes completed quickly and without much cost, especially where all persons interested in the estate are in agreement and are available to sign the required documentation, there can still be delays.

If a person has placed most of his or her assets in a revocable trust prior to death and where there are no minor children, probate administration may not be necessary.

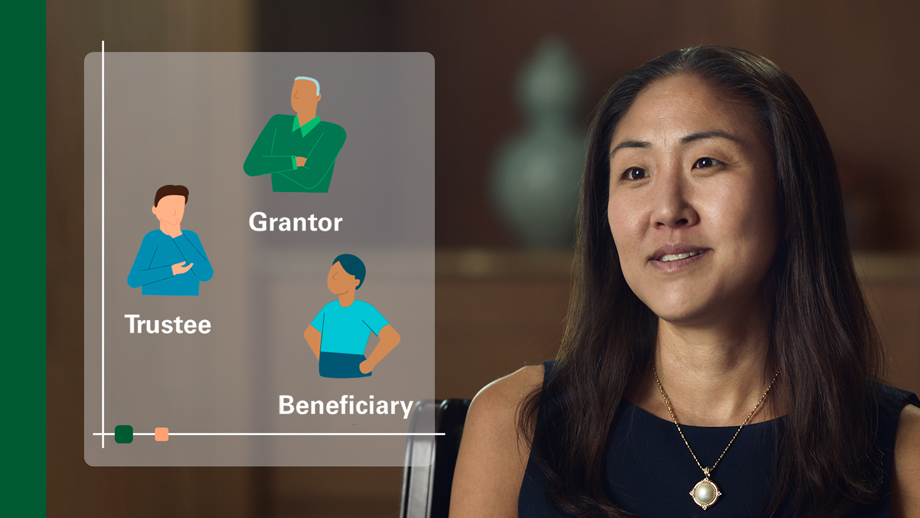

Revocable Trust

Your revocable trust (if your plan includes a revocable trust) is generally the primary document that disposes of your assets. This often includes the structure for continuing trusts for children and further descendants.

1. Probate Avoidance or Minimization

As discussed above, assets titled in the name of your revocable trust are not subject to the probate process. Accordingly, in many states, probate can be avoided by creating a revocable trust and transferring most of your assets to the trust during lifetime.

If you own real estate in other states, titling it in the name of the revocable trust can result in the avoidance of “ancillary probate” proceedings in the other states. Real estate held directly upon death must generally be transferred through a local probate proceeding. This can mean that separate court proceedings are required in each state where the decedent owned real estate, with the attendant costs (and possible delays) associated with those additional proceedings.

2. Privacy

During the probate process, your will is filed with the court and becomes a public document. However, in most states, the revocable trust is not filed and should not become a public document. By using a revocable trust as the primary document to dispose of your assets, little information relating to your estate plan would generally become publicly available.

3. Protection During Incapacity

If you become unable to manage your financial affairs, the successor trustee will continue to administer the revocable trust assets for your benefit until your recovery or death.

4. Basic Structure of a Revocable Trust

As the name implies, you, as the grantor (sometimes called the settlor or trustor) retain full control over your trust and the ability to change the terms of the trust, or to revoke the trust entirely, as long as you are living and have capacity to manage your assets. Therefore, unlike an irrevocable trust, you can change your mind as to any aspect of your trust at any time in the future.

You may serve as the sole trustee during your lifetime, with complete control over all investments, distributions, etc. Unlike a beneficiary of an irrevocable trust created by someone else, there is no issue with you serving as trustee, because the trust provides you with no tax or creditor benefits. You may also name someone else as trustee, but retain the ability to remove and replace the trustee at any time.

Spouses usually create “joint” trusts in the nine “community property” states, and separate trusts in the remaining “common law” states.

During your lifetime and as long as you retain capacity, the trustee (you or someone else of your choosing) will manage the revocable trust property as you direct, and will distribute income and principal of the revocable trust to you or for your benefit or otherwise as you direct.

If you become incapacitated, your successor trustee will manage the revocable trust assets for your benefit (and often for the benefit of your spouse) until your recovery or death.

At your death, the revocable trust will become irrevocable, and the revocable trust property, including any property passing to the revocable trust under your pour-over will or outside of probate (e.g., life insurance proceeds), will be distributed as you have provided.

5. Disposition of Your Assets

Through the process of developing your revocable trust, there are some questions you will have to answer:

- What party or parties will benefit? This usually includes a surviving spouse and descendants, and may also include charitable beneficiaries or others.

- When and how will the beneficiary or beneficiaries receive distributions? Trusts can provide guidance to your beneficiaries and can help protect the trust assets even after you are no longer living.

- How much should be distributed today versus how much in the future? Under what circumstances should the trustee make (or not make) distributions to the beneficiaries?

6. Choosing a Trustee

Choosing your successor trustee(s) is extremely important. The trustee will have major responsibilities for trust investments, supervising administration and making crucial distribution decisions for the beneficiaries. The trustee exercises discretion in all of these matters and has a fiduciary duty to the beneficiaries to act only in the best interest of the beneficiaries.

Power of Attorney for Property

You should have a power of attorney for property (sometimes called a durable power of attorney, a general power of attorney, or a financial power of attorney), whereby you, as principal, name someone else as your financial agent (also sometimes called an attorney-in-fact), who is authorized to manage your financial affairs, including to pay bills, manage investments, and transfer property to your revocable trust. A power of attorney for property may be effective immediately, even while you have full capacity, or it may be effective only if you become incapacitated.

Note that the agent under the power of attorney for property would have authority over your personal assets (e.g., an IRA), but not over any assets held in your revocable trust.

Power of Attorney for Health Care

You should have a power of attorney for health care (sometimes called a health care proxy or advance directive), designating a health care agent who is authorized to make medical and personal care decisions for you if you cannot make those decisions for yourself. These decisions include administration of medical treatments, admission to hospitals, application to and communication with insurance carriers, and continuation of life-sustaining treatment in the event of a terminal condition.

A health care power of attorney often grants your health care agent the authority to review and release your “protected health information” and can set forth any special instructions regarding particular types of care you should or should not receive.

Living Will

You should have a living will, also sometimes referred to as an advance directive, to express your wishes regarding the administration or withholding of artificial life support, nourishment, hydration, etc, where there is no expectation of recovery. In some states, this document is separate from a power of attorney for health care and, in others, they are part of the same document.

Health Care Disclosure

A health care disclosure or HIPAA release document should be executed by you to authorize your health care providers to disclose your medical information to those family members or other individuals that you designate. Without this authorization, your health care providers may be prohibited from sharing such information as a result of the implementation of certain privacy requirements under the Health Insurance Portability and Accountability Act of 1996 (HIPAA).

This summary is for your general information. The discussion of any estate planning alternatives and other observations herein are not intended as legal or tax advice and do not take into account the particular estate planning objectives, financial situation, or needs of individual clients. This summary is based upon information obtained from various sources that Bessemer believes to be reliable, but Bessemer makes no representation or warranty with respect to the accuracy or completeness of such information. Views expressed herein are current only as of the date indicated, and are subject to change without notice.