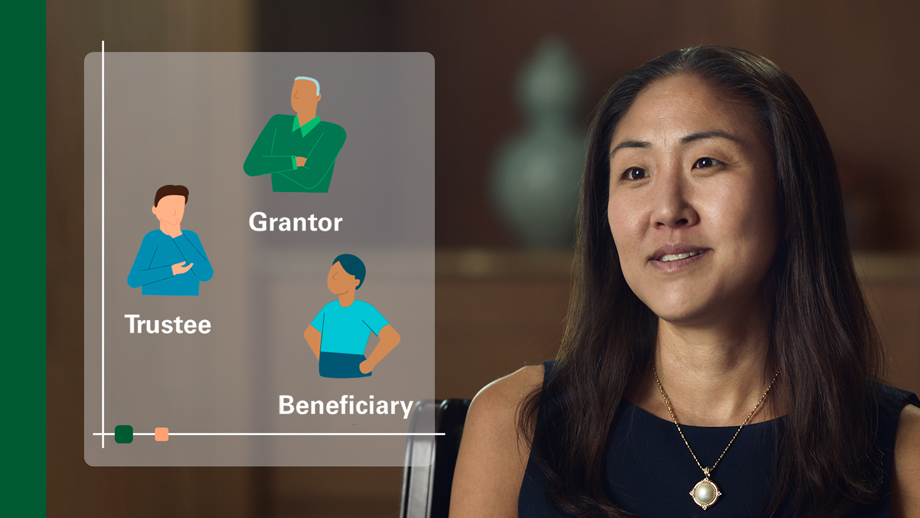

Revocable Trust

The basics of these trusts that can be cancelled at any time and for which you can serve as grantor, beneficiary, and even trustee.

Purpose

A revocable trust, sometimes known as a “living trust” or “revocable living trust,” allows a trustee of your choosing to administer your assets and use them for your needs if you become unable to manage the assets during your lifetime. In addition, any assets held by the trust at the time of your death will avoid probate, a process by which state courts oversee the administration of your estate.

Description

You create a trust of which you are the beneficiary during your lifetime. Pursuant to the terms of the trust, you can direct how the income and principal are to be paid during your lifetime, or the trustee may have the discretion to pay income and principal to you or on your behalf. You reserve the right to amend the trust, change it, or revoke it at any time. Upon your death, the trust can serve as a “will substitute”: the assets in the trust can be distributed to — or placed in a trust for — your intended beneficiaries. A revocable trust is often accompanied by a “pour over” will, which dictates that any assets owned in your name at your death will be distributed to the trustees of your revocable trust.

If you wish, you can serve as your own trustee during your lifetime. If you become incapacitated, the successor trustee (or trustees) you have selected will continue to manage the assets for your benefit. The trust may also provide that the trustee can use the assets to care for your spouse or others dependent on you, and to make gifts.

Funding

You may transfer a variety of assets, including liquid assets, closely held stock, tangible personal property, and real estate. In fact, you must transfer property into the trust if you wish for the trust to effectively manage assets for your benefit during your lifetime. That is because the trustee must have something to manage. Similarly, only assets held in the name of the trust at the time of your death will actually avoid probate.

Suitability

In general, a revocable trust may be appropriate if you:

- Are concerned that you may become incapacitated and want to ensure that your assets will be managed for your benefit.

- Have a lifestyle that makes managing your own assets difficult or inconvenient.

- Are inexperienced in investment management and wish for someone else to manage the assets for you.

- Own real property in more than one state and wish to avoid probate in one or more of those states at your death. (However, in some states, a revocable trust by itself may not accomplish this: see “Disadvantages.”)

- Wish to avoid probate for any other reason, such as cost savings or privacy concerns.

- Wish to avoid judicial supervision of any continuing trusts that may be created after your death.

Advantages

Consolidation of assets and ease of administration. You can transfer multiple accounts and assets to your revocable trust, allowing straightforward administration of those assets for your benefit. Thus, if you become incapacitated, all the assets can be managed immediately for your benefit by the trustees. This eliminates the challenge and delay of forcing an agent who is acting under a durable power of attorney to try to collect your assets from multiple financial institutions.

Avoidance of probate. Assets that fund the trust will avoid the probate process. Probate is a public process and may be costly and time-consuming as well. An involved probate process may result in delayed distributions to beneficiaries.

Disadvantages

Not a tax-savings device. Using a revocable trust does not let you avoid income, gift, estate, or generation-skipping transfer taxes. You will continue to be taxed on the income generated by the trust during your lifetime. Because you retain the right to amend or revoke the trust, the trust’s assets will be included in your estate for tax purposes at your death.

Varies from state to state. In some states, revocable trusts by themselves won’t necessarily exempt your estate from the probate process.

Not an asset-protection device. The revocable trust does not provide asset protection.

Other Considerations

Joint revocable trusts. If you live in a community-property state and are married, you and your spouse may wish to create a joint revocable trust to consolidate your assets and to keep track more easily of your community property and separate property. If you later move out of the community-property state to a common law property state, you may wish to keep the joint revocable trust in existence to preserve the community-property status of the assets.

Example

Jane, a 73-year-old widow, has a $40 million portfolio and two homes, one in New York and one in New Hampshire. She is retired with many activities and hobbies, and is actively involved in her financial affairs. She is concerned, however, that if something happens to her health, no one will be available to oversee her assets. On her death, she wants the assets to pass to trusts for her son, Charles, and his daughter, Julie.

To provide for her possible future incapacity and to spare Charles and Julie the time and financial burden of a probate process carried out in two states at her death, Jane sets up a revocable trust, naming herself as the initial trustee and Bessemer as the successor trustee, to serve in the event she is unable to act as trustee. Jane titles her investment management accounts and both houses in the name of the revocable trust. Should Jane become incapacitated, Bessemer, as successor trustee, would manage the assets for Jane’s benefit. Following her death, trusts would be established for the benefit of Charles and Julie, without the need for a lengthy probate process.

This summary is for your general information. The discussion of any estate planning alternatives and other observations herein are not intended as legal or tax advice and do not take into account the particular estate planning objectives, financial situation, or needs of individual clients. This summary is based upon information obtained from various sources that Bessemer believes to be reliable, but Bessemer makes no representation or warranty with respect to the accuracy or completeness of such information. Views expressed herein are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in law, regulation, interest rates, and inflation.