Executive Summary

- AI is likely to reshape work meaningfully, but not all at once. While capabilities are advancing rapidly, real-world adoption will be constrained by infrastructure, cost, regulation, and human behavior, leading to uneven and incremental change.

- History suggests that work is more likely to be disrupted than to disappear. Technological advances tend to augment productivity and shift labor demand rather than eliminate it outright, though the transition can create meaningful dislocation across industries and skill levels.

- Our portfolio positioning is designed to capture opportunity while navigating market volatility. We have selectively added to high-quality software and cybersecurity companies following recent weakness, focusing on businesses with durable platforms and strong positioning in an AI-driven economy.

The start of 2026 has been shaped by two forces dominating headlines and investor sentiment: geopolitical tension and rapid advances in artificial intelligence. We recognize that recent market volatility has heightened uncertainty for many investors. While we address near-term market developments in our Weekly Investment Update and our latest market update video, this Quarterly Investment Perspective focuses on artificial intelligence (AI), specifically its potential implications for the labor market, the nature of work, and the pace at which technological change may reshape the economy.

In an environment where the most extreme viewpoints often dominate the conversation, our aim is to focus on what we believe is most likely: AI will drive meaningful change, but its impact will unfold unevenly, creating both disruption and opportunity. Recent volatility in software valuations reflects how quickly sentiment can shift as markets attempt to price uncertainty.

AI has become less a technology discussion and more a cultural Rorschach test. Ask 10 people what AI means for society, and you are likely to hear one of two answers: It will either usher in an age of unprecedented prosperity or trigger systemic collapse. The incremental middle ground is often overshadowed.

One reason AI provokes such polarized reactions is that it is not merely another communication technology. The internet transformed how information and services move; AI is beginning to reshape how work itself gets done. It targets cognitive labor, including drafting, analysis, decision support, and workflow execution, functions that historically sat inside the human mind rather than inside machines.

The Myth of Sudden Transformation

A persistent misconception about AI is that change will be abrupt and sweeping. History suggests otherwise. Major technologies rarely replace entire systems overnight. Instead, they diffuse gradually and unevenly, filtered through institutions that adapt in fits and starts.

Electricity did not instantly reorganize the economy. The internet did not eliminate all intermediaries. Even transformative technologies are constrained by factors such as regulation, human nature, labor markets, and legacy infrastructure.

In our view, AI is likely to follow a similar path. It will reshape workflows and compress certain functions. It will augment some workers and displace others, as we are beginning to see in early, though still limited, cases (Exhibit 1). It will create new roles that are difficult to foresee. But these shifts will unfold within the constraints of regulation, capital allocation, and human habits.

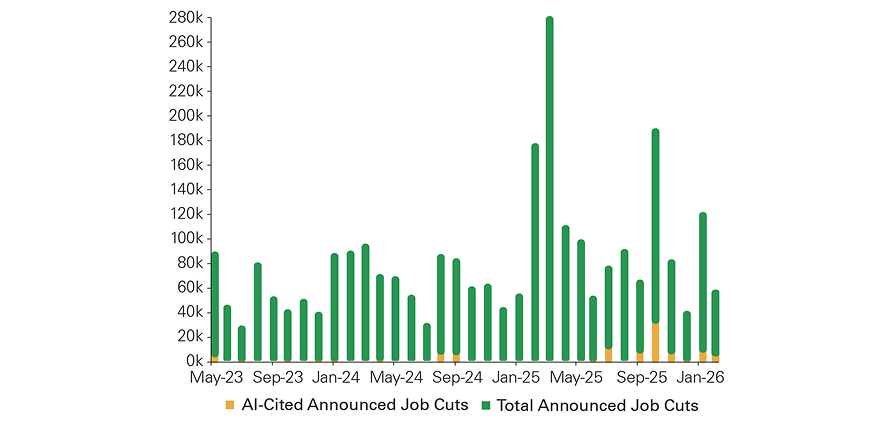

Exhibit 1: Total Monthly Job Cut Announcements vs. AI-Cited Job Cut Announcements

Key takeaway: While the magnitude remains modest, AI-related displacement is beginning to increase.

While the magnitude remains modest, AI-related displacement is beginning to increase.

The Incentive to Tell Extreme Stories

In modern information markets, attention is the most valuable currency. Extreme narratives travel faster than nuanced ones. Claims that “everything will change” or “this will destroy everything” tend to outperform more measured views of gradual, uneven change. The algorithms that now curate most of our information tend to amplify the extremes.

For technologists and investors, the utopian narrative can unlock capital and policy support. Framing AI as the most transformative innovation in history attracts urgency and resources. For critics, policymakers, and institutions wary of disruption, dystopian framing fuels the desire for regulation and caution.

Beyond incentives, human psychology plays a central role. Technological change introduces uncertainty, and uncertainty can activate fear.

When people sense that a tool might rival or exceed their core skills, the fear response tends to intensify. Dystopian narratives externalize that fear into grand stories of job loss, power concentration, or loss of agency. Utopian narratives, by contrast, channel the same uncertainty into hope, including liberation from drudgery, exponential productivity, and new frontiers of knowledge.

Both reactions are understandable. Yet each, on its own, is incomplete.

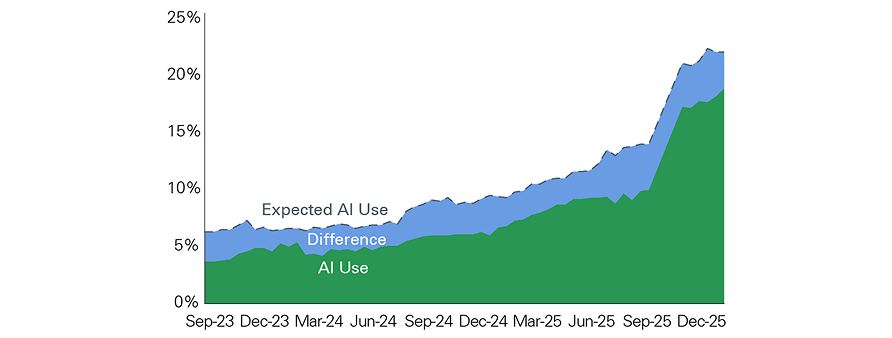

Historically, diffusion has followed an S-curve. Early adoption is slow and expensive, then accelerates as costs fall and complementary infrastructure matures, and finally decelerates as integration costs rise and marginal returns diminish. AI seems to be following this trend as adoption rates remain low but are accelerating (Exhibit 2). AI adds another layer of friction because enterprise deployment is not a consumer app download. It requires governance, compliance, security, and workflow redesign. In practice, this creates a gap between capability and adoption. Improvements in AI models do not automatically translate into widespread real-world adoption. Capability can improve exponentially while adoption proceeds incrementally.

The most probable future lies between apocalypse and utopia. More likely, it will be defined by friction.

Exhibit 2: Census Bureau AI Adoption vs. Potential AI Adoption

Key takeaway: Despite relatively low levels of AI adoption, trends indicate steady growth ahead.

Despite relatively low levels of AI adoption, trends indicate steady growth ahead.

An additional constraint that tempers the idea of sudden, economy-wide displacement is physical infrastructure, particularly energy generation and regulatory capacity. Advanced AI systems run on data centers that require enormous and reliable power. At first glance, improvements in model efficiency, and the resulting decline in the cost per unit of computation, might suggest that overall demand for compute would fall. If each task requires fewer resources, the total need for computing power should decline. In practice, however, the opposite tends to occur. As costs fall, adoption expands across industries and consumer applications, driving a significant increase in overall demand for computation. Marginal cost does not necessarily reduce aggregate resource use when adoption scales rapidly; it often increases it.

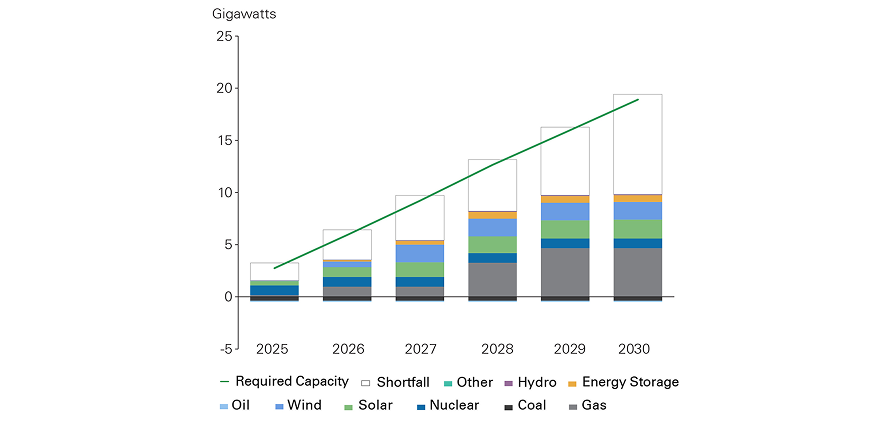

That dynamic implies sustained pressure on electricity generation, grid modernization, semiconductor supply chains, and permitting processes. These systems do not adjust overnight. They require capital and regulatory support. Energy availability and infrastructure buildout therefore act as natural pacing mechanisms, making a sudden, all-at-once labor displacement scenario less structurally plausible (Exhibit 3). Large-scale labor substitution would require a significant increase in electricity and infrastructure supply – which won’t happen overnight.

Exhibit 3: Data Center Electricity Demand vs. Power Capacity, 2025–2030

Key takeaway: AI power demand is rising, but it is constrained by the pace of electricity expansion.

AI power demand is rising, but it is constrained by the pace of electricity expansion.

As demand for automation rises, the total cost of compute can rise with it through chips, power infrastructure, and energy. Where the marginal cost of compute exceeds the marginal cost of human labor, substitution becomes economically irrational. This does not suggest AI will stall; rather, it underscores that deployment is governed not only by algorithms but also by input costs.

Ironically, resistance to data center construction in parts of the U.S. risks shifting both capital and value creation abroad. Because digital services operate globally, capital will migrate toward jurisdictions that offer predictable permitting and regulatory clarity. A more coherent strategy would pair responsible data center expansion with energy investment and environmental standards, ensuring the economic gains from AI infrastructure accrue domestically rather than offshore.

The most persistent fear surrounding artificial intelligence is not about software margins or capital allocation. It is about work itself. Will AI eliminate jobs at scale? Will it make large portions of the population economically redundant? These fears feel new because the technology feels new. In reality, the concern can be found throughout history.

In a recent column,* economist Paul Krugman revisited this debate and emphasized a core point long supported by economic theory: There is little evidence that technological progress eliminates work across the entire economy. As he argues, predictions of permanent, economy-wide job destruction have been made repeatedly, and repeatedly proven wrong.

The fear itself has deep roots. In 1930, British economist John Maynard Keynes introduced the term “technological unemployment,” warning that advances in productivity might outpace our ability to create new uses for labor. Two decades later, Kurt Vonnegut’s 1950 novel “Player Piano” imagined a future in which machines had displaced nearly all human workers, leaving society stratified and unstable. Each generation has projected its most advanced machinery into a dystopian labor narrative.

Yet the historical record tells a different story.

Today, output per hour worked in the U.S. is roughly five times higher than it was in the mid-20th century. By any measure, automation has transformed agriculture, manufacturing, logistics, and information processing. And yet employment among prime-age adults remains robust. More than 80% of Americans between the ages of 25 and 54 are employed, a higher share than in the mid-century era.

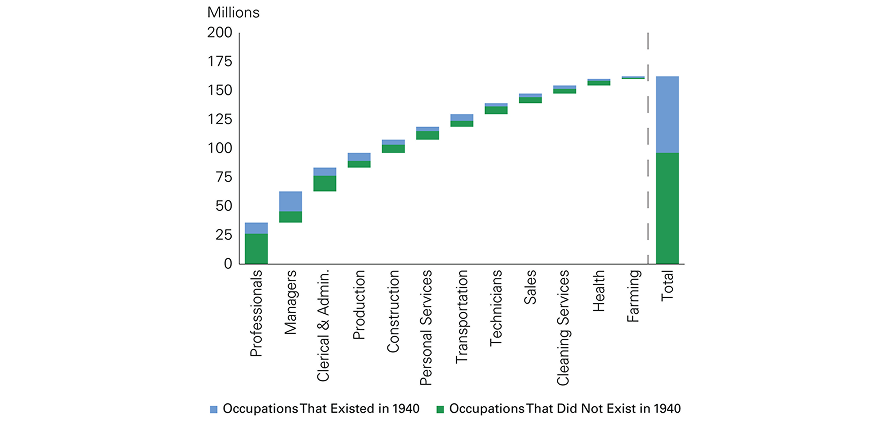

At the same time, the structure of work has changed dramatically: About 60% of workers today are in jobs that did not exist in 1940 (Exhibit 4), though the existence of work itself has not disappeared.

Exhibit 4: Employment by New and Preexisting Occupations

Key takeaway: Technological innovation drives employment growth over time.

Technological innovation drives employment growth over time.

Krugman attributes recurring fears of technological joblessness to what economists call the “lump of labor fallacy,” the mistaken assumption that there is a fixed quantity of work to be done in an economy; if machines perform more tasks, fewer jobs must remain for humans. In reality, labor demand expands with productivity, rising incomes, and evolving preferences.

The transformation of consumption over the past 70 years illustrates the point. The average new American home is now more than two and a half times the size of homes built in the mid-century era, even as household sizes have declined. Car ownership, once a marker of affluence, is now nearly universal, and two-car households are more common. Children possess smartphones and personal computers, which would have seemed fantastical decades ago. Entire industries, from digital advertising to cloud computing to streaming entertainment, did not exist in their current form a generation ago.

These expansions were not inevitable. They emerged because productivity gains lowered costs and unlocked new categories of demand. As societies grow wealthier, they rarely declare themselves materially satisfied. Instead, they redefine what constitutes a baseline standard of living, continually pushing the consumption boundary.

There is little reason to believe that AI will abruptly reverse this pattern. If anything, it may accelerate it. By reducing the cost of cognitive tasks, AI systems can increase overall productivity. Higher productivity, in turn, can raise real incomes and expand consumption possibilities. New services, experiences, and forms of customization may emerge, many of which will require human oversight.

The near-term labor impact is therefore more likely to resemble augmentation than elimination. In many workflow-heavy roles, the function persists but becomes less labor intensive: fewer employees per unit of output, higher throughput for remaining workers, and a shift in tasks toward oversight, exception handling, and relationship-heavy work. In practice, this increasingly means AI agents operating alongside human workers within enterprise systems, creating a parallel digital workforce.

At the macro level, this dynamic is consistent with slower unit labor cost growth in affected occupations, margin expansion in labor-intensive service businesses, and greater wage dispersion between AI-complementary workers, who become more productive, and AI-substitutable workers, whose tasks become cheaper to replicate. Over time, these shifts may alter the balance between labor and capital income. Industrialization shifted value toward physical capital; the internet concentrated value in platforms. AI may increase returns to compute infrastructure, model development, and workflow control, even as real wages rise through productivity gains. The ultimate distributional outcome will depend less on the technology itself and more on company-level winners and losers and regulatory policy.

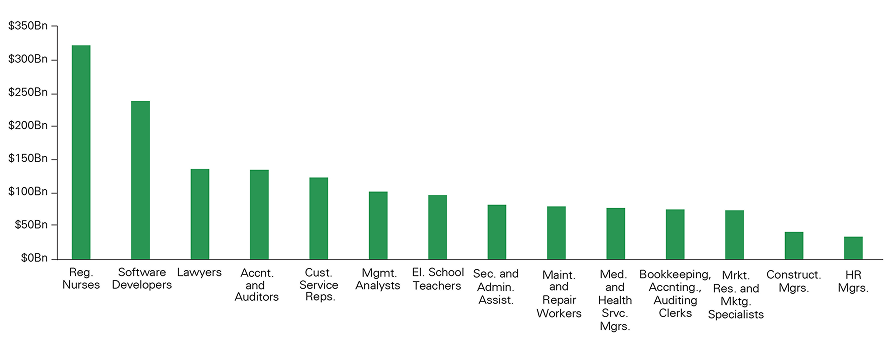

For AI to reshape the economy meaningfully, it must be used within the largest pools of labor income. Using Bureau of Labor Statistics employment and wage data, the largest wage pools sit in services-heavy, cognitive or semi-cognitive occupations, including healthcare, software development, legal services, accounting, customer support, and management analysis (Exhibit 5). This framing matters because the economic opportunity in AI is less about expanding a roughly $600 billion software market and more about augmenting or partially automating workflows embedded in a roughly $10 trillion services and labor market. In that sense, service-as-software, which transforms traditional human-delivered services into automated software solutions, may ultimately represent a larger opportunity than traditional software-as-a-service, a subscription-based method of software delivery and licensing.

Exhibit 5: Total Addressable Market by Job Sector

Key takeaway: The largest job markets are people-intensive, underscoring that much of the real economy will remain difficult to automate.

The largest job markets are people-intensive, underscoring that much of the real economy will remain difficult to automate.

This does not imply that the transition will be seamless. Technological change can be deeply disruptive at the occupational and regional level. Tasks can disappear faster than workers can retrain, and wage polarization can intensify if relevant skills are scarce.

Disruption does not mean elimination.

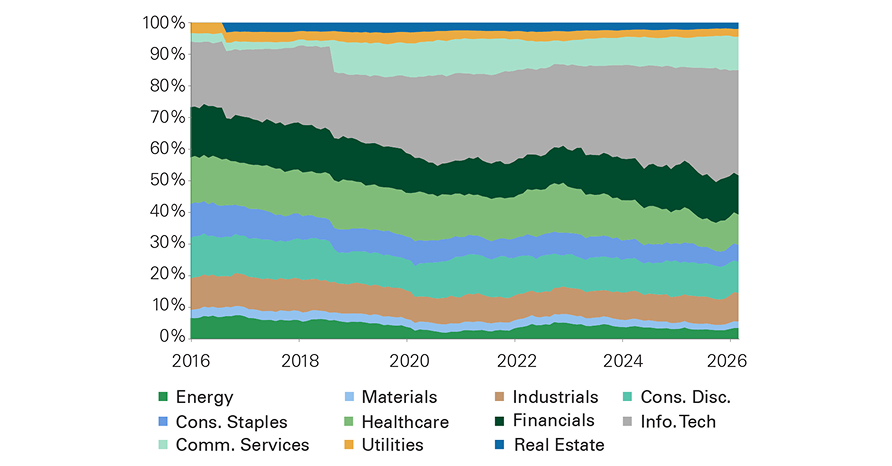

One reason this matters for markets is that, historically, labor-based services have been difficult to scale into trillion-dollar public companies. Growth tends to be linear with headcount, and margins are constrained by labor intensity. As a result, the largest market-cap winners in the S&P 500 have generally been product-, platform-, or asset-based businesses rather than traditional people-intensive services (Exhibit 6). If AI meaningfully relaxes this labor constraint, it could expand the universe of scalable services businesses and reshape where public market value accrues over the next decade.

Exhibit 6: S&P 500 Sector Weights Over the Past 10 Years

Key takeaway: Public market leadership has historically favored scalable models over labor-intensive services, a constraint AI may begin to relax.

Public market leadership has historically favored scalable models over labor-intensive services, a constraint AI may begin to relax.

Rather than eliminating jobs, a more likely outcome is a world in which work evolves unevenly, rewarding those who adapt quickly. The central policy challenge is therefore managing the transition: investing in education, supporting mobility, preserving competitive markets, and ensuring that productivity gains are broadly shared.

Krugman’s reminder is ultimately about economic resilience. Predictions of mass technological unemployment have surfaced for nearly a century. They have been fueled by understandable fears and vivid storytelling. Yet labor markets have consistently adjusted, sometimes with significant dislocation across industries and workers, but rarely catastrophically at the aggregate level.

Artificial intelligence may prove more powerful than prior waves of automation in certain domains. It may compress cognitive tasks in ways that feel qualitatively different. Importantly, however, progress is unlikely to be uniform. AI already solves graduate-level mathematical problems while struggling with simple puzzles that a child can perform intuitively. Capabilities are advancing unevenly across domains, making the labor impact jagged rather than linear. Even so, the underlying economic logic remains intact: The amount of work in an economy is not fixed. Human wants continue to evolve, and productivity growth expands possibilities rather than simply eliminating roles.

The debate, then, should shift from whether AI will end work to how societies shape the next configuration of work. The greater risk lies less in a vanishing job market and more in complacency around the distributional effects of rapid change. If history is a guide, the future will still require human labor. The question is how effectively we prepare for the form it will take.

*Paul Krugman, “The Economics of Technological Change: What History and Models Can (and Can’t) Tell Us About AI,” March 1, 2026.

The proliferation of artificial intelligence has coincided with recent elevated market volatility and uncertainty combined with a broader shift in market structure. Retail investor participation remains elevated, and social media’s growing influence can amplify market moves, even when fundamentals remain sound. One notable area affected by these dynamics is the software sector, which experienced its largest non-recessionary drawdown in more than 30 years, driven in part by AI-related disruption fears. Bessemer portfolios trimmed software exposure throughout 2025 but have used the recent pullback to add to companies with compressed valuations, deeply embedded platforms, and strong fundamentals.

Our largest overweight within the software sector relative to the benchmark is Microsoft, which serves roughly 450 million commercial users of Microsoft 365. At the same time, Microsoft Azure and other cloud services revenue grew 39% last quarter, driven by strong demand across workloads and customer segments. We believe Microsoft’s deeply embedded enterprise software base, paired with rising demand for its AI offerings, leaves it well positioned to benefit despite recent underperformance.

Similarly, the rise of AI is increasing the importance of cybersecurity. We recently added to CrowdStrike given that it is one of the largest cybersecurity providers, and we believe the company is well equipped to adapt to the increasingly complex landscape of cyberattacks.

While we are closely monitoring the risk of headline-driven market volatility, we are also using this shifting market backdrop to find opportunities amid the noise.

Extreme narratives about AI persist because they are emotionally satisfying, strategically useful, and economically incentivized. But they obscure a more important truth: AI is best understood as an extension of existing human systems, not a force that operates outside of them.

Its trajectory will be shaped by choices around governance, competition, capital allocation, labor adaptation, and institutional design. Rather than unfolding all at once, change is more likely to emerge through a series of incremental adjustments — some visible, others less so — across industries and over time.

The real question is not whether AI leads to utopia or dystopia, but how effectively societies manage the transition.

We thank Andrea Tulcin and Joseph Clay for their contributions.

Past performance is no guarantee of future results. This material is provided for your general information. It does not take into account the particular investment objectives, financial situations, or needs of individual clients. This material has been prepared based on information that Bessemer Trust believes to be reliable, but Bessemer makes no representation or warranty with respect to the accuracy or completeness of such information. This presentation does not include a complete description of any portfolio mentioned herein and is not an offer to sell any securities. Investors should carefully consider the investment objectives, risks, charges, and expenses of each fund or portfolio before investing. Views expressed herein are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included herein to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indexes in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index. Alternative investments, including private equity, real assets, and hedge funds, are not suitable for all clients and are available only to qualified investors.