The Expanding Buyer Landscape for Family Business Sales

- Family business owners today have access to a broader range of buyers and transaction structures than ever before, expanding the options available for liquidity, succession, and growth.

- Family offices, independent sponsors, and specialized private equity firms represent a growing share of the buyer landscape, and each offers distinct approaches to partnership, governance, control, and value creation.

- Bessemer helps business owners evaluate and execute liquidity alternatives and align transition decisions with their broader wealth planning and legacy goals.

For many family business owners, deciding whether and how to transition ownership is one of the most consequential decisions they will face. Beyond the financial considerations, these decisions often involve questions of family legacy, control, governance, employee continuity, and the future direction of the business.

Historically, owners seeking liquidity or a transition of ownership generally considered a relatively limited set of alternatives, most commonly a sale to a strategic acquirer or a traditional private equity firm. Today, however, the landscape has evolved. A broader range of buyers and investment structures has emerged, creating greater flexibility for owners pursuing liquidity, succession, growth capital, or long-term strategic partnerships.

This article examines the qualities that make family-owned businesses attractive acquisition targets, reviews the traditional liquidity framework, and explores the expanding range of alternatives available today.

Enduring Strength of Family-Owned Businesses

Family businesses are often attractive acquisition targets because they possess qualities that can be difficult to replicate and contribute to their durability and long-term value:

- Long-term orientation and sound financial management: Family businesses are typically well established in their core markets, with strong profitability and a conservative approach to financial leverage. Profits are often reinvested into the core business and key strategic initiatives before being allocated to shareholder distributions. This disciplined approach supports financial strength and long-term competitive positioning.

- Competitive advantage built on long-standing relationships: Deep relationships with customers and suppliers, developed over decades through consistent ownership and decision-making, create a durable competitive advantage. Counterparties often trust family businesses to operate with a long-term perspective and strong values, fostering lasting partnerships and creating barriers to entry.

- Family legacy as a strategic asset: Many family businesses benefit from a reputation for excellence in operations, quality, and service. Because these areas reflect the family’s legacy and values, owners tend to place particular emphasis on maintaining high operating standards. This is frequently supported by experienced employees with deep expertise who often spend their careers with the business.

When family businesses reach an inflection point and want to explore exit, liquidity, and transition strategies, it is important to know the full range of available alternatives. Family business owners should not underestimate how attractive these characteristics are to potential buyers and partners.

Historical Liquidity Alternatives for Family Businesses

Historically, family business owners seeking liquidity or an ownership transition generally pursued one of two paths: a sale to a strategic buyer or a traditional private equity firm.

Strategic buyer: A strategic buyer is a company in the same or a related industry seeking to acquire and integrate the business into its existing operations.

Strategic buyers are typically positioned to pay an attractive price to achieve synergies, scale, and growth. Often these transactions are for the acquisition of full control in the business and require cultural integration and potentially the loss of a legacy brand.

Traditional private equity: A traditional private equity firm is a financially oriented buyer that acquires businesses for a defined period, typically five to seven years, to create value and generate investment returns.

Private equity firms typically seek control positions and focus on increasing earnings through revenue growth, operational improvements, and add-on acquisitions. They often use the acquired business as a platform for industry consolidation and generally restructure governance while partnering with management through rollover equity and incentive participation. These transactions can work well for owners seeking upfront liquidity while preserving the opportunity for additional upside upon a future sale. However, they also introduce the use of significant leverage and often place less emphasis on preserving legacy and culture.

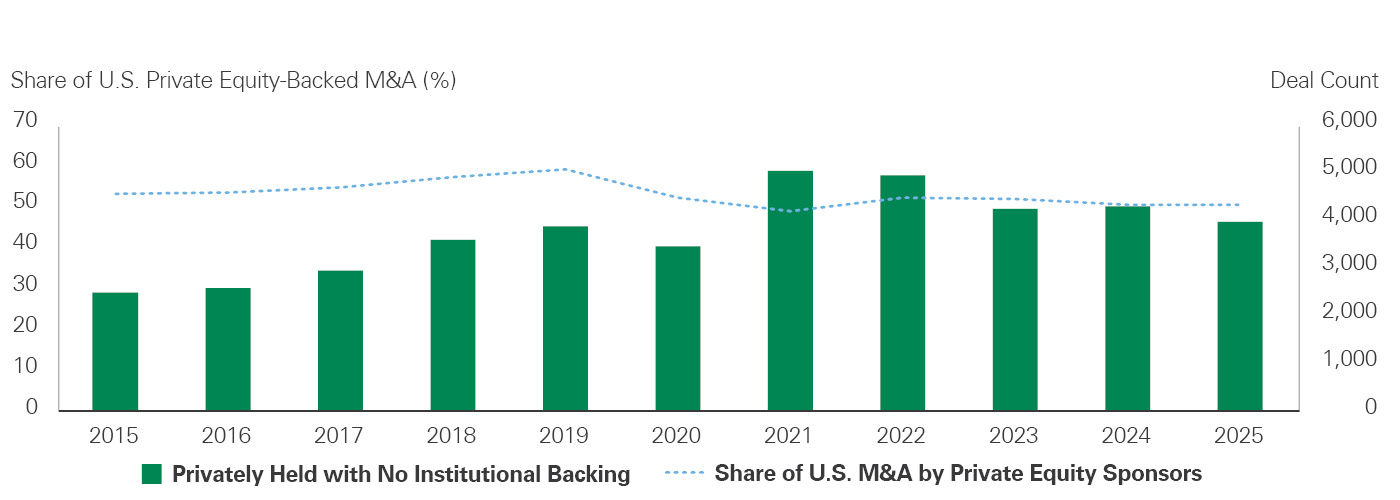

Market Context: An Active Environment for Private Business Transactions

An active U.S. M&A environment provides important context for family business owners considering liquidity, succession, or strategic partnership opportunities. While public attention often focuses on large headline-making transactions, much of U.S. M&A activity continues to involve privately held companies, including businesses with limited or no prior institutional ownership.

The chart below uses privately held companies with no institutional backing as a proxy for family- and founder-owned businesses. It shows that these companies continue to represent a meaningful source of U.S. transaction activity, while private equity sponsors remain active participants in the market. For business owners, this activity underscores the importance of understanding the range of potential buyers, structures, and partnership models available today.

U.S. M&A Activity Involving Privately Held Companies with No Institutional Backing (2015–2025)

Expansion of Buyer Landscape for Family Businesses

While strategic buyers and traditional private equity firms remain the most prominent acquirers, newer buyers such as family offices, independent sponsors, and alignment-focused private equity firms are increasingly interested in strategic partnership. Each offers a distinct combination of liquidity, control, governance, and partnership characteristics, giving business owners greater flexibility in pursuing liquidity events that align with their family and business goals.

Family offices: Many wealthy families and individuals have established their own family offices to manage their wealth. Increasingly, many family offices are investing directly in operating businesses as a way to diversify beyond public markets and institutional funds.

Family office capital is often attractive to business owners due to its patient, long-term approach and emphasis on preserving company culture and legacy. Many family offices can also act as a strategic partner to advise the business owner on key business decisions. Additionally, family offices often have flexibility to invest in a variety of ways, including both common and more structured equity. While family offices tend to prefer lower leverage profiles than private equity firms, their more conservative approach can translate to less aggressive valuations and pricing of transactions. They also typically have leaner deal teams that do not move as quickly through transaction and diligence processes.

Another attractive feature of some family offices is their flexibility to make minority investments rather than requiring full control. For family business owners not yet ready to sell the business outright, minority investments can provide growth capital, a shareholder liquidity opportunity, and a strategic partner while preserving control. The tradeoff is that minority investments may involve valuation discounts and added governance complexity.

Independent sponsors: An independent sponsor is an individual or small team that sources, acquires, and manages a business using outside investors’ capital rather than a precommitted fund.

The key considerations for owners are that these transactions are typically entrepreneur-led and feature a high level of collaboration between the business owner and the sponsor. They can work well when an owner is seeking a gradual transition or when succession is unclear. Bringing in the expertise from the sponsor can often alleviate succession planning concerns. A potential drawback is the broad spectrum of quality and often a more limited track record. Some sponsors are highly experienced investors and operators, while others are less proven. Because capital is typically raised on a deal-by-deal basis, sellers should carefully assess certainty of close, investor support, and the sponsor’s ability to execute through the full transaction process. In recent years, the independent sponsor market has matured, with more capital available and a growing number of institutionally trained sponsors choosing this model despite having the ability to raise committed capital. For many sponsors, however, it represents a deliberate step in building a track record and investor base before launching a committed fund.

Case Study: The Independent Sponsor Model

A family-owned, regionally focused equipment rental business with a long operating history began evaluating succession following a generational transition. The company had built a strong regional position supported by durable customer relationships, a well-established asset base, and a reputation for reliable service.

An independent sponsor identified the opportunity based on deep familiarity with the sector, having followed the company and industry for nearly a decade. After departing a blue-chip private equity firm, this represented the sponsor’s first transaction in a sector it knew well. While the sponsor may pursue raising committed capital over time, it was able to compete effectively with traditional private equity firms and ultimately win the opportunity.

The transaction was structured to provide liquidity while preserving continuity and was tailored around bespoke tax and estate planning objectives across a range of family stakeholders. Backed by a small group of aligned investors, including Bessemer, the sponsor is working closely with management on a focused growth and operational plan, highlighting the growing appeal of the independent sponsor model for select business owners.

Modern private equity: Private equity continues to evolve as competition for high-quality businesses increases and traditional return drivers, including leverage and multiple expansion, become less reliable on their own. A newer group of specialized firms has emerged with greater industry expertise, a stronger operational focus, and an increased emphasis on aligning interests, often with longer hold periods and more flexible partnership structures.

These firms can provide liquidity while allowing owners to retain an equity stake and participate in future value creation. Their specialized expertise and focused operating models may help businesses accelerate growth and profitability while preserving continuity in leadership and culture.

A key consideration for owners is that modern private equity firms can help take the company to the next level. This allows an owner to achieve significant liquidity at the time of sale while retaining an equity stake that can participate in future value appreciation through a subsequent exit. Given these firms’ narrower industry focus and value-creation playbooks, they can help family businesses achieve growth while partnering with management rather than replacing it. This approach can help preserve the family business legacy by keeping the business owners and key employees aligned with the investment team. This strategy involves additional risk due to the use of leverage and the potential for misalignment between the interests of the founding family, management, and the private equity sponsor over time. As with all private equity investments, generating strong financial returns remains the sponsor’s primary objective.

Q&A: The Evolution of Modern Private Equity

In the Q&A that follows, Noah interviews Kyle about the changing private equity landscape, including how firms differentiate themselves today, what matters most in evaluating partnerships, and why specialization and operational expertise have become increasingly important.

Q: How has the sale process changed for high-quality family-owned businesses?

Historically, private equity firms often focused on convincing families that they were strong buyers with capital, experience, and certainty of execution. Today, the standard is higher. Firms must convince multiple stakeholders that they are the right owner for the company’s next chapter. That may include family members across generations, management teams, employees, advisors, and fiduciaries. Buyers need to demonstrate that they understand the business, respect its legacy, and have a strong plan for future growth.

Q: What is a common misconception about selecting a private equity buyer?

A common misconception is that the decision should be based primarily on a firm’s expertise, but owners should not lose sight of the human element. Management teams will work with individuals across the organization, not just the senior partners leading the transaction. Stability and culture also matter, though they can be difficult to evaluate. Challenges will inevitably arise, and owners need confidence in how their partner will respond. These intangibles are difficult to measure but are core to the evaluation of new partnerships.

Q: How has private equity evolved in recent years?

Private equity has become more specialized and intentional. Many firms are focused on developing a clear “right to win” in specific sectors, supported by experience, relationships, and a repeatable value-creation strategy. We see this particularly in regulated industries such as aerospace and defense, where domain expertise and access can create a meaningful competitive advantage. We are also closely tracking the emergence of AI transformation as a core value driver, particularly as the opportunity sets of venture capital and buyout firms increasingly converge.

Q: What does the Bessemer Private Equity team look for when evaluating firms?

We look for firms that can generate outsized returns in a repeatable way, rather than simply benefit from a favorable market cycle. That starts with characteristics such as differentiated sourcing, deep sector expertise, and strong alignment with management teams. It also requires attracting exceptional talent, retaining it, and fostering a culture of continuous improvement.

We are especially drawn to firms that combine discipline with ambition. The best managers are thoughtful about downside risk, but they are also willing to pursue attractive growth opportunities when they have conviction and a clear vision for what a business can become over time.

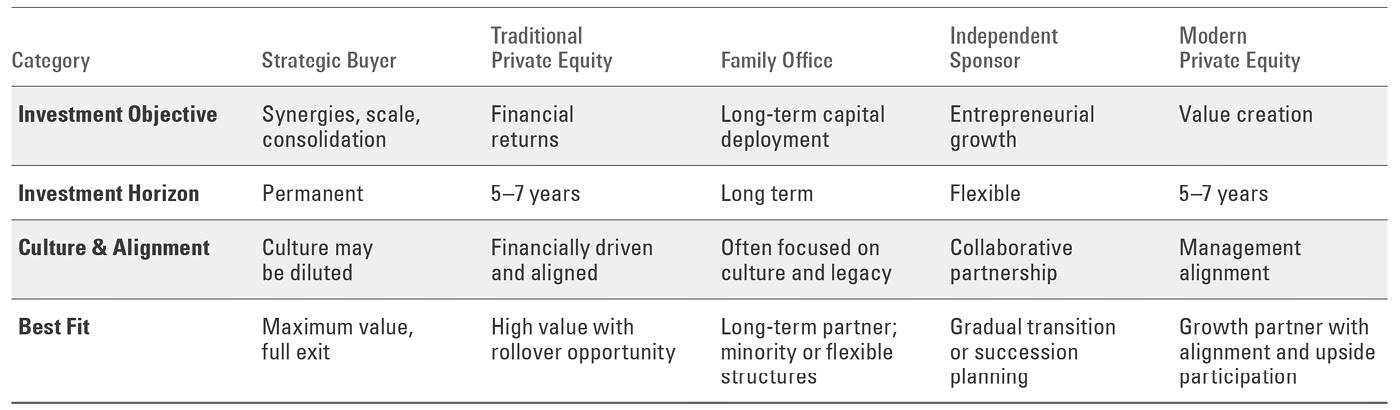

Summary Exhibit

A comparison table titled "Summary Exhibit" evaluates five categories of business acquirers: Strategic Buyer, Traditional Private Equity, Family Office, Independent Sponsor, and Modern Private Equity.

The table compares each buyer type across four criteria:

- Investment Objective

- Strategic Buyer: Synergies, scale, and consolidation.

- Traditional Private Equity: Financial returns.

- Family Office: Long-term capital deployment.

- Independent Sponsor: Entrepreneurial growth.

- Modern Private Equity: Value creation.

- Investment Horizon

- Strategic Buyer: Permanent ownership.

- Traditional Private Equity: 5–7 years.

- Family Office: Long term.

- Independent Sponsor: Flexible.

- Modern Private Equity: 5–7 years.

- Culture & Alignment

- Strategic Buyer: Company culture may be diluted.

- Traditional Private Equity: Financially driven but aligned.

- Family Office: Often focused on preserving culture and legacy.

- Independent Sponsor: Collaborative partnership.

- Modern Private Equity: Strong management alignment.

- Best Fit

- Strategic Buyer: Sellers seeking maximum value through a full exit.

- Traditional Private Equity: High-value transactions with rollover equity opportunities.

- Family Office: Long-term partnerships using minority or flexible investment structures.

- Independent Sponsor: Gradual ownership transition or succession planning.

- Modern Private Equity: Growth partnership with management alignment and shared upside participation.

Overall, the exhibit contrasts how different buyer types vary in objectives, ownership timelines, cultural considerations, and the situations where each is most appropriate.

Conclusion: Takeaways for Family Business Owners

The evolving buyer landscape has expanded the strategic alternatives available to family business owners. In addition to control sales, owners now have access to a broader range of buyers and structures, including minority investments, longer-term partnerships, and more flexible governance arrangements. Each option has distinct implications for liquidity, control, legacy, and risk. Bessemer’s experts work with clients to evaluate these alternatives within the context of a broader wealth planning strategy, helping families navigate complexity while aligning business and long-term family objectives.

Past performance is no guarantee of future results. This material is provided for your general information. It does not take into account the particular investment objectives, financial situations, or needs of individual clients. This material has been prepared based on information that Bessemer Trust believes to be reliable, but Bessemer makes no representation or warranty with respect to the accuracy or completeness of such information. This presentation does not include a complete description of any portfolio mentioned herein and is not an offer to sell any securities. Investors should carefully consider the investment objectives, risks, charges, and expenses of each fund or portfolio before investing. Views expressed herein are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included herein to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indexes in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index. Alternative investments, including private equity, real assets, and hedge funds, are not suitable for all clients and are available only to qualified investors.