Tax Reform Revives Qualified Opportunity Funds

- Recent tax law changes significantly reshape the qualified opportunity fund rules beginning in 2027, reviving a planning strategy that had largely lost momentum under the prior law.

- For taxpayers realizing substantial capital gains, the revised rules may provide an opportunity to defer gain recognition, reduce deferred taxable gain, and potentially eliminate tax on future appreciation associated with qualifying long-term investments.

- While the tax benefits can be meaningful, these funds remain complex investment vehicles with strict compliance requirements, long holding periods, and investment risks that should be evaluated alongside broader portfolio, liquidity, and wealth planning considerations.

Taxpayers who realize substantial capital gains — whether through the sale of a business, concentrated stock position, real estate holding, or other appreciated asset — often face a narrow window in which to evaluate planning opportunities before the associated tax liability comes due.

Qualified opportunity funds (QOFs) offer one potential way to defer recognition of eligible gains while pursuing long-term investment opportunities. Created in 2017 under the Tax Cuts and Jobs Act (TCJA), QOFs were designed to encourage long-term investment in economically distressed communities designated as qualified opportunity zones (QOZs).

Although the original QOF rules generated significant interest when introduced in 2018, portions of the tax benefits became less valuable over time due to fixed statutory deadlines embedded in the legislation. The One Big Beautiful Bill Act (OBBBA) substantially revises the framework for investments made after December 31, 2026, restoring and, in some cases, expanding the potential planning benefits associated with these structures.

For taxpayers anticipating future liquidity events or currently evaluating the reinvestment of realized gains, the revised rules may warrant renewed attention.

Understanding the QOF Framework

QOFs are investment vehicles organized as partnerships or corporations for the purpose of investing in qualified opportunity zone property. Opportunity zones are economically distressed communities nominated by states, territories, or the District of Columbia and certified by the U.S. Treasury.

In broad terms, taxpayers may elect to reinvest eligible capital gains into a QOF within 180 days of the triggering sale or transaction. If the applicable requirements are satisfied, the investment may qualify for favorable tax treatment.

While the framework is straightforward, the underlying rules are highly technical. QOFs are subject to detailed compliance requirements, including the 90% asset deployment test, substantial improvement standards, and specialized working capital rules. Investors should work closely with experienced legal, tax, and investment advisors before pursuing these structures.

The Three Potential Tax Benefits

Qualified opportunity fund investments may provide three potential tax benefits for eligible investors:

Deferral of existing gain. Eligible capital gains reinvested within the required time period may qualify for temporary deferral of federal income tax.

Reduction of deferred gain. Under certain circumstances, a portion of the deferred gain may ultimately be excluded from taxation.

Potential exclusion of future appreciation. If the investment is held for at least 10 years, appreciation on the qualified opportunity fund investment may generally be excluded from federal income tax upon sale or disposition.

How the Rules Changed

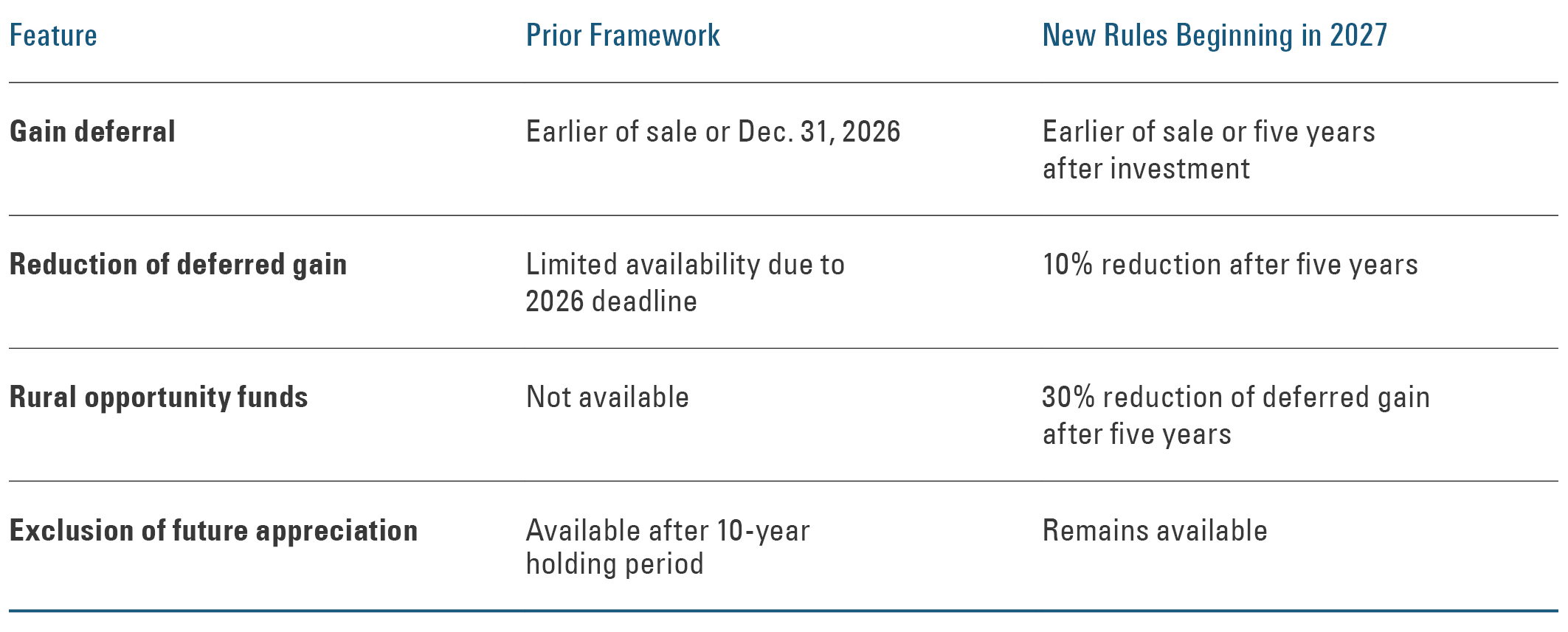

A three-column comparison table contrasts the prior Qualified Opportunity Fund framework with new rules beginning in 2027. The columns are labeled Feature, Prior Framework, and New Rules Beginning in 2027.

The table includes four rows:

- Gain deferral: Previously, gain could be deferred until the earlier of the asset's sale or December 31, 2026. Under the new rules, gain may be deferred until the earlier of the asset's sale or five years after the investment.

- Reduction of deferred gain: Previously, the benefit was limited due to the 2026 deadline. Beginning in 2027, investors receive a 10% reduction of deferred gain after five years.

- Rural opportunity funds: Previously, no special benefit was available. Under the new rules, qualifying rural opportunity funds provide a 30% reduction of deferred gain after five years.

- Exclusion of future appreciation: Under the prior framework, appreciation could be excluded after a 10-year holding period. This benefit remains available under the new rules.

The table uses blue column headings, bold feature labels in the left column, horizontal divider lines between rows, and a blue line along the bottom.

Tax Law Changes Revive the Strategy

OBBBA materially alters the timing and structure of the QOF rules for investments made after December 31, 2026.

Rolling five-year deferral period. Under the original framework, all deferred gains become taxable by December 31, 2026. As that date draws closer, the value of the deferral benefit diminishes for new investors because they have less and less time before the gain must be recognized. After that date, new investors would receive no gain-deferral benefit.

To restore this benefit for future investors, the new law replaces the fixed recognition date with a rolling five-year deferral period for investments made after December 31, 2026. In general, deferred gain becomes taxable upon the earlier of the disposition of the QOF investment or five years after the investment is made.

Return of the basis step-up benefit. Under TCJA, taxpayers holding a QOF investment for at least five years could reduce deferred taxable gain by 10% (and previously by as much as 15% for longer holding periods). Because all deferred gains became taxable by the end of 2026, this benefit effectively disappeared for many later investors.

OBBBA restores the five-year benefit structure for future investments.

For standard QOF investments held at least five years, deferred gain may generally be reduced by 10%.

Enhanced benefits for rural opportunity funds. The OBBBA also introduces a new category of investment vehicle: qualified rural opportunity funds (QROFs). To qualify, a fund generally must invest at least 90% of its assets in rural opportunity zones.

In exchange for directing investment to these communities, taxpayers investing eligible gains into QROFs may receive a substantially enhanced benefit: a 30% reduction in deferred gain after satisfying the applicable holding period requirement.

An Illustrative Example

Assume Liam sells a privately held business in 2027, generating a $50 million capital gain. Within the required 180-day period, he reinvests the full gain into a qualified rural opportunity fund. He holds the investment until 2037 and sells it after it has appreciated by $28 million:

- Under the new rules, recognition of the original $50 million gain is deferred until 2032;

- The deferred taxable gain may be reduced by 30%, resulting in recognition of only $35 million of taxable gain; and

- Since Liam holds the investment for at least 10 years, the $28 million appreciation attributable to the QROF investment itself is excluded from federal income tax upon sale in 2037.

For taxpayers with significant realized gains and long investment horizons, the combined effect of deferral, partial gain reduction, and potential exclusion of future appreciation may be substantial.

Planning Considerations Before Investing

Although the potential tax benefits associated with qualified opportunity funds can be significant, these investments should be evaluated within the context of an investor’s broader financial and wealth planning objectives.

Qualified opportunity funds often involve long holding periods, specialized investment strategies, and complex compliance requirements. As with any investment opportunity, the underlying economics, risk profile, liquidity considerations, and quality of the investment manager remain important factors alongside any potential tax advantages.

Conclusion

OBBBA substantially reshapes the qualified opportunity fund landscape beginning in 2027, restoring several benefits that had effectively expired for many later investors under the original TCJA framework and introducing enhanced incentives for certain rural-focused investments.

For taxpayers anticipating significant capital gains, the revised rules may create meaningful planning opportunities, particularly when paired with a long-term investment horizon and a carefully evaluated underlying strategy.

This material is for your general information. It does not take into account the particular investment objectives, financial situation, or needs of individual clients. This material is based upon information obtained from various sources that Bessemer Trust believes to be reliable, but Bessemer makes no representation or warranty with respect to the accuracy or completeness of such information. The views expressed herein do not constitute legal or tax advice; are current only as of the date indicated; and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. Bessemer Trust or its clients may have investments in the securities discussed herein, and this material does not constitute an investment recommendation by Bessemer Trust or an offering of such securities, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference.