Qualified Small Business Stock After the OBBBA

- Qualified small business stock (QSBS) is a powerful tax planning tool for founders and early investors, in part because it can allow a significant portion of gain on a successful exit to be excluded.

- The latest federal tax law preserves existing QSBS rules for previously issued shares while introducing more flexible provisions for newly issued stock, including shorter holding periods and a higher maximum exclusion amount.

- As a result, QSBS tax benefits have increased and become more accessible, but careful attention to acquisition timing and holding periods is required to achieve optimal outcomes.

Founders and investors have long favored qualified small business stock (QSBS) for its tax benefits, which allow a portion of gains to be excluded on the sale of qualifying shares. The tax savings can be substantial, particularly when eligible stock has appreciated significantly and is sold as part of a successful exit.

The enactment of the One Big Beautiful Bill Act (OBBBA) introduces a layer of complexity. While the legislation preserves the existing QSBS framework for stock acquired before July 5, 2025, it also creates a parallel set of rules for stock acquired on or after that date, expanding certain benefits while introducing additional considerations around timing and holding periods.

As a result, QSBS strategies may now be more flexible, but they also require a more nuanced understanding of how these rules interact. In the sections that follow, we outline the core requirements for QSBS treatment, the updated gain exclusion framework, and key planning considerations under both regimes.

QSBS Requirements

At its core, QSBS refers to stock in certain domestic C corporations that meet the requirements of IRC Section 1202. When these requirements are satisfied, shareholders may be eligible to exclude a portion — or, in some cases, all — of the gain realized on a sale.

To qualify for this treatment, the stock and issuing corporation must meet several key criteria:

- The stock must be originally issued after August 10, 1993.

- The stock must be acquired by a noncorporate taxpayer at original issuance in exchange for money or property other than stock, or as compensation for services provided to the corporation.

- If the stock is acquired before July 5, 2025, the aggregate gross assets of the C corporation at all times prior to and immediately after the issuance (including amounts received in the issuance) must not exceed $50 million. For stock acquired on or after July 5, 2025, the threshold increases to $75 million, indexed for inflation.

- The corporation must use at least 80% of its assets in the active conduct of a qualifying trade or business.

- Certain businesses do not qualify, including the following: service businesses; banking, insurance, and leasing businesses; investment management, accounting, and law firms; farming businesses; minerals, oil, and gas businesses; and hotels and restaurants.

- Certain redemptions of stock by the corporation shortly before or after issuing new shares may disqualify those newly issued shares from QSBS treatment.

- Gifts of stock generally retain QSBS eligibility for the recipient, as do transfers at death and certain transfers from a partnership to a partner.

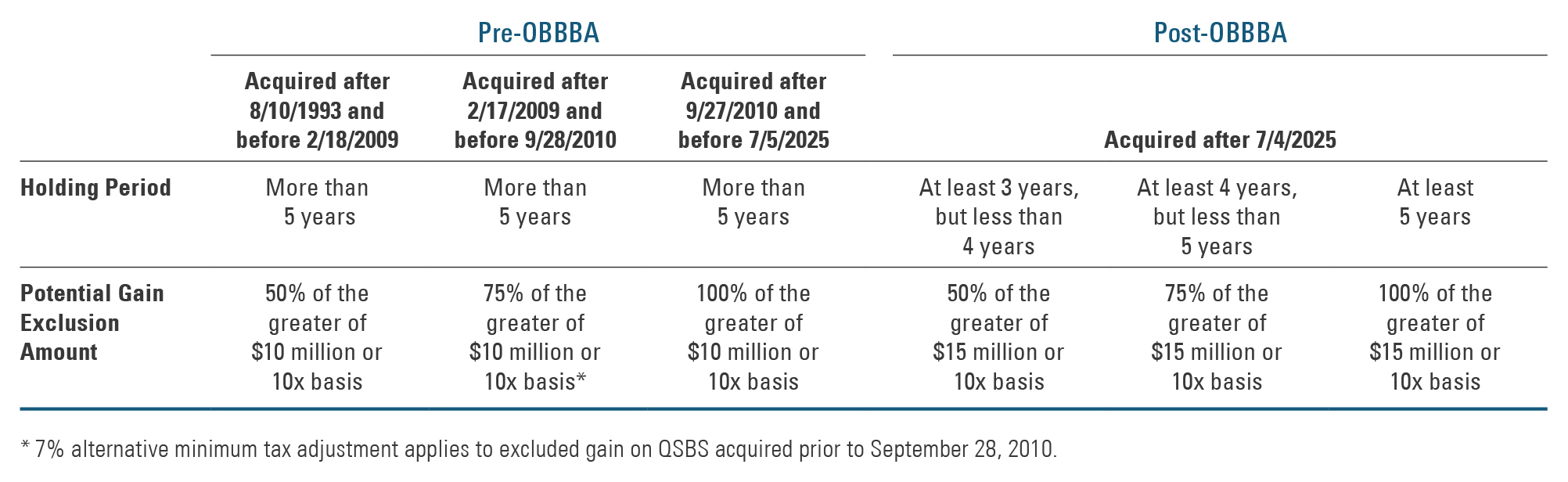

Exhibit 1: Gain-Exclusion Scenarios

A table outlines qualified small business stock (QSBS) tax treatment before and after the OBBBA changes. For stock acquired before July 5, 2025, investors must hold shares for more than five years to qualify for gain exclusions of 50%, 75%, or 100%, depending on acquisition date, with a cap of the greater of $10 million or 10 times basis. For stock acquired after July 4, 2025, tiered holding periods apply: 3–4 years qualifies for 50% exclusion, 4–5 years for 75%, and 5+ years for 100%, with an increased cap of the greater of $15 million or 10 times basis. A footnote notes a 7% alternative minimum tax adjustment for certain earlier acquisitions.

Holding Period and Excludible Gain

The tax benefit associated with QSBS depends largely on two factors: when the stock was acquired and how long it has been held.

Prior to the OBBBA, a minimum holding period of more than five years was required, and the excludible gain increased over time.

The OBBBA introduced a tiered structure for excludible gain based on holding period and increased the maximum exclusion to the greater of $15 million (indexed for inflation) or 10 times basis. Under this framework, the exclusion is determined as follows:

- 50% for stock held at least three years

- 75% for stock held at least four years

- 100% for stock held at least five years (unchanged)

Exhibit 1 illustrates the six gain-exclusion scenarios for QSBS. The date of acquisition and holding period will determine which gain exclusion scenario applies.

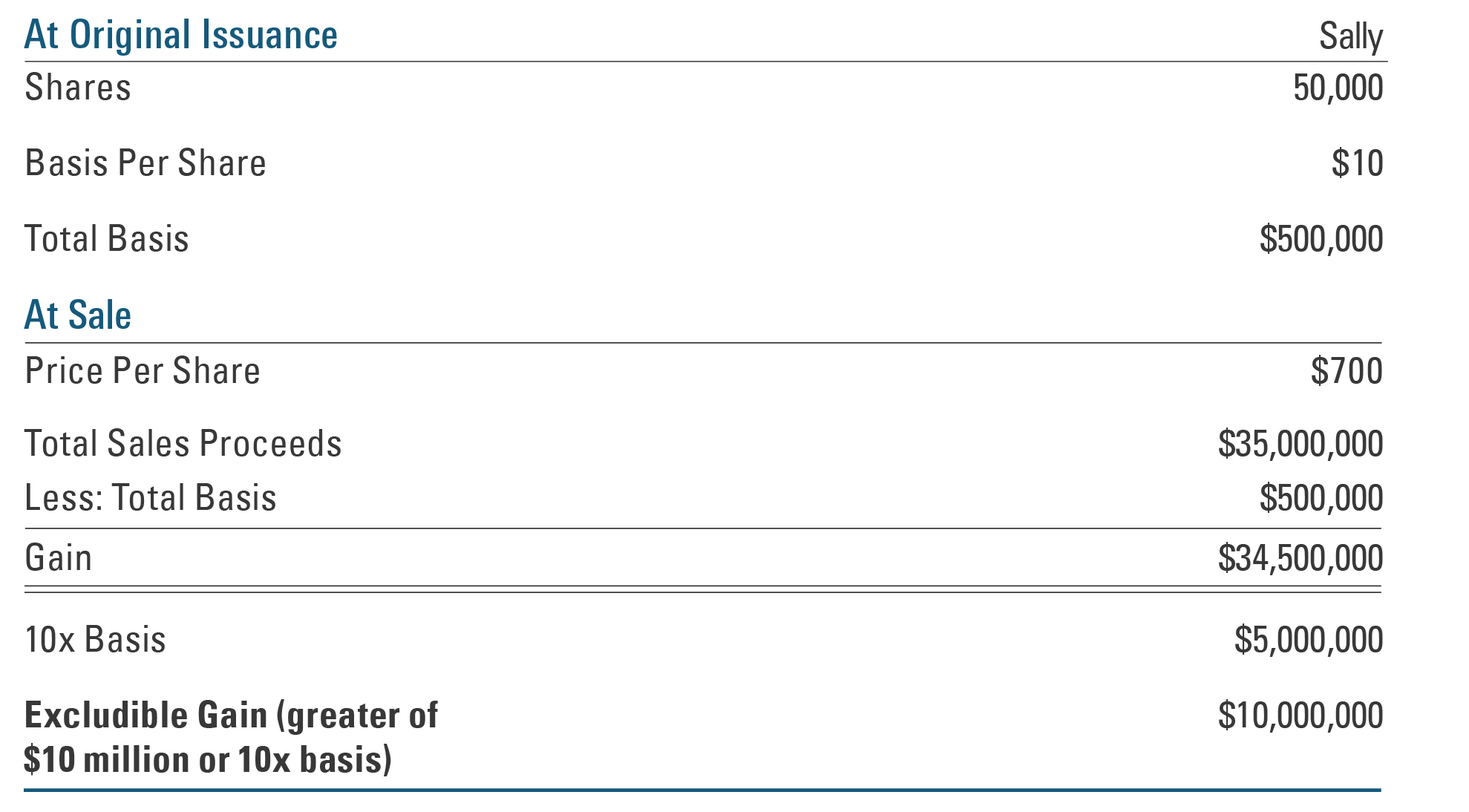

Example 1: Founder Sale — Pre-OBBBA Stock Acquisition

Sally is one of the founders of Acme, a domestic C corporation that produces medical devices. Assume the following:

- Sally acquired 50,000 shares at original issuance in 2019

- Her basis is $10 per share ($500,000 total)

- Acme satisfies the active business requirement

- Aggregate gross assets did not exceed $50 million at issuance

- No disqualifying redemptions have occurred

Acme is sold in 2026 for $700 per share. Sally’s proceeds are $35 million, resulting in a gain of $34.5 million.

Since Acme stock qualifies as QSBS and Sally has held the shares for more than five years, she can exclude 100% of the greater of $10 million or 10 times basis. As a result, she will exclude $10 million in gains.

Example 2: Founder Sale — Post-OBBBA Stock Acquisition (3- to 4-Year Holding Period)

Assume the same facts as above, except:

- Sally acquired her shares on August 1, 2025

- The sale occurs on September 15, 2028

Sally therefore holds the shares for more than three years but fewer than four years. Because the stock was acquired after July 4, 2025, the OBBBA rules apply.

As a result, she may exclude 50% of the greater of $15 million or 10 times basis. She may exclude $7.5 million of gain.

Section 1045 Rollover

When QSBS is sold before the required holding period is met, IRC Section 1045 allows the proceeds to be rolled over into new QSBS. The original stock must have been held for at least six months, and the proceeds must be reinvested in new QSBS within 60 days. The holding period for the replacement QSBS includes the holding period of the original shares, effectively combining the two periods for purposes of meeting the QSBS holding requirement.

Significant advance planning may be required to identify and complete a qualifying reinvestment within the required timeframe.

Planning for Multiple QSBS Exclusions

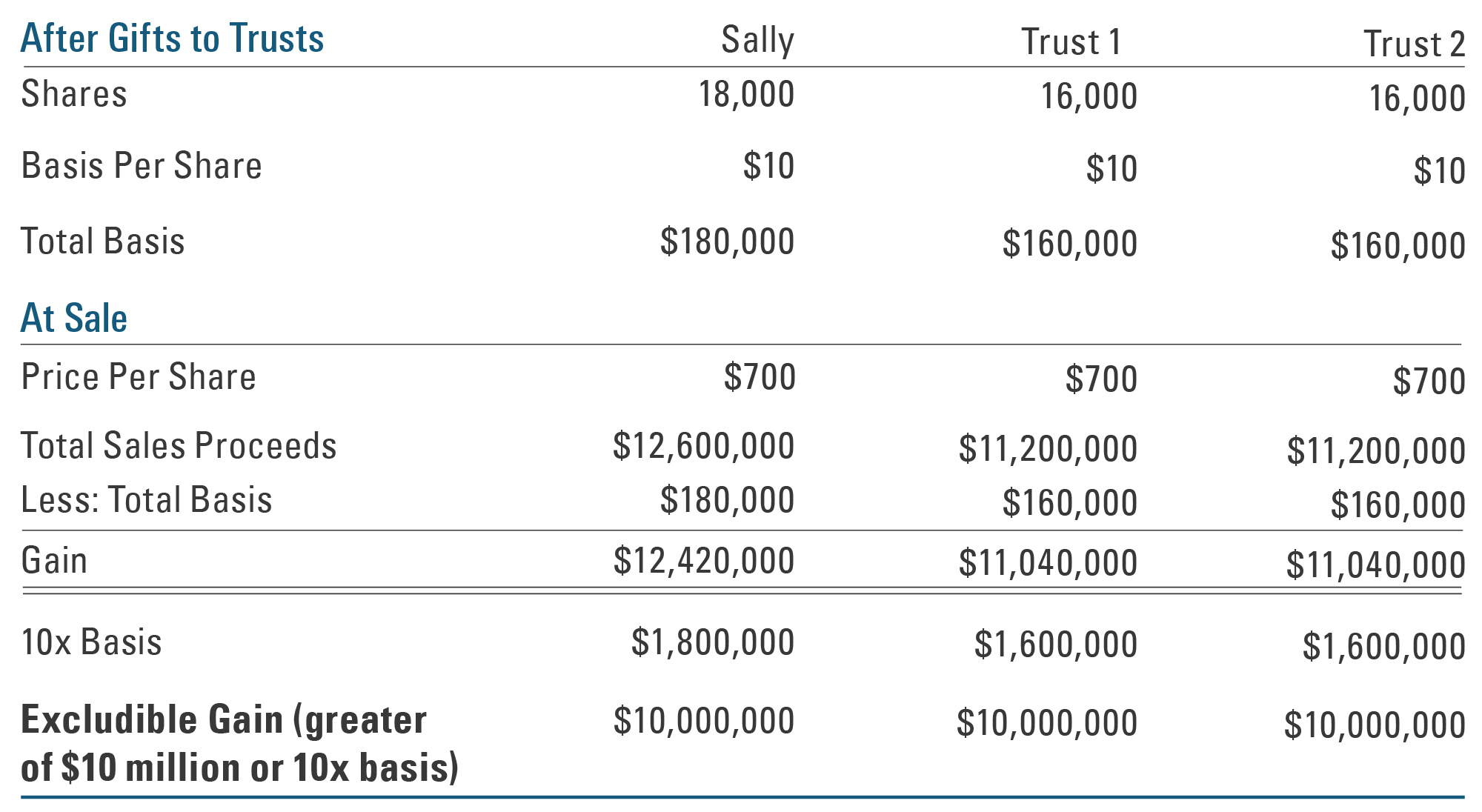

Stock that is gifted retains QSBS eligibility. This may present an opportunity for shareholders to multiply, or “stack,” QSBS exclusions.

A common strategy is to transfer shares to one or more non-grantor trusts. These trusts are treated as separate taxpayers for income tax purposes, allowing each to claim its own QSBS exclusion. By contrast, a similar strategy using a grantor trust would not be effective, as the grantor is treated as the owner for income tax purposes and is limited to a single exclusion.

When implemented thoughtfully, a stacking strategy can significantly increase the total amount of tax-exempt gain on a future sale, particularly in cases of substantial appreciation. It is often advantageous to make these non-grantor trust transfers well in advance of a potential liquidity event, when share values may be lower for gift tax purposes.

Example 3: Gifting Strategy — Multiplying QSBS Exclusions

Assume the same facts as in Example 1, except that in 2021, Sally gifted 16,000 shares to each of two non-grantor trusts established for her children.

At sale, each trust can claim a $10 million QSBS exclusion, allowing Sally to triple the total exclusion available by making gifts of shares to non-grantor trusts.

Advanced Planning — Basis Loading or Packing

Since the QSBS exclusion is calculated as the greater of a specified dollar amount or 10 times basis, strategies that increase basis — and therefore the amount of gain eligible for exclusion — may be considered.

These strategies, often referred to as basis loading or packing, may involve converting an LLC or other entity into a C corporation and/or increasing basis through additional capital contributions and share issuances.

Another approach involves selling both high-basis and low-basis stock within the same year. In certain situations, coordinating these sales may help maximize the total exclusion available, particularly when the 10-times-basis limitation is relevant.

Given the technical nature of these strategies, long-term planning and coordination with experienced legal counsel and tax advisors is essential.

Nonconforming States

Finally, while the federal tax benefits of QSBS can be substantial, state tax treatment should also be considered. Several states do not conform to the federal rules and therefore do not allow the same exclusions. California is a notable nonconforming state.

Putting QSBS Planning into Practice

Effective QSBS planning begins with understanding how the rules apply to a particular situation. QSBS can offer meaningful tax advantages for founders and early investors, particularly when appreciation is significant. At the same time, the changes introduced by the OBBBA add complexity, broadening the range of possible tax outcomes depending on when stock is acquired and how long it is held.

The next step is confirming QSBS eligibility and understanding key attributes, such as acquisition date, basis, and holding period. From there, thoughtful structuring and advance planning may help preserve eligibility and enhance the potential benefit of the exclusion.

As with many tax-driven strategies, the appropriate approach will depend on specific circumstances. Careful modeling of potential outcomes and coordination with experienced tax and legal advisors remain essential to realizing the full benefits of QSBS planning.

This material is for your general information. It does not take into account the particular investment objectives, financial situation, or needs of individual clients. This material is based upon information obtained from various sources that Bessemer Trust believes to be reliable, but Bessemer makes no representation or warranty with respect to the accuracy or completeness of such information. The views expressed herein do not constitute legal or tax advice; are current only as of the date indicated; and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. Bessemer Trust or its clients may have investments in the securities discussed herein, and this material does not constitute an investment recommendation by Bessemer Trust or an offering of such securities, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference.