Planning to Change Your State Residency? An Integrated Tax-Planning Perspective

- State tax residency isn’t determined solely by where you live; it depends on how your actions align with your stated intentions. Two separate standards, domicile and statutory residency, can independently trigger full-year resident taxation.

- Your residency status can also influence how your trusts are taxed, depending on whether you’re a grantor, beneficiary, or trustee. Different rules apply, and a change in personal residence may not eliminate trust-level exposure. Domicile will also affect whether your estate is subject to a state-level estate tax.

- We discuss how coordinated income, estate, and trust planning can help mitigate the risk of being taxed in more than one state and ensure your choices support your long-term goals.

Changing where you live is often a deeply personal decision, shaped by family priorities, financial or business considerations, and lifestyle goals. But it’s also a legal decision with tax implications that can persist long after the boxes are unpacked. As more individuals relocate from high-tax states or divide their time between homes in more than one state, understanding how residency is defined — and taxed — has become essential to thoughtful planning.

While taxpayers often focus on the steps required to establish residency in a new state, far less attention is paid to a critical distinction at the center of state tax law: domicile versus statutory residency.

And the implications don’t stop at the individual level. Residency status can also affect the state tax treatment of trusts, depending on whether you’re a grantor, beneficiary, or trustee. Because the rules vary widely by state and operate independently across states, a change in residence can lead to unintended exposure if not carefully coordinated, including the possibility of double taxation.

In the sections that follow, we explore how to avoid costly surprises by understanding how domicile and statutory residency are defined, how states apply each test, and why focusing on one without the other can expose individuals to full-year taxation in more than one state. We also examine how personal residency decisions intersect with trust taxation and outline strategies to align the two.

Changing your address does not automatically change your state tax exposure.

Domicile vs. Statutory Residency: Two Independent Tests

When it comes to state income tax, it’s important to understand the difference between domicile and statutory residency. Although these terms are often used interchangeably, they are distinct legal concepts, each capable of subjecting an individual to full-year resident taxation.

Domicile and Statutory Residency: Decisions With Broad Tax Consequences

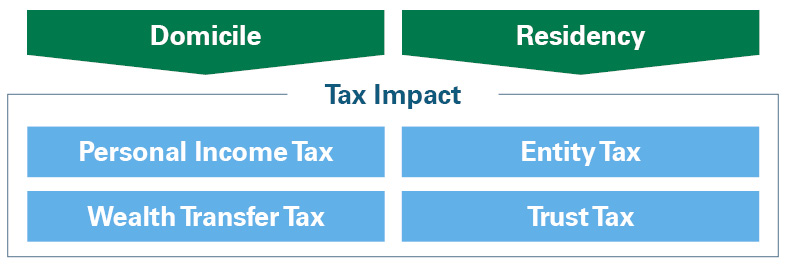

Graphic illustrating the relationship between domicile and residency and their tax impact. At the top are two green banner shapes labeled “Domicile” and “Residency.” Below, a section titled “Tax Impact” connects to four blue boxes arranged in two columns. Under Domicile are “Personal Income Tax” and “Wealth Transfer Tax.” Under Residency are “Entity Tax” and “Trust Tax.” The layout visually shows how domicile and residency influence different categories of taxation.

Domicile: Intent Reflected Through Lifestyle

Your domicile refers to your true, fixed, and permanent home. It’s the place you intend to return to whenever you’re away. You can own multiple residences, but you can only have one domicile at a time.

To change your domicile, you must:

- Physically move to a new location and

- Intend to make it your permanent home, abandoning the former domicile.

Because intent is subjective, states rely on lifestyle evidence to assess it. In practice, this means examining your overall pattern of life, including where you spend your time, which residence you treat as primary, where your social and family life is centered, and where you maintain professional, medical, and financial relationships.

High-tax states place particular emphasis on substance over form. Continuing to maintain a home or meaningful ties in your former state can make it difficult to break residency for tax purposes. Administrative steps (see checklist below), such as obtaining a new driver’s license, registering to vote, or updating estate planning documents, are relevant, but they are persuasive only when supported by consistent lifestyle changes.

A recent court decision by the New York Tax Appeals Tribunal underscores this point.* The taxpayers undertook numerous formal steps to establish Florida residency: acquiring property in Florida, taking steps to sever certain ties with New York, and carefully limiting the amount of time they spent in New York during the relevant tax years. Nevertheless, the tribunal concluded that these actions were insufficient to effect a change in domicile. After closely examining the totality of the circumstances, the tribunal found that the taxpayers’ “general habit of life” continued to point to New York as the true center of their personal, social, and economic affairs and concluded that their intent to abandon New York domicile was not supported by their overall lifestyle. As a result, despite their deliberate planning and compliance with technical requirements, the taxpayers were deemed to remain domiciled in New York for tax purposes.

Domicile also determines whether your estate will be subject to a state-level estate or inheritance tax. While the trend has been for states to eliminate their estate tax, about a dozen states still impose an estate tax with marginal rates up to 20% (although there is a federal deduction for state estate taxes paid).

Statutory Residency: A Mechanical Day-Count Test

Statutory residency is fundamentally different than domicile. It does not consider intent. Instead, it is based on objective statutory thresholds.

In New York, for example, you are considered a statutory resident if you:

- Maintain a permanent place of abode in New York and

- Spend more than 183 days in the state during the tax year.

If you meet both of these conditions, New York may tax you as a full-year resident even if you’re clearly domiciled elsewhere. Other states, including Connecticut and Massachusetts, have similar rules, though the details vary by state.

As a result, you could successfully change your domicile and still be taxed by your former state under statutory residency rules simply because you spent too much time there or retained access to a home.

Why These Distinctions Matter

States apply domicile and statutory residency as separate and independent tests, and either one can trigger full-year resident taxation.

This creates two distinct risks:

- Domicile risk, driven by lifestyle continuity and failure to demonstrate true abandonment of the former home and

- Statutory residency risk, driven by day counts and the continued availability of a residence.

Both standards must be satisfied to avoid exposure to unexpected tax liabilities, including the possibility of double taxation.

Nongrantor Trust Taxation: Residency Beyond the Individual

Residency planning becomes more complex when trusts are involved. State rules governing trust income taxation do not always align with individual residency standards, and an individual’s role as grantor, beneficiary, trustee, or special fiduciary (e.g., trust protector, distribution advisor) can independently create state tax exposure for the trust.

Establishing a Change of Domicile: A Practical Checklist

Domicile Change Checklist

When changing your domicile, be prepared to demonstrate that you left your old state and moved to a new state with the intent to remain there permanently. While each state may view what is necessary differently, below is a list of factors that can help you substantiate your intent to change the location of your permanent home.

Establish a pattern that supports the fact that you have moved to a new primary home:

- Cell phone, credit card, travel activity, and other accessible data will support your physical location.

- Acquire a substantial home in the new state; downsize in the old state.

- Establish a move date (not January 1); take pictures and save receipts evidencing it.

- Move your most precious sentimental or monetary personal items and save shipping documentation.

- Move pets and enroll children in school in the new state.

- Change travel patterns — spend significantly more time in the new state and significantly less time in the former state compared to the past.

- Move primary vehicles and register them.

- Move your homestead exemption.

- File a declaration of domicile if available.

- Change your address. All mail should be addressed to your new primary home.

- Submit a permanent change of address request to the U.S. Postal Service.

- Get a new driver’s license and relinquish your old driver’s license.

- Change toll passes and parking permits.

- Update your homeowner’s insurance policy to reflect the new primary residence.

- Execute new wills, powers of attorney, and other estate planning documents in the new state.

- Open an account at a local bank and relocate your safe deposit box.

Unplug from your previous community, and plug into your new community:

- Spend more time where your primary home is located than anywhere else.

- Join clubs and social and religious organizations near your new home, and change status to “non-resident” or resign from old ones.

- Look for board and committee memberships in the new state, and resign from previous local leadership positions.

- Get season tickets, join museums and community groups, and attend local attractions.

- Reduce significantly or do not renew memberships and season tickets in the previous state.

- Find new doctors, dentists, hairstylists, gyms, therapists, etc., near your new home.

- Have medical records forwarded from your former providers.

- Register to vote, and vote in person.

- Make new friends and connect with extended family near your new home.

- Change social media profiles and post evidence of local engagement.

- Host special occasions at your primary home.

Move your business activities or retire/scale back business activities in your former state:

- Even if you don’t travel for business, scale back day-to-day activities and decision making for the business located in your former state.

- Get a job, establish a business, or otherwise work from your new location.

- Move professional licenses, business registrations, and professional affiliations.

- Change online business profiles to reflect your new home state and affiliations.

We recommend creating an audit response file that documents all your steps to establish domicile in the new state and the affirmative actions you have taken to break or reduce ties to the old state. The more organized and well documented your change in domicile is, the smoother and less stressful the audit experience will be. Bessemer can assist with this process.

Settlor’s Residency: Lasting Effects on Trust Taxation

In many states, a trust may be treated as a resident trust based on the settlor’s domicile at the time the trust became irrevocable.

Take New York, for example. An irrevocable trust funded by an individual domiciled in New York is classified as a New York resident trust, even if:

- The settlor later moves to another state and

- The trustees and beneficiaries reside outside New York.

Fortunately, New York provides an exception: A resident trust is exempt from tax if there are no New York trustees, New York property, and New York income sources.

A state’s ability to tax a trust is not unlimited. In many cases, a state may not tax a trust if there is only minimal connection between the trust and the taxing state, sometimes described as “insufficient nexus.” For Bessemer clients, this connection may be established or limited using Bessemer Trust’s multiple trust companies and carefully limiting fiduciary powers that could establish connections to high-tax states. Care must be taken to avoid granting significant powers to other fiduciaries, such as investment or distribution advisors, that could create additional state contacts.

The legal landscape in this area continues to evolve, with several favorable court decisions limiting state taxation of trusts, including McNeil (2013, Pennsylvania), Linn (2013, Illinois), Kaestner (2015, North Carolina), and Fielding (2018, Minnesota).

These rulings underscore the importance of reviewing existing trusts before a domicile change and considering whether restructuring or trustee changes may be appropriate.

When establishing a grantor trust, it’s important to select a trustee whose residency won’t trigger state taxation if grantor status is ever turned off or the settlor dies. For existing trusts, it’s worth reviewing trustee residency before making any change to grantor status.

Trustee Residency and Trust Administration: A Key Nexus Factor

Where a trust is administered and where its trustees reside can be decisive factors in determining a trust’s state tax exposure.

States such as California, Arizona, Oregon, and New Mexico place significant weight on where trustees reside and where fiduciary decisions are made. If you name a trustee who lives and administers the trust in a high-tax state, that state may assert taxing rights over the trust, even if the grantor and beneficiaries reside elsewhere.

By contrast, Florida, which does not impose a state income tax, is often viewed as a favorable jurisdiction for trust administration. But naming a Florida trustee or administering the trust in Florida does not automatically eliminate tax exposure. Other states may still assert residency based on grantor, trustee, or beneficiary connections.

In other words, trustee residency matters, but it’s just one part of a broader picture. Choosing trustees and structuring administration should be done with a full view of how all parties and fiduciary roles interact across state lines.

Coordinating Residency and Trust Planning

Individual residency rules and trust residency rules operate independently. Changing your domicile does not automatically resolve trust-level tax exposure and may, in some cases, introduce new complexity.

If you’re relocating, it’s worth asking:

- Whether any of your existing trusts may remain taxable in your former state.

- How your current domicile may affect future trusts when they become irrevocable.

- Whether trustee composition, trust situs (the trust’s legal location for administration and tax purposes), or governing law should be revisited.

- How beneficiary residency may influence distribution planning.

These questions are especially important if you own multiple homes or have complex family structures or closely held business interests. Addressing domicile, statutory residency, and trust residency in a coordinated manner is essential.

Plan Ahead to Minimize Risk

Ultimately, state residency planning is about creating alignment between your intentions and your behavior, your residency and trust structures, and today’s decisions and your long-term goals.

A thoughtful, well-documented approach, developed in coordination with tax and legal advisors, can mitigate the risk of disputes and unexpected tax bills in an increasingly aggressive state tax environment. Your Bessemer advisor can help you plan ahead to successfully navigate this process.

Matter of John J. Hoff & Kathleen Ocorr-Hoff.

The information and opinions contained in this material were prepared by Bessemer Trust and are for informational purposes only. They do not take into account the particular investment objectives, financial situation, or needs of any individual client. This material is based upon information obtained from various sources that Bessemer Trust believes to be reliable, but Bessemer makes no representation or warranty with respect to the accuracy or completeness of such information. The views expressed herein do not constitute legal or tax advice; are current only as of the date indicated; and are subject to change without notice. Bessemer Trust does not provide legal advice. Please consult with your legal advisor to determine how this information may apply to your own individual situation. Whether any planned tax result is realized by you depends on the specific facts of your own situation at the time your taxes are prepared.