Is a Family Office Right for You?

- As a family’s wealth and responsibilities expand, increased complexity often raises questions about how best to coordinate investments, planning, and operational oversight — and whether a family office may be an appropriate solution.

- Family office structures exist along a spectrum — from models supported primarily by external professionals to those fully staffed in house, with several hybrid approaches in between.

- In this piece, we explore key considerations, assess structural options, and weigh service and cost dynamics in determining the most appropriate approach for you.

For many families of substantial wealth, there comes a time when financial complexity begins to outpace coordination.

You may have sold the family business. Your investment portfolio may now include private equity, real estate, and other illiquid assets, or your philanthropic commitments may be expanding. Your family may have multiple generations requiring planning, education, and governance. With many moving parts, oversight can begin to feel fragmented.

You may find yourself asking whether a family office would be right for you.

How a Family Office Supports Your Wealth

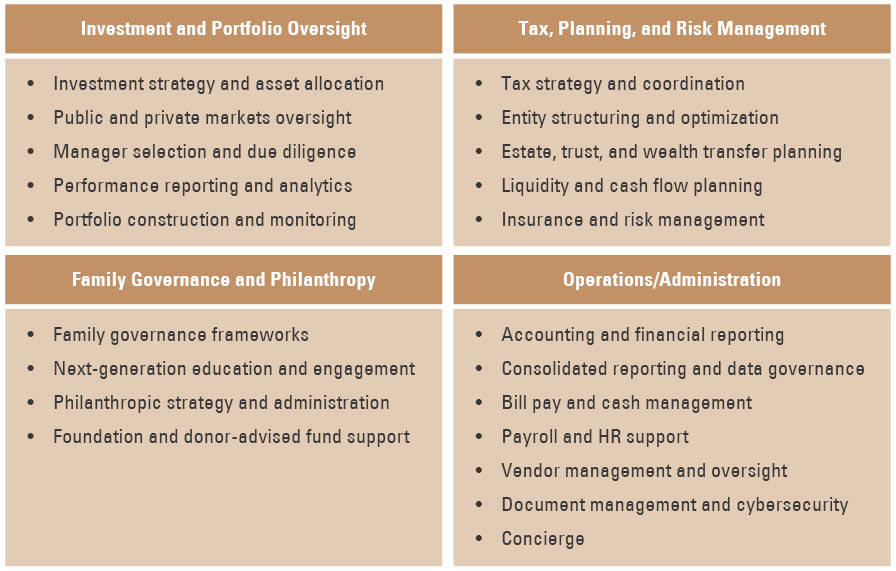

A family office brings structure by centralizing oversight of a family’s financial life and the operational responsibilities that support your household and related entities. These responsibilities typically span several core areas — from investment management and planning to day-to-day administration (Exhibit 1).

Exhibit 1: The Range of Family Office Services

A four-quadrant infographic summarizes the primary functions of a family office. The first section, “Investment and Portfolio Oversight,” includes investment strategy and asset allocation, public and private markets oversight, manager selection and due diligence, performance reporting and analytics, and portfolio construction and monitoring. The second section, “Tax, Planning, and Risk Management,” covers tax strategy and coordination, entity structuring, estate and wealth transfer planning, liquidity and cash flow planning, and insurance and risk management. The third section, “Family Governance and Philanthropy,” highlights governance frameworks, next-generation education and engagement, philanthropic strategy, and donor-advised fund support. The fourth section, “Operations/Administration,” includes accounting, consolidated reporting, bill pay and cash management, payroll and HR support, vendor oversight, document management, cybersecurity, and concierge services.

How these services are delivered — and the structure required to support them — will depend on your family’s specific needs and priorities. When these services are organized around the needs of one family, the structure is often referred to as a single family office (SFO).

Clarifying Your Objectives

Depending on the scope of services provided and the level of oversight a family wishes to retain, an SFO can be organized in different ways. If you’re considering an SFO, an important first step before determining the right approach is clarifying your objectives, as these priorities ultimately shape the office’s design.

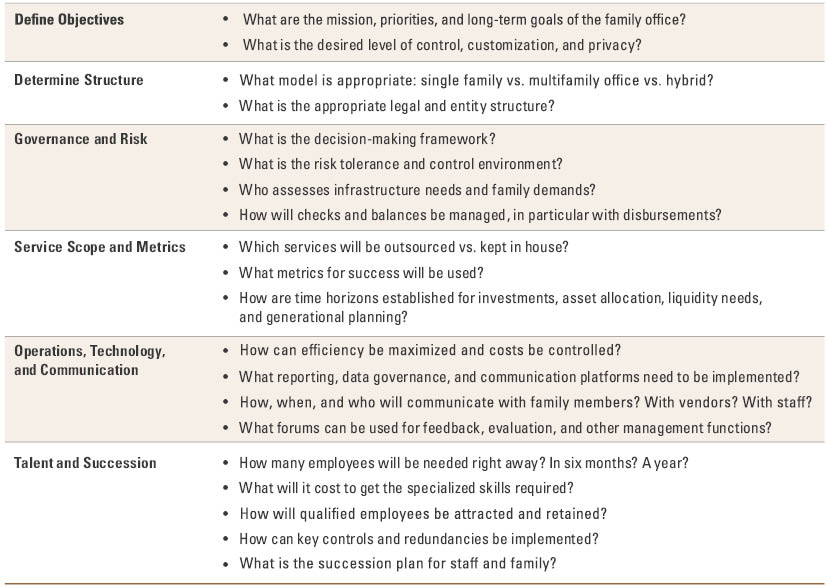

As you translate these objectives into an SFO structure, several key design considerations come into focus (Exhibit 2):

- The size and complexity of your family’s wealth, including the mix of liquid and illiquid assets.

- The scope of services required, including both investment and non-investment needs.

- The desired level of control and governance, including how much oversight is retained in house.

- The role of family members, including their capabilities and level of involvement.

Once you establish clear priorities, you can determine the appropriate structure — or decide whether a family office is right for you at all.

Exhibit 2: Family Office Design Considerations

A structured checklist presents major planning categories for establishing a family office. Sections include defining objectives, determining the appropriate organizational structure, governance and risk oversight, service scope and metrics, operations and communication, and talent and succession planning. Each category contains guiding questions related to mission, privacy, legal structure, decision-making, outsourcing, reporting systems, staffing needs, cost management, and succession planning for both staff and family members.

Family Office Structures: A Spectrum of Approaches

Single family office structures exist along a continuum, reflecting different approaches to staffing, outsourcing, oversight, and operational responsibility (see Exhibit 3). These structures can range from largely outsourced to embedded or hybrid models and fully staffed in-house offices that place more capabilities under the family’s direct control. Families may access external support through integrated multifamily offices (MFOs) or a combination of specialized third-party providers, depending on their needs and desired level of involvement. Multifamily offices, including Bessemer Trust, may support families across this spectrum — serving as the primary provider of family office services for some families while providing targeted services or specialized capabilities for others. Many families begin with targeted support in specific areas and adjust their structure over time, adding internal capabilities, outsourcing specialized functions, or consolidating services as their needs change.

Exhibit 3: Spectrum of Single Family Office Structures

A horizontal spectrum illustrates increasing levels of internal staffing and direct oversight in family office models. On the left, the “Outsourced” model relies heavily on external professionals and integrated multifamily office platforms. The middle “Embedded” model retains selected internal capabilities while outsourcing specialized functions. On the right, the “Fully Staffed” model uses dedicated employees to deliver most services in house. The arrow indicates progression toward greater internal control and operational complexity.

While every arrangement is ultimately customized, the following models provide a useful framework for evaluating these choices:

Outsourced. At one end of the spectrum, families may rely on external professionals to deliver comprehensive family office services. This can be implemented either by coordinating multiple specialized providers or by working with a single integrated firm. In the latter case, services are often delivered through an MFO platform, which provides families with a shared infrastructure while still offering customization to meet their unique needs. This approach provides greater efficiency and access to institutional capabilities with less day-to-day operational oversight required from the family.

Embedded. Moving toward the middle of the spectrum, some families adopt a more flexible model, retaining core capabilities internally while outsourcing select specialized services such as investment management, tax advisory, legal services, or technology support. In many cases, these internal functions may be embedded within a family’s operating business. These structures balance control with access to external expertise and require active coordination across providers to ensure seamless service delivery and accountability.

Fully staffed. At the other end of the spectrum, a family may build and operate a fully staffed office, with services delivered primarily in house by dedicated employees. This model offers a high degree of customization and direct oversight but comes with higher costs as it requires significant resources, infrastructure, and staffing — particularly to recruit and retain the right talent. In practice, fully staffed offices can range in size from a single employee to teams of 50 or more, depending on the scope and complexity of services provided.

These models are not static. As a family’s needs change, it may adjust its structure by adding internal capabilities, outsourcing specialized functions, or consolidating services with fewer, more integrated providers.

Where a family falls along this spectrum depends on its objectives, complexity, desired level of oversight, and tolerance for operational responsibility.

What are the family’s needs, how complex are they, and do they have the scale to warrant a family office?

— Michael Marquez, President, Bessemer Trust

The Wall Street Journal, “What Is a Family Office and How Does It Work?”

In-House or Outsourced Services?

Managing a significant pool of wealth can be time-consuming and complex. For families establishing or evolving a family office structure, a key question is which services are best handled in house and which are better outsourced.

Keeping key functions in house provides direct day-to-day oversight but can increase complexity and cost.

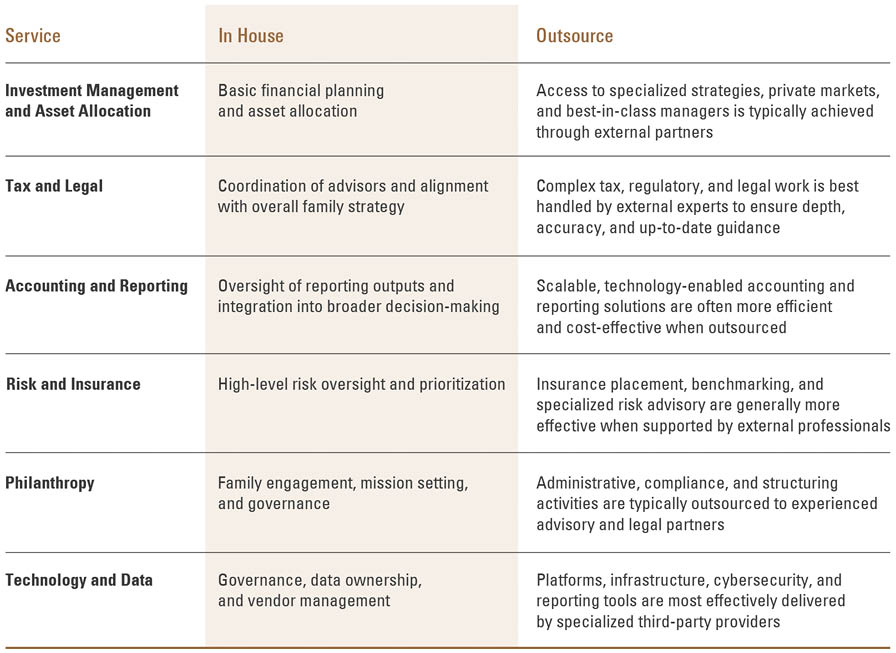

Third-party professionals often bring specialized tools, expertise, robust technology platforms, research capabilities, and infrastructure that enhance value and efficiency, particularly for non-core or highly specialized functions (Exhibit 4).

Exhibit 4: What to Keep In House? What to Outsource?

A comparison table outlines typical responsibilities handled in house versus outsourced across several family office functions. Investment management internally focuses on planning and asset allocation, while specialized strategies and manager access are often outsourced. Tax and legal functions emphasize advisor coordination internally but rely on outside experts for technical compliance work. Accounting oversight may remain internal while scalable reporting systems are outsourced. Risk and insurance oversight is typically strategic internally, with insurance placement and benchmarking managed externally. Philanthropy governance often remains internal, while administrative and compliance support is outsourced. Technology and data governance stay in house, while infrastructure, cybersecurity, and reporting platforms are commonly managed by third-party providers.

Key criteria in deciding which services to retain in house and which to outsource include:

- The depth and breadth of expertise required

- The cost to acquire that expertise

- Technology needs and associated costs

- Administrative complexity and required management time

- The range of non-investment services required

- The required involvement and capabilities of family members

The Cost and Complexity of a Fully Staffed SFO

Among the structures described above, a fully staffed single family office (SFO) is typically the most resource-intensive. For families considering this model, it is important to understand both what is involved in establishing the office and what will be required to operate it over time.

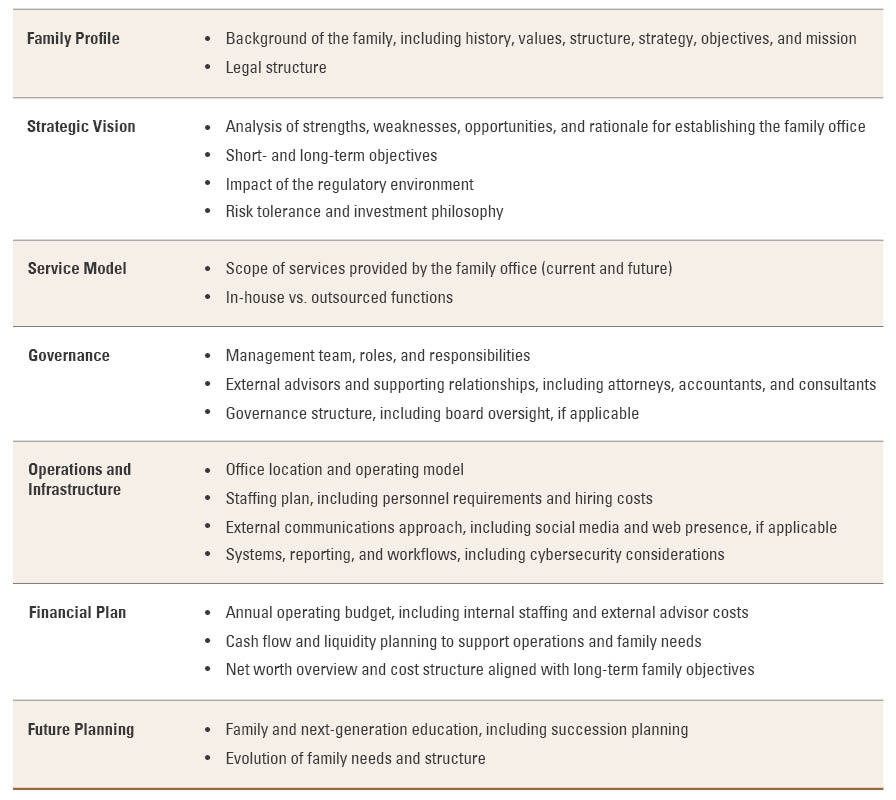

In practice, building a fully staffed office often begins with a comprehensive business plan developed with the support of experienced advisors. This plan should address the organizational, operational, and financial dimensions of the office, including its governance structure, scope of services, staffing needs, technology requirements, office space, reporting capabilities, and risk management framework (Exhibit 5).

Exhibit 5: Components of the Family Office Business Plan

A business planning framework outlines the core components of a family office plan. Categories include family profile, strategic vision, service model, governance, operations and infrastructure, financial plan, and future planning. Topics covered include family history and objectives, legal structure, investment philosophy, in-house versus outsourced services, management roles, staffing requirements, reporting systems, cybersecurity, annual budgets, liquidity planning, succession planning, and next-generation education.

The scope of planning required to establish a fully staffed SFO is closely tied to the resources needed to support it, both at the outset and on an ongoing basis.

For families with $250 million to $750 million in assets, establishing a fully staffed office can involve significant upfront costs related to staff recruitment, relocation, office space, and technology. Families with assets below $250 million often limit services to administration, asset oversight, and risk management.

Maintaining a full-service family office can cost $1 million or more annually, and in some cases significantly more (Exhibit 6). Costs vary widely depending on the scope of services, geographic location, and staffing needs. Many families adopt a more flexible approach, allowing their family office to evolve over time as their needs change.

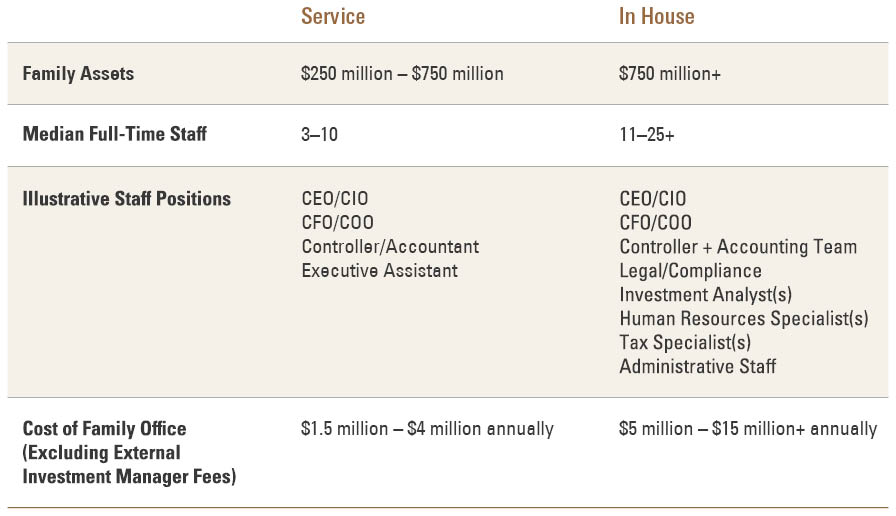

Exhibit 6: What Does It Cost to Run a Full-Service Single Family Office?

A benchmarking table compares two family office operating structures. Service-oriented offices typically support families with $250 million to $750 million in assets, employ three to ten full-time staff, and incur annual operating costs between $1.5 million and $4 million excluding investment manager fees. Fully in-house offices generally support families with more than $750 million in assets, employ eleven to twenty-five or more staff, and incur annual costs ranging from $5 million to more than $15 million. The table also lists illustrative roles such as CEO/CIO, CFO/COO, controllers, accountants, tax specialists, HR personnel, legal/compliance staff, analysts, and administrative support.

How these costs are incurred and allocated can also have important tax implications. For more on how family office structures may affect the tax treatment of expenses, please see “Evolving Structure and Governance for Today’s Family Office.”

Staffing is often the largest ongoing expense. In our experience working with family office clients, compensation and benefits account for more than 60% of total operating costs, consistent with industry norms. Competition for skilled professionals can make recruitment and retention both costly and challenging.

Staffing requirements can also be extensive (Exhibit 7). In addition to personnel, families should budget for infrastructure, including systems to support alternative investments — such as private equity, real estate, oil and gas, and commodities — and portfolio monitoring, reconciliation, and regulatory reporting.

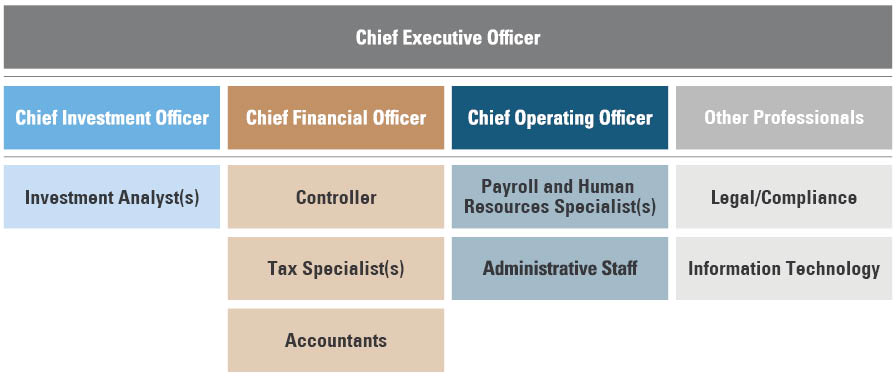

Exhibit 7: Full-Service SFO Staffing Requirements

An organizational chart displays a typical family office hierarchy. At the top is the Chief Executive Officer. Reporting roles include the Chief Investment Officer, Chief Financial Officer, Chief Operating Officer, and other professional functions. Supporting positions include investment analysts under the CIO; controllers, tax specialists, and accountants under the CFO; payroll and HR specialists plus administrative staff under the COO; and legal/compliance and information technology professionals under other professional services. The chart illustrates the division of responsibilities across investment, finance, operations, compliance, and technology functions within a family office structure.

Ongoing information technology (IT) costs, including system upgrades, data backups, and system risk management, particularly cybersecurity, would also need to be factored in. For more on this topic, please read “How to Protect Your Single Family Office From Cybercrime.”

Managing these operating costs — including staffing, administration, and IT — is an ongoing challenge and a key reason many families choose to work with integrated providers. In addition to accessing specialized expertise, families can benefit from economies of scale, as the firm spreads costs over a larger asset base and delivers greater efficiencies than most standalone operations can achieve.

Finding the Right Balance

A well-designed family office should evolve as your family evolves. With thoughtful planning, you can establish an approach that balances flexibility, efficiency, and cost, supporting your goals today and across generations.

No single model fits every family. The appropriate structure depends on your family’s wealth, priorities, and desired level of involvement. Many start with targeted support in specific areas and transition to different family office structures as complexity increases. Others maintain an established family office structure and augment it with external resources. The most effective approach is one that adapts as your family’s needs change.

Founded in 1907 as the Phipps family’s single family office, Bessemer Trust evolved with the family’s needs and opened its doors to nonfamily clients in 1974. Today, as a multifamily office, Bessemer brings generational experience and a long-term perspective to helping families navigate complex circumstances and determine how the pieces fit together. Bessemer supports families across a range of single family office structures — whether they are building and operating a dedicated in-house office, coordinating select internal and external resources, or seeking a fully integrated solution.

Through investment management, wealth planning, and family office services — including portfolio management, fiduciary services, accounting, bill pay, and other day-to-day financial administration — we help families design an approach that fits their needs today and can evolve with them across generations.

To explore whether a family office could make sense for your family — and, if so, what structure may best support your needs — please contact your Bessemer advisor.

This material is for your general information. It does not take into account the particular investment objectives, financial situation, or needs of individual clients. This material is based upon information obtained from various sources that Bessemer Trust believes to be reliable, but Bessemer makes no representation or warranty with respect to the accuracy or completeness of such information. The views expressed herein do not constitute legal or tax advice; are current only as of the date indicated; and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. Bessemer Trust or its clients may have investments in the securities discussed herein, and this material does not constitute an investment recommendation by Bessemer Trust or an offering of such securities, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference.