Blocking and Tackling: Year-End Income Tax Planning in 2022

- The midterm elections are past, and no major tax law changes are likely in the near future.

- Effective year-end tax planning is still possible. In fact, a consistent focus on tax planning fundamentals can bring significant future benefits.

- In this Wealth Planning Insights, we review some fundamental tax planning strategies that have the potential to provide long-term economic value.

Year-end income tax planning moves are often recommended in anticipation of actual or expected changes in the tax law. When higher tax rates are on the horizon or deductions are set to be suspended or eliminated, tax planning moves are generally intuitive and easy to chart out.

However, this is not the situation we presently face. With the midterm elections behind us, we do not expect significant tax law changes in the near future. The next major set of tax law changes are not scheduled until the end of 2025, when the individual tax provisions from the Tax Cuts and Jobs Act (TCJA) will expire (see TCJA Provisions Scheduled to Expire 12/31/2025).

A relatively static tax landscape does not preclude the potential for effective year-end tax planning. In such times, we should focus on the fundamentals — the blocking and tackling of tax planning. Consistently applied, the following planning moves can yield significant future benefits.

Self-Employed Retirement Plans

Many individuals report net self-employment income as part of their yearly tax filing, including the receipt of consulting or directors’ fees, which can be substantial. A frequently overlooked tax planning opportunity is a self-employed retirement plan. Contributions can be made to these plans based on the amount of net self-employment income. Not only are these contributions tax-deductible, providing an immediate tax benefit, but the funds will grow in a tax-deferred account until withdrawn in retirement.

One such plan, the solo 401(k), allows for surprisingly large tax-deductible contributions. Depending on the level of self-employment income, annual contributions in excess of $60,000 may be allowed.

Retirement plan contributions need not be made by the end of 2022. Depending on the type of plan chosen, the funding is generally required by April 15, 2023.

Tax benefits: Current-year tax deduction; multiple years of tax-deferred growth, future Roth conversion opportunity.

TCJA Provisions Scheduled to Expire 12/31/2025

- Reduced individual top tax rate of 37%

- Increased AMT (alternative minimum tax) exemption and phaseout threshold

- Increased standard deduction

- Suspension of Pease provision — income-based reduction in allowable itemized deductions

- $10,000 cap on state and local tax deduction

- Suspension of miscellaneous itemized deductions

- 20% qualified business income deduction

- Suspension of limitation on mortgage and home equity interest

- 60% AGI (adjusted gross income) limitation on cash contributions to public charities

- Increased estate and gift tax lifetime exemption

Tax Loss Harvesting

It is often beneficial to recognize losses within an investment portfolio to offset current-year realized taxable gains. Short-term gains are subject to a combined federal and net investment income tax rate that can be as high as 40.8%, so these may warrant special attention. Losses from cryptocurrency investments can be used to offset other portfolio gains.

Care should be taken when exiting and re-initiating positions in substantially identical securities. The wash sale rule forestalls the recognition of losses where substantially identical securities are purchased 30 days prior to or following the date of sale.

Tax benefit: Reduced current-year tax liability on capital gains.

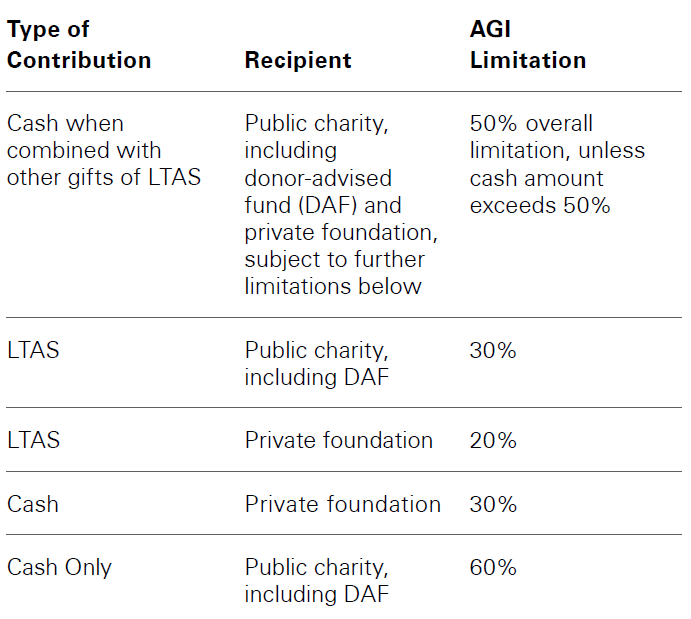

Charitable Gifts of Long-Term Appreciated Securities

We recommend clients use long-term appreciated securities (LTAS) for charitable giving. A tax deduction is allowed for the full fair market value of securities donated to charity without triggering recognition of the embedded taxable gain. To qualify as long term, the holding period must exceed one year.

As compared to cash, the economic value of appreciated securities is actually less than fair market value due to the associated tax burden on the appreciation. Nonetheless, the tax code provides a deduction equal to fair market value.

The amount of deduction allowed in any given year may be limited based on the type of contribution, the charitable recipient, and adjusted gross income (see chart below). Excess amounts may be carried forward for five years.

Tax benefit: Allowable deduction exceeds actual economic value of donated securities.

Front-Loading Charitable Contributions

The Tax Cuts and Jobs Act increased the standard deduction for all taxpayers. In 2022, married taxpayers filing jointly will itemize if their total deductions exceed the standard deduction amount of $25,900. In certain situations, front-loading several years of charitable contributions, perhaps by using a donor-advised fund (DAF), can result in increased deductions over a multiyear period when combined with several years of claiming the standard deduction.

In this scenario, taxpayers could continue to make annual charitable contributions over several years with the amount front-loaded into their DAF.

Tax benefits: Increased level of total allowable deductions over a multiyear period due to the higher standard deduction. May also provide a charitable benefit at the state level.

Qualified Charitable Distribution (QCD)

Taxpayers aged 70½ and over can make distributions directly from their IRA to a qualified charity. The maximum distribution is $100,000 per year (or $200,000 for married taxpayers filing jointly). The QCD can be counted toward satisfying required minimum distributions (RMDs), which begin at age 72. Since QCDs are excluded from income, no corresponding charitable deduction is allowed.

Adjusted gross income will be reduced by the QCD, such that limitations on other tax benefits tied to higher AGI levels may not apply. One such benefit is the 20% deduction for qualified flow-through business income.

Tax benefit: Reduced AGI may yield larger allowable deductions.

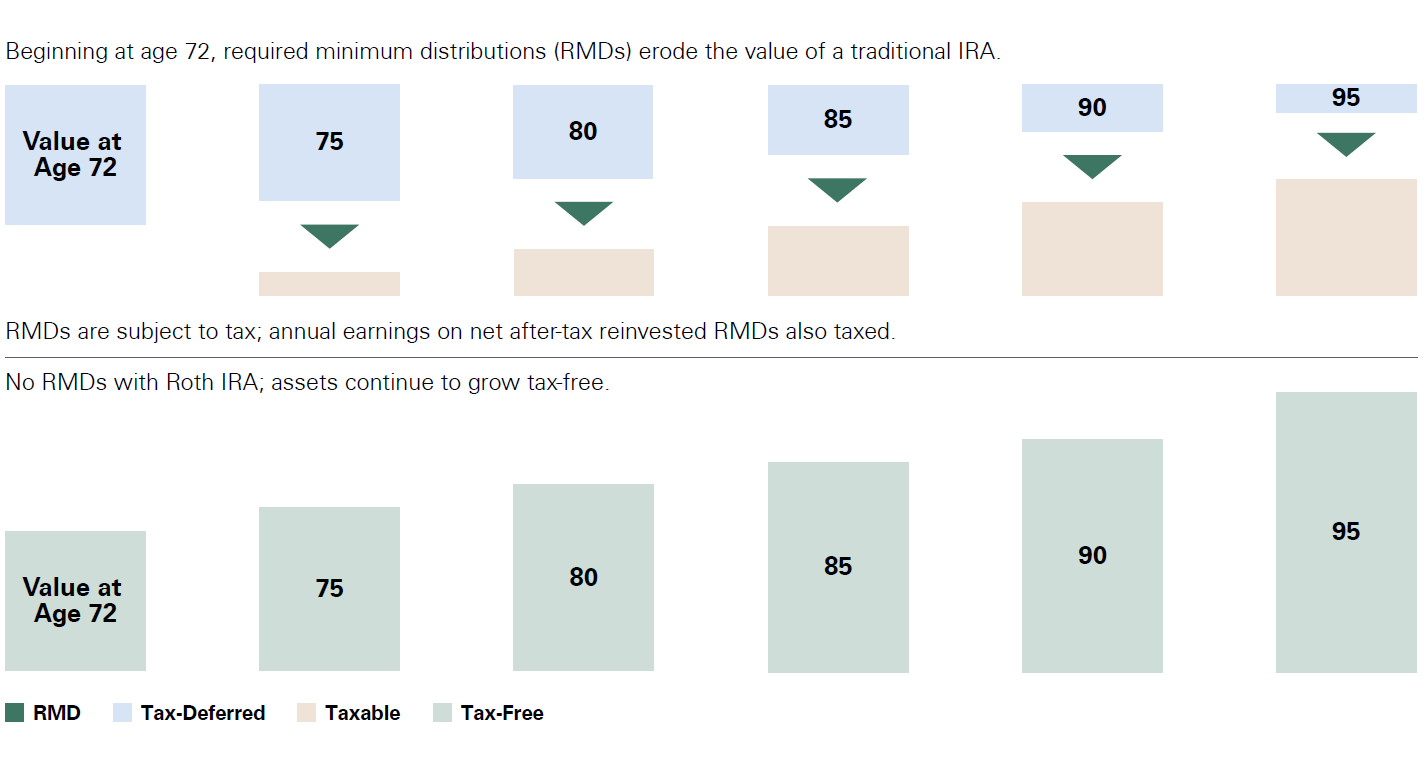

Roth IRA Conversion

Roth IRAs provide an array of valuable tax benefits. All appreciation and income earned in the account is tax-free, and all distributions are excluded from income. Further, there are no RMDs for the owner or spousal beneficiary. (Except in certain situations, non-spouse beneficiaries must distribute the account fully within 10 years.)

Compare this to a traditional IRA, where income is tax-deferred but RMDs do apply beginning at age 72 and distributions are treated as ordinary income, potentially subject to tax at the highest marginal rate. Converting a traditional IRA into a Roth can be a compelling opportunity, especially if the associated tax cost can be reduced or eliminated.

The tax treatment of a Roth conversion is simple: The amount converted must be included in taxable ordinary income in the same taxable year. One strategy to reduce the tax cost is to convert in a tax year where a large charitable contribution is planned. By offsetting income recognized on the conversion, the charitable deduction effectively reduces the tax cost involved.

Another opportunity we have seen is where taxpayers have investments with suspended passive activity losses. These losses become allowable on disposition and can be used to offset the ordinary income connected with a Roth conversion.

Tax benefits: Tax-free income and distributions with no RMDs for owner and spousal beneficiary; tax-free distributions for non-spouse beneficiaries, potential for reduced tax cost on conversion.

Exhibit 1: Traditional IRA vs. Roth IRA

Beginning at age 72, required minimum distributions (RMDs) erode the value of a traditional IRA. RMDs are subject to tax; annual earnings on net after-tax reinvested RMDs also taxed. No RMDs with Roth IRA; assets continue to grow tax-free.

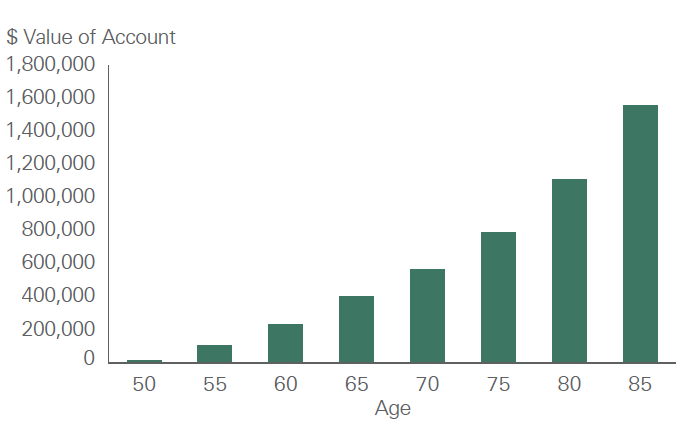

Backdoor Roth Conversions

Although the name might suggest something indecorous, the backdoor Roth conversion is an effective strategy to add to a Roth IRA balance. There are income limits on the direct funding of Roth IRAs. A taxpayer with earned income can bypass these restrictions by setting up and funding a non-deductible IRA and converting the account to a Roth shortly thereafter. Because it was a non-deductible IRA with no appreciation, there is no tax cost on the conversion. This strategy only works where the taxpayer has no existing traditional IRAs.

The maximum contribution is $7,000 per year for 2022 if the taxpayer is age 50 or older ($6,000 if younger than 50). Similar amounts may be contributed for spouses even if they have no earned income.

As seen in Exhibit 2, a married couple aged 50 contributing $14,000 per year for 15 years would have Roth IRAs totaling nearly $1.5 million at age 85.

Tax benefits: Tax-free income and distributions with no RMDs for owner and spousal beneficiary; tax-free distributions for non-spouse beneficiaries.

Exhibit 2: Growth of Roth IRA

Husband and wife each contribute $7,000 ($14,000 total) on January 1 to a Roth IRA

every year for 15 years starting at age 50. Assumes a 7% tax-free growth rate. Above

values represent joint total.

every year for 15 years starting at age 50. Assumes a 7% tax-free growth rate. Above

values represent joint total.

Source: Bessemer Trust

Annual Exclusion Giving

For 2022, every individual is entitled to give $16,000 ($32,000 for a married couple) to any number of individuals without reducing their remaining lifetime exemption. While annual exclusion giving should always be coordinated with the overall estate plan, there are two strategies that can provide significant income tax benefits as well:

529 plans. Congress established 529 plans to encourage saving for future education costs. The vast majority of states sponsor these plans, and most will provide at least a partial annual state income tax deduction for amounts funded, effectively paying people to save for college. A donor can front-load up to five years of annual exclusion gifts to a 529 plan in one tax year.

If account withdrawals are used for qualifying education expenses or tuition, the account earnings will never be subject to income tax. Although direct payments of tuition are not treated as taxable gifts, 529 plan distributions can be used for expenses beyond tuition such as room and board, computer equipment, books, fees, and supplies. Up to $10,000 per year can also be applied toward private elementary or secondary school tuition expenses.

Tax benefits: State tax deduction, tax-free earnings and distributions when used for qualifying education expenses.

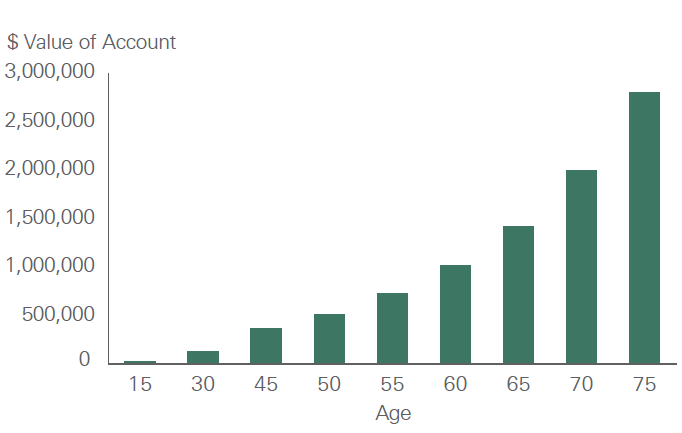

Roth IRA for children. Parents may wish to fund Roth IRA contributions for children as part of an annual giving strategy. Provided that children have earned income, perhaps from a summer job or other employment, Roth IRA contributions are permitted. For adult children with income exceeding $144,000, the backdoor Roth strategy should be considered.

Exhibit 3 shows the long-term value of funding Roth IRAs for children. A Roth IRA is funded with $6,000 each year for 10 years beginning at age 15. There is no funding beyond that. At age 75, the account has grown to more than $2.5 million.

Tax benefits: Tax-free income and distributions with no RMDs for owner and spousal beneficiary; tax-free distributions for non-spouse beneficiaries.

Exhibit 3: Long-Term Growth of Roth IRA for Children

A 15-year-old makes a $6,000 contribution every year for 10 years. Assumes a 7%

tax-free growth rate.

tax-free growth rate.

Source: Bessemer Trust

Summary

The fundamental tax planning strategies discussed above may not provide significant tax benefits in a single year. However, if they are consistently applied on an annual basis, the long-term economic value can be quite substantial.

We hope you have found this discussion helpful. If you have any questions, please contact your client advisor or one of our senior tax consultants.

The information and opinions contained in this material were prepared by Bessemer Trust, and is for informational purposes only. It does not take into account the particular investment objectives, financial situation, or needs of any individual client. This material is based upon information obtained from various sources that Bessemer Trust believes to be reliable, but Bessemer makes no representation or warranty with respect to the accuracy or completeness of such information. Views expressed herein are current only as of the date indicated, and are subject to change without notice. Bessemer Trust does not provide legal advice. Please consult with your legal advisor to determine how this information may apply to your own individual situation. Whether any planned tax result is realized by you depends on the specific facts of your own situation at the time your taxes are prepared.