Ways to Give

- Individuals are increasingly adopting more strategic approaches to their charitable giving.

- The choice of charitable vehicle is a crucial first step in crafting a strategy that aligns your philanthropic and wealth planning objectives.

- We explore the most common and effective vehicles, drawing on insights from our work with clients and their families.

Selecting Your Philanthropic Vehicles

Individual donors are increasingly seeking to be more strategic and impactful in their philanthropy. They’re adopting thoughtful and well-crafted approaches to their charitable giving that integrate with their overall wealth plan, maximize their contributions, and make a measurable and lasting impact on the causes that matter to them.

If you’re looking to make the shift from traditional direct giving to a more strategic approach, one of the crucial decisions is determining which charitable vehicles best fit your philanthropic and wealth planning goals.

Because goals vary from one donor to another, there is no one-size-fits-all approach to giving. At Bessemer, we collaborate with our clients to develop custom frameworks, often employing a combination of vehicles to establish a “charitable toolkit” that prioritizes donors’ goals and desired impact.

We discuss the most common and effective approaches to giving and share insights from our work with clients and their families:

Your Bessemer team can facilitate a seamless and transparent decision-making process — equipping you with current and comprehensive information to make the most effective choices. We are here to work closely with you every step of the way.

Strategic philanthropy starts with choosing the right structure for your charitable and wealth planning goals.

Traditional Grantmaking

The simplest and most direct way of giving to a qualified charity is by contributing cash, securities, or other assets. This enables the donor to have a personal relationship with a nonprofit and allows a high level of flexibility in responding to immediate needs.

A direct gift is tax deductible in the year it is given, subject to certain income-based limitations. Donors can deduct only amounts in excess of 0.5% of their adjusted gross income (AGI). There is also a 35% cap on the tax benefit of all itemized deductions for high earners. For more details, refer to the table titled “Tax Considerations for Charitable Giving.”

Direct giving also has limitations when it comes to ongoing family engagement, but it can be a useful part of any donor’s plan — either as a simple one-time grant, with or without a gift agreement, or as part of a larger plan of complex giving.

Direct giving is the most streamlined giving approach, and it can be an ideal way to begin philanthropic giving; it can also be a useful tool within more complex strategies. We have seen families give thoughtfully and effectively using this method.

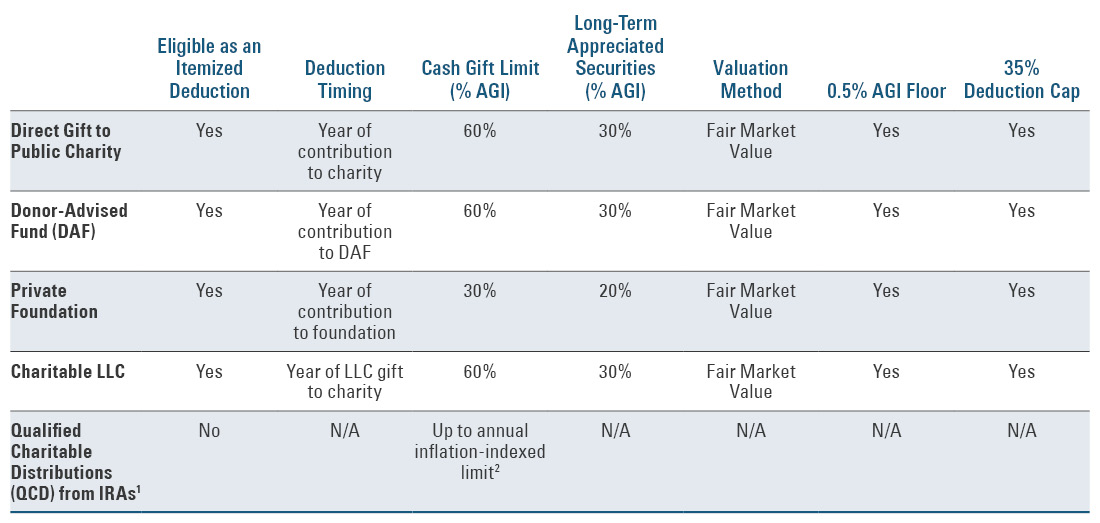

Tax Considerations for Charitable Giving

Donor-level federal tax rules for popular charitable giving vehicles.

A comprehensive comparison table outlining the tax treatment and deduction rules for various charitable giving vehicles, including direct gifts to public charities, donor-advised funds (DAFs), private foundations, charitable LLCs, and qualified charitable distributions (QCDs) from IRAs.

The table highlights that direct gifts to public charities and DAFs are eligible as itemized deductions in the year of contribution, with cash gift limits up to 60% of adjusted gross income (AGI) and long-term appreciated securities capped at 30% of AGI. Both use fair market value for valuation and are subject to a 0.5% AGI floor and a 35% deduction cap.

Private foundations offer lower deduction limits—30% of AGI for cash and 20% for appreciated securities—while still using fair market value and maintaining eligibility for itemized deductions. Charitable LLCs mirror public charity treatment in many respects, including 60% and 30% AGI limits.

Qualified charitable distributions (QCDs) from IRAs differ significantly: they are not itemized deductions, are not subject to AGI percentage limits in the same way, and instead allow annual distributions up to an inflation-indexed limit (noted as $111,000 in 2026). QCDs can only be made to eligible public charities, excluding DAFs and private foundations.

² $111,000 in 2026. Please consult your tax advisor for the most current limits.

As their philanthropy matures, donors often broaden their strategy to include one or more of the charitable vehicles discussed below. For example, the volume of their grantmaking may be increasing, grants may be growing more complex, or they may want to formalize a family giving platform where multiple — and often younger — generations are empowered to engage in the process.

A donor-advised fund, or DAF, is a giving vehicle accessible to donors through individual accounts. It is created and administered by a sponsoring institution, such as the Bessemer Giving Fund or a community foundation, that qualifies as an independent 501(c)(3) public charity. Once the donor makes an irrevocable contribution of personal assets to their DAF account, they can make recommendations to the sponsoring organization as to how those funds are granted to operating charities. Donors may also make anonymous grants. The sponsoring institution almost always honors the recommendation if it names a qualifying public charity to receive the grant.

DAFs allow donors to receive an immediate tax benefit for their charitable giving, and recommend grants from the fund over time. Contributions of illiquid assets may be considered on a case-by-case basis. Compared to other charitable vehicles, they offer an avenue for giving with lower costs, less oversight and effort for the donor, and more efficiency overall. The sponsoring institution is responsible for all administration and compliance of the DAF.

Additional Charitable Fund Structures

Many sponsoring organizations offer these structures as alternatives to donor-advised funds, providing different levels of donor involvement and direction. Both receive the same tax and administrative treatment as donor-advised funds and are available to Bessemer clients through the Bessemer Giving Fund.

Designated Fund

A designated fund allows donors to provide ongoing financial support to one specific charitable organization.

Field of Interest Fund

A field of interest fund allows donors to make an impact in a philanthropic area of their choice without having to select specific organizations. Donors define the parameters of the fund and delegate the sourcing and diligence process to the sponsoring institution.

DAF donations are tax deductible in the year they are made and are subject to the same federal tax limitations that apply to direct gifts.

For a detailed summary, refer to the table titled “Tax Considerations for Charitable Giving.”

At present, DAF accounts are not subject to a minimum annual distribution requirement. Donors experiencing sudden liquidity events often establish DAFs to offset capital gains and gain time to thoughtfully develop their charitable giving plans. This creates room for donors to construct a grantmaking portfolio that will be most meaningful to them and impactful to the communities they support.

Donor-advised funds offer a flexible, tax-efficient, and simple-to-use approach to charitable giving.

One feature that may make DAFs less attractive to philanthropic families is the inability to formally structure a complex governing framework, such as a board with fiduciary authority. To mitigate this, DAF-holding families can assign specific individuals the right to request grants as a donor advisor, which simplifies succession planning.

Although a donor cannot create a formal governance framework within a DAF, Bessemer’s philanthropic advisory team can work with your family to help facilitate consensus and create a decision-making framework that provides the opportunity for family engagement and continuity in giving across generations.

A private nonoperating foundation, referred to in this piece as a private foundation, is a nonprofit grantmaking organization that is created and funded by an individual, family, or corporation. Assets are irrevocably transferred to the foundation, a strategic shift that can offer tax and estate planning advantages.

To avoid penalties, private foundations are required to distribute a minimum percentage of their assets annually for charitable purposes, typically 5%.

Private foundations have the advantage of being able to treat reasonable and necessary operational expenses — such as staff salaries, office rent, tax and legal advisory services, investment management fees, meeting expenses, and related travel — as part of the 5% required distribution to the extent they are necessary to carry out the foundation’s charitable activities.

Unlike DAFs, the net investment income of a private foundation is subject to an excise tax of 1.39%.

While private foundations can be more complicated to establish, from a family engagement and governance perspective, they remain a go-to vehicle for larger-scale endeavors. They are particularly appropriate for families with significant assets to devote to philanthropy.

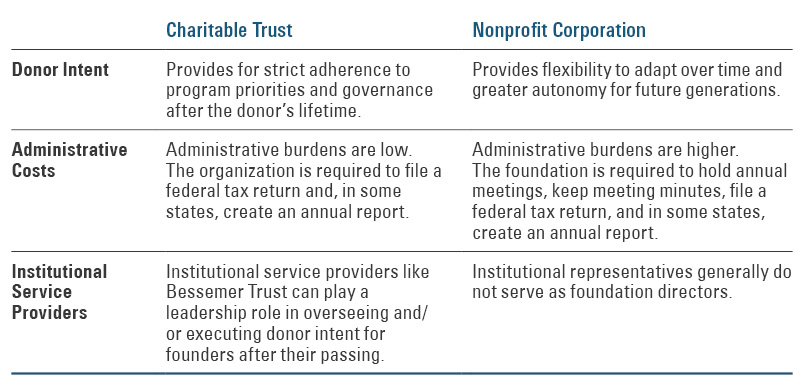

Private foundations can be structured as a charitable trust or a nonprofit corporation. Donors should consider the following elements when determining which structure will work best for their philanthropic goals:

Private Foundation Structural Comparison: Charitable Trust vs. Nonprofit Corporation

A side-by-side comparison of charitable trusts and nonprofit corporations, focusing on donor intent, administrative complexity, and institutional involvement.

Charitable trusts emphasize strict adherence to the donor’s original philanthropic intent, with governance structures designed to preserve those priorities even after the donor’s lifetime. Administrative burdens are relatively low, typically requiring a federal tax return and, in some jurisdictions, an annual report. Institutional service providers, such as wealth management firms, can play a significant role in overseeing and executing donor intent over time.

Nonprofit corporations, by contrast, offer greater flexibility to adapt strategies and mission over time, providing autonomy for future generations. However, they come with higher administrative requirements, including annual board meetings, documented minutes, tax filings, and potential state-level reporting. Institutional providers typically do not serve as directors, reinforcing independence in governance.

Charitable LLCs are playing a growing role for philanthropists who prioritize flexibility, minimal compliance requirements, and privacy, and when immediate tax efficiencies are not the main goal. This vehicle combines the profit-driven nature of traditional business entities with a philanthropic mission. These entities can generate revenue and allocate a portion of their profits to charitable causes — which, when given to a public charity, enables the associated tax efficiencies to flow back to the LLC’s members.

LLCs are not required to disburse any of their assets, and when dissolved, all assets held revert to the members.

It is important to note that no tax deductions are available when funding an LLC. Tax deductions come into play when gifts are made to public charities, and then those tax deductions are available to the owners of the LLC.

Furthermore, all income earned on the assets within the LLC is taxable to its owners. By blending the flexibility of a business vehicle with social responsibility, charitable LLCs offer a new model for traditional grantmaking.

Planned Giving and Estate Planning

In addition to the charitable vehicles previously discussed, several planned giving strategies offer a means to leave a philanthropic legacy and receive a gift or estate tax benefit.

Planned giving vehicles can help to minimize taxes, transfer wealth, and ensure that your assets are distributed according to your wishes.

The most common philanthropic estate planning vehicles are charitable remainder trusts and charitable lead trusts. Variations of these vehicles provide individuals with the ability to support charitable causes while also enjoying certain financial benefits. Planned giving vehicles can be utilized to minimize tax liabilities, transfer wealth, and ensure that your assets are distributed according to your wishes.

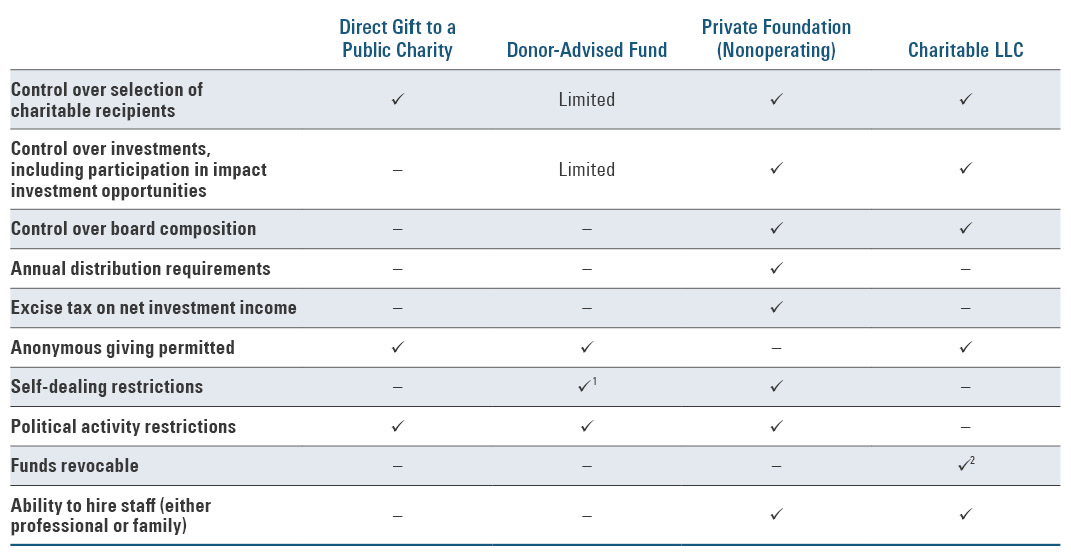

Comparison of Key Features by Charitable Vehicle

Compare charitable giving vehicles based on key structural and governance features.

A detailed comparison matrix evaluating control, regulatory constraints, and operational flexibility across four philanthropic structures: direct gifts to public charities, donor-advised funds (DAFs), private foundations (nonoperating), and charitable LLCs.

The exhibit shows that donors retain full control over recipient selection when making direct gifts, while DAFs provide limited advisory influence. Private foundations and charitable LLCs offer the highest level of control across recipient selection, investment decisions (including impact investing), and board composition.

Private foundations are subject to annual distribution requirements and excise taxes on net investment income, along with strict self-dealing and political activity restrictions. DAFs also face regulatory oversight, including excess benefit transaction rules.

Charitable LLCs stand out for operational flexibility, allowing donors to retain full control of assets, revoke funds, and hire staff, including family members. They also permit anonymous giving and are not bound by the same regulatory constraints as traditional nonprofit entities.

² Since contributions are not treated as charitable gifts, donors retain full control of the assets.

Charitable remainder trusts are useful when donors want to create an income stream for themselves or others but also have charitable intent. The income stream can be in the form of an annuity (the recurring dollar amount is determined at the creation of the trust) or a unitrust (an annual percentage of the trust assets). The annual payments can be structured for a term of up to 20 years or for the lifetime of the individual(s). The remainder interest at the end of the chosen period is left to charity. It is possible to name the donor’s DAF or private foundation as the recipient (with certain tax considerations).

These structures often allow the donor to claim an income tax deduction in the year of the contribution and remove the assets from the donor’s taxable estate.

Charitable lead trusts, on the other hand, are set up to create an income stream for a charity (which may be a DAF or private foundation), with the remainder interest, after the chosen period, going to family members. Again, the income stream can be in the form of an annuity or a unitrust. We often see charitable lead trusts used as an estate tax savings vehicle. You may reduce or eliminate your estate tax liability by leaving the amount of your estate that would otherwise be taxable to a charitable lead trust. This would provide a gift to charity and leave any remainder amount after the term of the charitable lead trust to your heirs.

Individual retirement accounts (IRAs) and life insurance policies can also be used as planned giving vehicles, allowing individuals to make annual distributions or designate beneficiaries to receive the funds upon their death. That said, life insurance policies are used less often, as they are not the most tax-efficient method for making a planned gift. Each spouse age 70½ or older may make annual qualified charitable distributions from an IRA, subject to an inflation-indexed annual limit. Consult your tax advisor for current limits. In addition, IRAs are often excellent choices to leave to charities because their assets would otherwise be subject to both estate and income tax.

Philanthropic Initiatives

A public charity is a tax-exempt nonprofit organization that receives most of its funding from the public, government agencies, corporations, private foundations, and other sources.

Public charities are dedicated to serving the public good by carrying out charitable, educational, religious, scientific, or other philanthropic activities.

Donors might consider starting a nonprofit organization if they are deeply passionate about a specific cause and want to have a direct and sustained impact. However, such an endeavor should be carefully evaluated as it requires full-time dedication and constant fundraising to meet the IRS “public support” test, all of which requires staff, whether paid or volunteer.

Private operating foundations can be thought of as hybrids of traditional private foundations and public charities in that they have limited funding sources but still carry out defined programmatic activities (e.g., museums, zoos, training programs, animal rescue farms). Private operating foundations give donors significant control over program activities if distribution requirements are met.*

Private operating foundations are advantageous for donors who prefer a hands-on approach to their philanthropy. They are well suited to donors interested in funding, staffing, and operating their own charitable initiative(s). Private operating foundations are not subject to any benchmarks for fundraising. While they can accept donations from various sources, they may also be funded in full by a single family.

However, sustainability can be a challenge for some private operating foundations as donors frequently underestimate the time and resources it takes to operate these entities. Some donors who might otherwise be inclined to operate their own charitable vehicle decide against private operating foundations and choose, instead, to make a complex grant to an existing organization to launch the initiative, start up a new nonprofit public charity, or launch a charitable project through a fiscal sponsor.

A fiscal sponsorship is a charitable vehicle in which one nonprofit organization, known as the fiscal sponsor, provides support to a project, individual, or another nonprofit organization that does not have its own 501(c)(3) tax-exempt status.

The fiscal sponsor is responsible for managing finances, receiving donations, and providing other services on behalf of the sponsored entity. This allows the sponsored project to receive tax-deductible contributions, utilize the fiscal sponsor’s established infrastructure and expertise, and focus on its mission without the burden of maintaining its own nonprofit status.

Donors typically consider fiscal sponsorship if they plan to work on a limited-time project or prefer to initially test a program idea. Projects can start quickly without the lengthy process of establishing a new nonprofit organization and have the flexibility to scale up or wind down operations, as needed, without the legal implications of dissolving a separate entity.

To leverage this route most effectively, we often recommend identifying a fiscal sponsor that is already working within the issue area that is aligned with the donor’s mission. This is typically the best option for incubation of a philanthropic initiative.

Charitable LLCs can also serve as flexible vehicles for launching and operating philanthropic initiatives. Donors often choose this structure because they retain full control over contributed assets and can adapt how funds are deployed over time. In addition, the LLC may conduct both charitable and mission-aligned for-profit activities that help support the organization’s work.

With the ability to bring together the best elements of for-profit and nonprofit vehicles, charitable LLCs have been reshaping how donors conceptualize and execute contemporary philanthropic strategies.

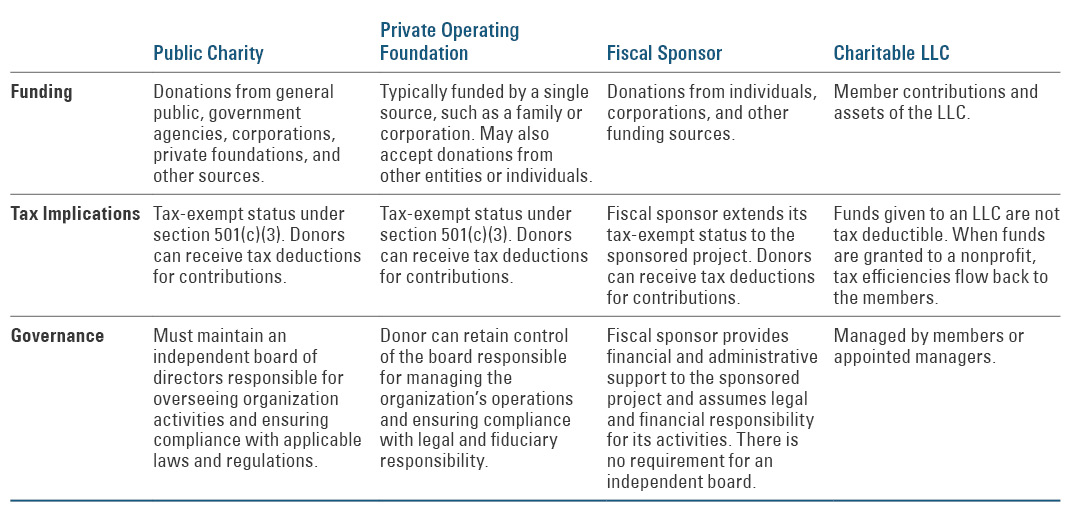

Overview of Philanthropic Initiative Vehicles

Compare key characteristics of vehicles commonly used to launch or operate philanthropic initiatives.

A comparative overview of four philanthropic structures: public charities, private operating foundations, fiscal sponsors, and charitable LLCs, focusing on funding sources, tax implications, and governance models.

Public charities are funded by a broad base, including individuals, corporations, and government sources, and maintain tax-exempt status under Section 501(c)(3), allowing donors to claim tax deductions. Governance requires an independent board responsible for oversight and regulatory compliance.

Private operating foundations are typically funded by a single primary source, such as a family or corporation, but may accept external contributions. They also qualify for 501(c)(3) status and allow donor tax deductions, with governance often remaining under donor or family control.

Fiscal sponsors extend their tax-exempt status to sponsored projects, enabling those initiatives to receive tax-deductible donations without forming a separate legal entity. The sponsor assumes legal, financial, and administrative responsibility.

Charitable LLCs differ structurally, as contributions are not tax-deductible. When funds are granted to nonprofits, tax efficiencies may pass through to members. Governance is flexible, managed by members or appointed managers, and not subject to traditional nonprofit board requirements.

Craft a Strategy That Works — and Works for You

When evaluating charitable giving options, it’s important to look beyond potential tax benefits. Consider the impact you hope to achieve, the timing of your gifts, and any personal circumstances or family dynamics that may shape your approach.

Choosing a giving vehicle — or a combination of vehicles — is often just the beginning. A thoughtful philanthropic strategy also involves identifying the causes that matter most, deciding who to involve in the process, and determining how best to structure and sustain your giving over time.

At Bessemer, we’re here to help you choose the charitable vehicle or mix of vehicles that best aligns with your goals — and to support you in developing a strategic, values-driven approach to your giving.

* A private operating foundation must spend at least 85% of the lesser of adjusted net income or 5% of the value of assets directly for the conduct of its charitable purpose. It must either devote 65% of its assets to its charitable activities or regularly use two-thirds of its minimum investment return for the active conduct of its exempt activities.

Bessemer Trust provides this material to you for your general information. It is based on information obtained from various sources that Bessemer believes to be reliable, but we make no representation or warranty with respect to the accuracy or completeness of such information. The discussion of any tax, charitable giving or estate planning alternatives and other observations herein are not intended as legal or tax advice and do not take into account the particular estate planning objectives, financial situation or needs of individual clients. Views expressed herein are current only as of the date indicated and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in law, regulation, interest rates, and inflation. We do not endorse, represent, or guarantee the organizations mentioned in this publication or their activities.