Supply Chain Round Trip:

Bringing It Back Home

- Increasingly focused on supply chain resiliency, more U.S. companies are diversifying away from an over-reliance on China by bringing production closer to their end markets.

- Aided by the substantial fiscal support provided by recent legislation, industrials and information technology should benefit from U.S. reshoring trends.

- We believe Bessemer portfolios are well positioned for supply chain diversification trends. We retain a heavy overweight to the U.S., which should benefit from increased domestic manufacturing spending. We remain underweight China.

Following the U.S.-China Trade War, which began in 2018, when tariffs were imposed on certain Chinese imports, reshoring gained momentum as the political landscape of conducting business with China became increasingly challenged. While globalization and world trade remain central to the global economy, emerging geopolitical challenges and the COVID after effects have prompted a shift in company sentiment to refocus on supply chain resiliency, which in some cases has resulted in moving production closer to end markets.

In a world where consumer trends can shift rapidly, adaptivity of supply chain management has become increasingly important to companies. Dual sourcing — that is, using two suppliers — has become a popular strategy to optimize production and to mitigate the risk of disruption in one region. To reduce risk going forward, companies are focused on removing supply chain uncertainty where feasible.

Reshoring and Nearshoring — What Are They?

Reshoring is the relocation of production that had been moved overseas back to the origin country with the goal of manufacturing in close proximity to end markets.

Nearshoring is when a company moves production closer to, though not within, end markets.

Background

Throughout much of human history, the exchange of goods was primarily local to each region or country as transportation costs were prohibitively high across long distances. International trade was largely limited to commodity-oriented goods that were scarce locally. However, trade dynamics began to improve meaningfully during the Industrial Revolution of the late 18th century. Over the next two centuries, the development of steamships, canals, railroads, and eventually airplanes, shipping containers, and other innovations lowered production costs and created greater accessibility for the transport of goods.

Lower transportation costs coupled with significant technological differences between countries and increased communications led to the rise in globalization and world trade from the 1970s to the 2010s. As a result of these improvements, China reengaged with the world economy and became the go-to low-cost manufacturing hub as foreign producers looked to capitalize on its lower-wage labor force. However, recent rising wages in China have led to diminishing gains for companies operating relocated manufacturing plants. In addition, a significant wave of regionalization, or when countries look to pursue supply chain diversification, occurred as a result of the U.S.-China Trade War. U.S. companies steadily reduced their import dependence on China from a peak of 21% to 13% today. In its migration from China, the U.S. has invested in production both domestically and internationally, manufacturing in countries such as India, Canada, Vietnam, and Mexico.

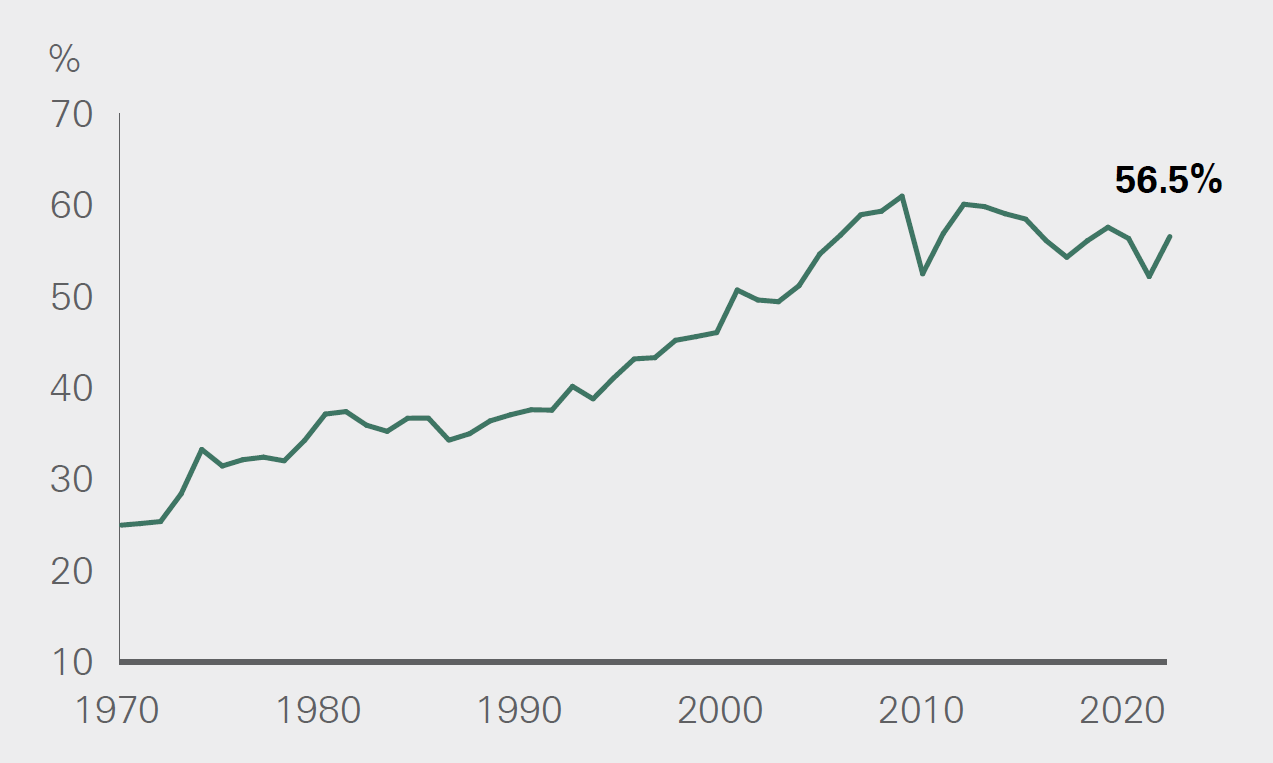

Despite recent fears of the end of globalization, global trade remains above its 30-year average. Historically, trade levels have shifted during times of technological advances or evolving foreign relations. Although global trade as a percentage of global GDP has declined modestly, the current rate of 56.5% is just below the 2008 peak of 61.0% (Exhibit 1).

Supply chain disruptions are likely to continue given ongoing geopolitical conflicts, inflationary pressures, and rapidly shifting consumer trends. Disruptions can impact access to raw materials and trade routes, which in turn impact the flow of goods and price level that consumers pay. A McKinsey survey of 113 supply chain leaders across a variety of industries noted that “97% of respondents said they have applied some combination of inventory increases, dual sourcing, and regionalization to boost resilience. Supply chain leaders believe that these efforts are paying off: 83% have reported that the footprint resilience measures they have taken over the past two years helped them minimize the impact of supply chain disruptions in 2022.”1

Exhibit 1: World Trade as a Percentage of GDP

Key takeaway: Although globalization has been challenged, world trade has continued at a relatively stable level.

Line/area chart illustrating world trade as a percentage of global GDP over time, showing trade levels remaining relatively stable despite geopolitical and pandemic-related disruptions.

Source: Our World in Data

Breaking Away From China

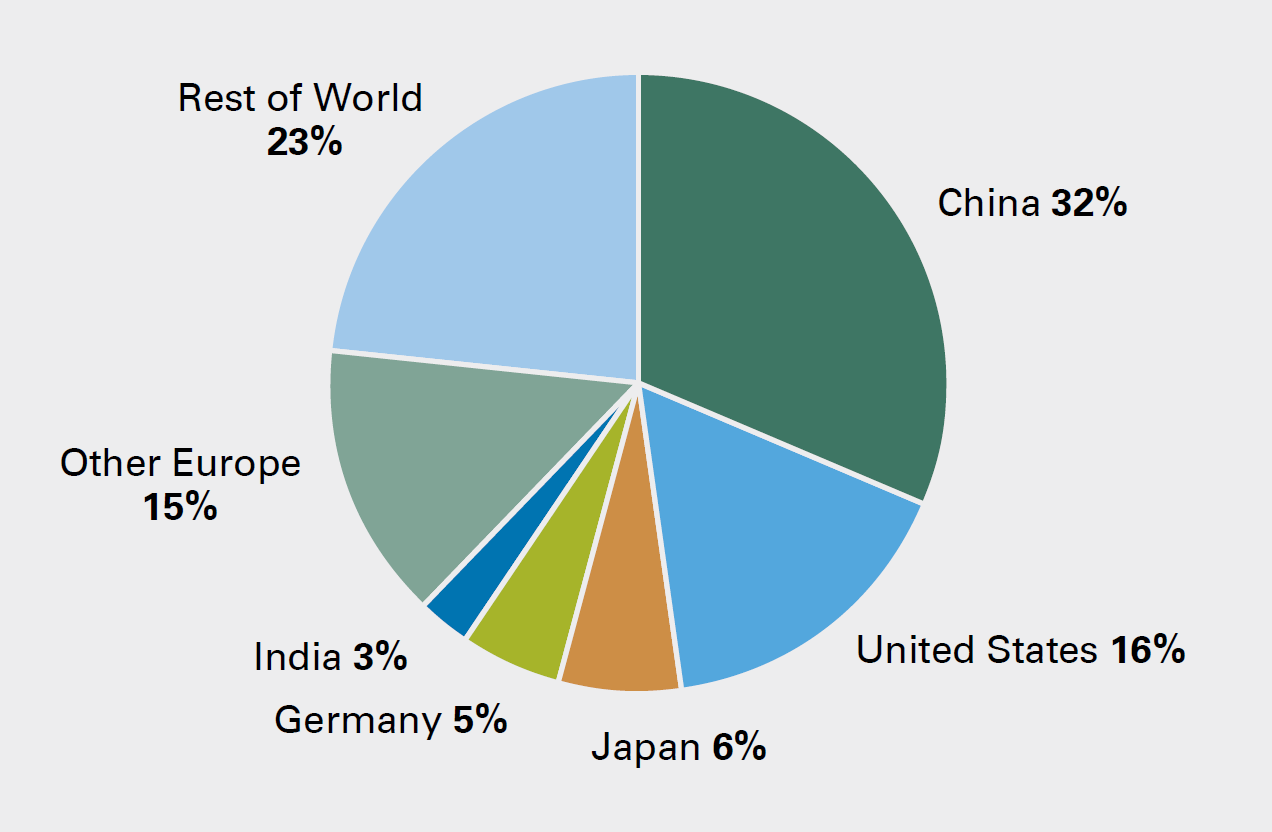

China has a unique position in the global manufacturing landscape given that the quality of infrastructure is competitive with developed countries, but wage dynamics are more favorable. Over time, China was able to increase its share of global manufacturing to over 30% due to the advancement of technology and cheaper labor dynamics (Exhibit 2). Now, China is around a $5 trillion manufacturing economy, representing one-third of the worldwide total and double that of the U.S. Additionally, Chinese manufacturing is well diversified across sectors, whereas 20% of manufacturing in Mexico is concentrated in the automotive sector.

Exhibit 2: Share of Global Manufacturing

Key takeaway: U.S. dependence on China has declined, but China still represents one third of global manufacturing.

Visualization of the distribution of global manufacturing output by country/region, highlighting the relative share of China versus other major manufacturing economies.

Source: United Nations Statistics Divison

Today, China is still deeply interconnected in global supply chains, and although U.S. dependence on China is waning, the ties between the world’s two largest economies won’t disappear overnight. Over 30% of the world’s shipping containers touch Chinese ports, and seven of the world’s 10 busiest ports are in Greater China. While evidence of a resurgence in manufacturing in the U.S. is emerging, China’s role in global manufacturing remains intact.

Following COVID-driven supply chain disruptions stemming from prolonged lockdowns in China, many companies are looking to diversify away from an overdependence on China or bring supply chains closer to the end consumer. New factors are contributing to decisions regarding the sourcing of goods. Production costs still matter, but geopolitical relations, changing wage differentials, government policies, and business continuity risks have taken on greater importance. Western policymakers are now more active in shaping production location decisions; many policymakers are incentivizing local manufacturing in their respective countries to ensure domestic policies support production and capitalize on the economic benefits of domestic manufacturing. Once goods are made, they still need to be shipped to the end customer. This requires highways, railways, and well-functioning ports.

Reshoring and nearshoring trends have garnered investor attention as data has shown increasing evidence of these trends in action. Mexico, which benefits from its proximity to the U.S., is an example of a country that can benefit from reshoring as it continues to invest in infrastructure, increasing its attractiveness for manufacturing and shipping goods.

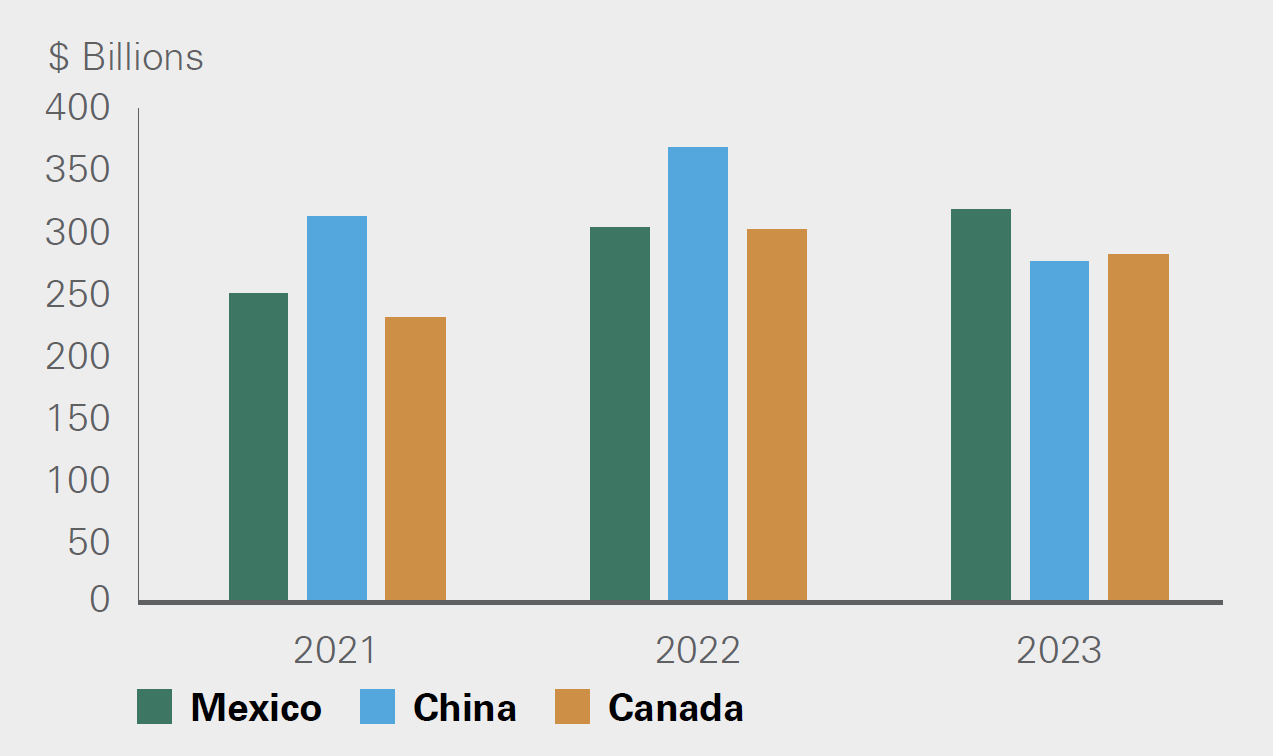

Underscoring this notion, U.S. imports from China fell to their lowest percentage of overall imports since 2005. For the first time in over 15 years, China lost the title of the top exporter of goods to the U.S., as Mexico and Canada became the number one and number two exporters to the U.S., respectively. Additionally, year-to-date imports from China have declined 25% relative to last year (Exhibit 3). Imports from China fell across a wide range of categories, but consumer electronics and industrial equipment, which represent around 20% of imports, significantly declined. We do note that imports from Southeast Asia, excluding China, have increased as companies search for alternative production facilities outside China with cheaper labor. Also, it is possible for the U.S. to import China-produced goods indirectly from Mexico — trade that would not be reflected in reported figures as it is difficult to track.

Exhibit 3: U.S. Imports ($ Billions, January to August)

Key takeaway: U.S. dependency on China has waned as it increasingly relies on other trading partners, such as Canada and Mexico.

Bar or line chart depicting U.S. import values from China and other trading partners from January through August, showing trends in import dependency and diversification.

Source: Bloomberg, U.S. Commerce Department

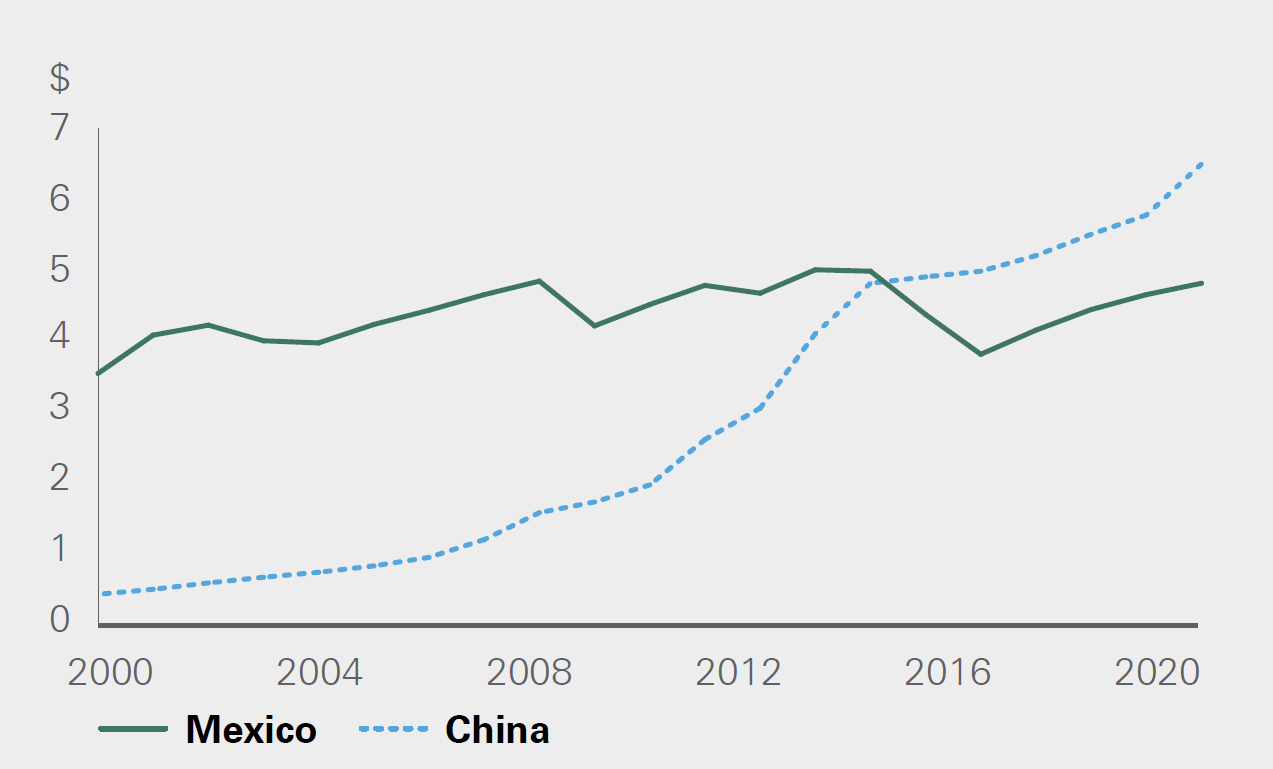

While companies are focused on reshoring, they are mindful of margin compression and are looking for ways to avoid it — for example, through higher costs. A primary driver of moving production to Mexico is the favorable wage dynamic and stable access to labor. For context, before China’s accession to the World Trade Organization in 2001, its U.S. dollar hourly manufacturing labor costs were one eighth those of Mexico. However, there has been a reversal over the last decade as Mexico has become more competitive than China with respect to the cost of labor (Exhibit 4). Although there are fewer people in Mexico (130 million versus 1.4 billion in China), Mexico is not faced with the current labor force issues that China is battling, including a high youth unemployment rate, shrinking population, and a depressed labor force participation rate.

Evidence of companies reducing their dependence on China is emerging, including Apple on the technology side and several original equipment manufacturers (OEMs) on the automotive side. Apple has announced substantial investments in India, where the company recently concluded building an advanced automated facility to manufacture the latest iPhone models. The company set forth its plans to produce 25% of all iPhones in India by 2025, up from 7% currently. While Apple has made progress in bringing production back to the U.S., over 90% of Apple’s production is currently in China, so diversifying from this level will likely take time.

Earlier this year, Tesla announced the construction of a $10 billion Gigafactory in Mexico that will start production of new vehicles by 2025, while BMW announced an $800 million investment in an electric vehicle facility in Mexico that is expected to start production in 2024.

Exhibit 4: Average Compensation in U.S. Dollars per Hour for Manufacturing Workers

Key takeaway: As wages have risen in China, it has become less advantageous to source labor there from a cost perspective.

Comparative chart of average hourly manufacturing wages across key countries (e.g., U.S., China, Mexico), illustrating relative labor cost trends influencing reshoring decisions.

Source: Strategas Research Partners, Supply Chain Dive.com

Industries Benefiting From Reshoring

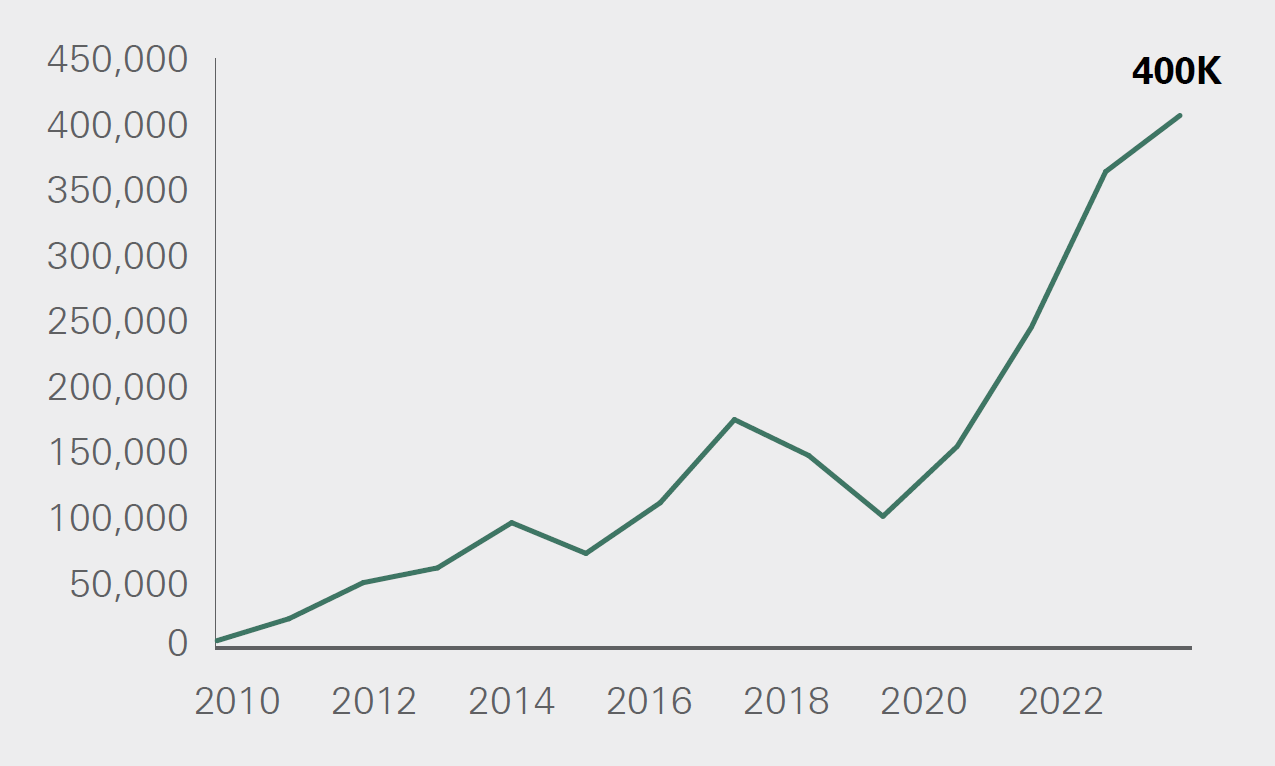

The U.S. has seen reshoring investments materialize since the start of 2022, when construction related to U.S. manufacturing surged. Momentum has continued thus far in 2023 with manufacturing spending levels now at record highs. Additionally, the number of new “reshoring-driven” jobs soared to over 350K in 2022, up 53% from the prior year. From data collected by the Reshoring Initiative, reshoring job growth is projected to continue the growth of 101K seen in the first quarter of this year and reach over 400K by the end of 2023 (Exhibit 5). Of the jobs added in the U.S. in 2022, 66% were in electrical equipment and computer and electronic industries, sectors receiving heightened fiscal support.

Exhibit 5: U.S. Manufacturing Job Announcements Per Year From Reshoring and Foreign Direct Investment

Key takeaway: Reshoring investments have materialized in the U.S., spurring manufacturing job growth.

Annual chart showing the number of U.S. manufacturing job announcements attributed to reshoring and foreign direct investment, reflecting growth momentum in domestic manufacturing employment.

Source: Reshoring Initiative. 2023 figure is the projection for this year based on first quarter results

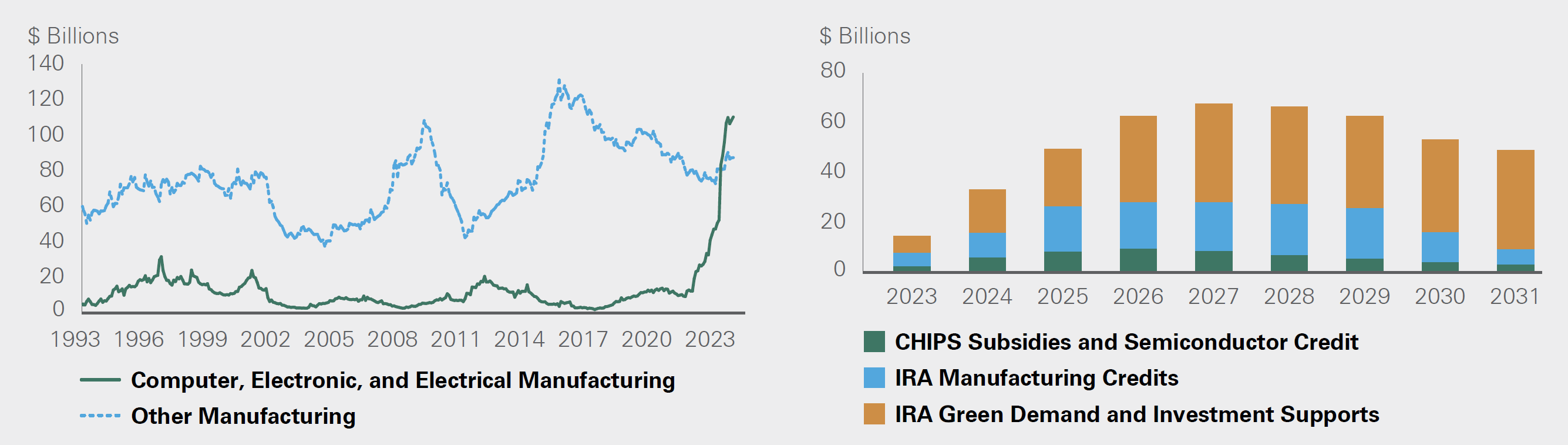

Certain industries are positioned to benefit more from reshoring than others, largely driven by the fiscal support in place. Manufacturing spending has experienced a notable increase in recent months, primarily due to increased spend for computer, electronic, and electrical manufacturing construction (Exhibit 6). The CHIPS Act alone includes $39 billion in subsidies for semiconductor manufacturing on U.S. soil, along with tax credits for the costs of manufacturing equipment. Moreover, the initial $271 billion announced for the Inflation Reduction Act (IRA) is now expected to increase to $500 billion over the next decade. Anticipated future spending as a result of the IRA and CHIPS Act are likely to continue boosting reshoring investment over the coming years.

Exhibit 6: Real Construction Spending of Manufacturing (L), Subsidies for Semiconductors and Batteries (R)

Key takeaway: The increase in manufacturing spending has been largely driven by recently passed legislation intended to incentive domestic manufacturing.

Dual-axis chart depicting real construction spending in the manufacturing sector on the left axis and government subsidies for semiconductors and battery production on the right, illustrating policy-driven capital flows.

Source: CBO, Department of Commerce, Piper Sandler

While some reshoring was occurring before the passage of these bills, efforts have been expedited because of the new legislation. In total, over $200 billion of new semiconductor investment in the U.S. has been announced over the last two years as a result of the CHIPS Act, IRA, and the Infrastructure Investment and Jobs Act (IIJA). This progress follows a period in which the U.S. represented a declining share of global semiconductor fabrication capacity, falling from 37% in 1990 to 12% in 2020. The CHIPS Act spurred the announcement of 23 new chip fabs along with the expansion of nine existing fabs in the U.S. Additionally, the tax incentives provided to manufacturers under the IRA are likely to support the manufacturing of electric vehicle batteries.

While some industries have seen a rapid push to reshore production, others may not benefit as much from a cost perspective. As we detail in our fourth quarter Quarterly Investment Perspective, for some pharmaceutical companies, producing drugs in China can be 20% to 30% cheaper, so we expect to see less focus on reshoring in some areas of healthcare.

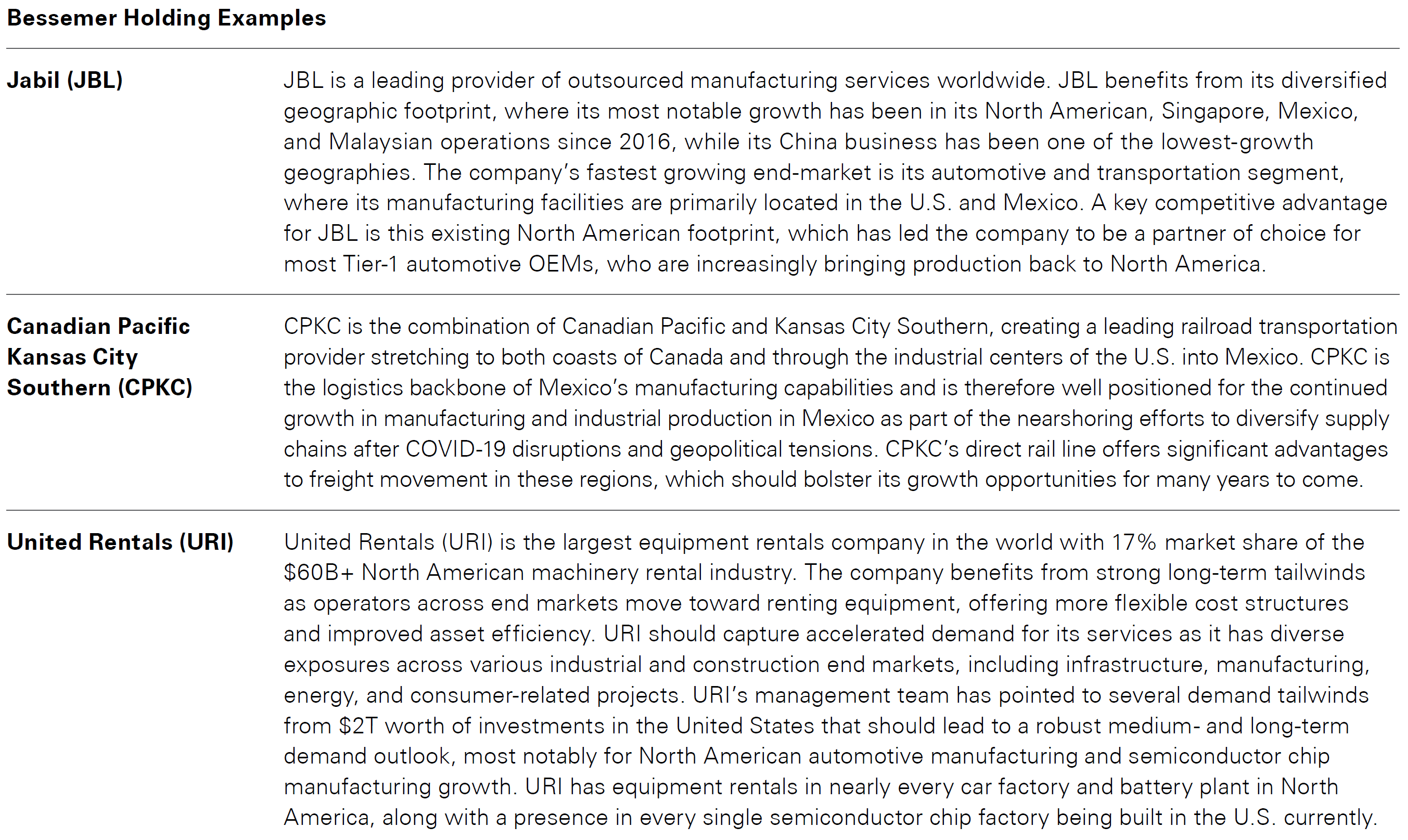

Geographically, reshoring activity has increased in Mexico as the country is close in proximity, has an agreeable political environment, and offers a low-cost, highly skilled labor force. Mexico enjoys a free trade agreement with the U.S., and its proximity allows for superior integration into just-in-time inventory chains. Mexico’s labor dynamics are attractive; according to data from the Nearshore Company, the average manufacturing wage in the U.S. is about 10 times higher than in Mexico. Bessemer portfolios own Canadian Pacific Kansas City Southern (CPKC), the combination of Canadian Pacific Railroad and Kansas City Southern Railroad that resulted in a leading transportation provider stretching to both coasts of Canada and through the industrial centers of the U.S. into Mexico. CPKC is the logistics backbone of Mexico’s manufacturing capabilities, and we believe it is well positioned for the immense growth in manufacturing and industrial production in Mexico as part of the nearshoring efforts to diversify supply chains. CPKC’s direct rail line offers significant advantages to freight movement in these regions, which should bolster its growth opportunities for many years to come. Please see Exhibit 7 for more detail on CPKC and other relevant Bessmer holdings.

Exhibit 7: Bessemer Public Equity Exposure

Key takeaway: Bessemer public equity holdings play a pivotal role in the reshoring process.

Bar or pie visualization showing the composition of Bessemer Trust’s public equity holdings aligned with reshoring trends, indicating sector and regional exposure supporting supply chain diversification.

Risks From Reshoring

Globalization has been an important driver of the lower inflation seen in many developed markets over the past decade prior to 2021, and the shift of supply chain management away from solely the cheapest inputs may pose an inflationary risk. To the extent that companies shift production for non-economic reasons, the outcome could be inflationary, though we believe the risk is low. The reshoring that has occurred thus far is in sectors where producers are receiving incentives from the government via the CHIPS Act or IRA, reducing the risk that higher costs will be passed onto consumers given the subsidies received. While reshoring could create upside risks to inflation, there are important mitigating factors, such as artificial intelligence, that could offset this risk by improving productivity. At the moment, more than 80% of warehouses do not utilize any sort of automation. To the extent that we see automation enhancements, inflation risks could be modestly offset.

As geopolitical tensions rise, the political environment becomes increasingly important. Between the tariffs imposed on China in 2018 and the more recent export bans, tensions between the U.S. and China have increased, putting a strain on the trade partnership. Although we believe the U.S. and China are likely to continue implementing divisive policies, the U.S., Mexico, and Canada passed a free trade agreement in 2020 to support trade and workers’ rights. While trade policy is crucial, emerging areas of reshoring opportunity present risks as well. Mexico, for example, faces obstacles related to stable and reliable sources of power, which creates potential risks if there are not improvements in its electricity infrastructure. Mexico’s economy also materially differs in size from China, and therefore capacity and economic constraints could put a limit on reshoring efforts. Overall, however, we believe the benefits of reshoring ultimately outweigh the geopolitical and inflationary risks.

Conclusion

We believe Bessemer portfolios are well positioned for supply chain diversification trends. Bessemer portfolios remain overweight the industrials and information technology sectors, both of which we expect to benefit from reshoring trends into North America.

We maintain a heavy overweight to the U.S., which should benefit from the offshoots of increased domestic manufacturing spending. Given building headwinds to the economic outlook for China, Bessemer portfolios are underweight the country.

Overall, we believe that supply chains are likely to be hedged and rewired, but we do not think they will be dismantled. The adjustment of supply chains is a process that can take years. For now, we see continued momentum in industries such as semiconductors, where ample fiscal support is in place. Fiscal support is likely to continue to drive investment within the U.S., and in a challenging economic environment, elevated fiscal stimulus should provide economic support in the coming years.

- Taking the Pulse of Shifting Supply Chains, McKinsey & Company

This material is for your general information. It does not take into account the particular investment objectives, financial situation, or needs of individual clients. This material is based upon information obtained from various sources that Bessemer Trust believes to be reliable, but Bessemer makes no representation or warranty with respect to the accuracy or completeness of such information. The views expressed herein do not constitute legal or tax advice; are current only as of the date indicated; and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. Bessemer Trust or its clients may have investments in the securities discussed herein, and this material does not constitute an investment recommendation by Bessemer Trust or an offering of such securities, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference.